After ending the previous session off its worst levels but still notably lower, the price of crude oil saw further downside during trading on Friday.

Crude for July delivery slumped $1.12 or 1.6 percent to $70.17 a barrel after tumbling $1.24 or 1.7 percent at $71.29 a barrel during Thursday’s trading.

The continued weakness in the price of crude oil reflected ongoing concerns about the outlook for demand ahead of several key central bank meetings next week.

“Next week will be big for oil as we get a few major central bank rate decisions that should determine the short-term outlook for the global economy,” said Edward Moya, senior market analyst at OANDA.

“China may cut rates, the Fed could deliver a hawkish skip, and the ECB is still playing catch up with their tightening cycles,” he added. “Oil will eventually trade higher when stockpiles are at uncomfortably low levels.”

The Federal Reserve’s monetary policy meeting is likely to be in the spotlight, with the U.S. central bank expected to pause its recent interest rate increases.

Traders are likely to pay close attention to the Fed’s accompanying statement as well as key inflation due next week for clues about the outlook for rates.

Statistics Canada says the unemployment rate rose to 5.2 per cent in May, marking the first increase since August 2022.

The federal agency says overall employment was little changed last month as the economy lost a modest 17,000 jobs.

The job report comes two days after the Bank of Canada raised its key interest rate by a quarter of a percentage point, citing concerns about a string of hot economic data, including low unemployment.

The unemployment rate previously hovered at five per cent for five consecutive months.

Last month, there were fewer people working in business, building and other support services as well as professional, scientific and technical services, while employment rose in manufacturing, utilities and services such as maintenance.

Meanwhile, wages continued to grow rapidly in May, rising by 5.1 per cent compared to a year ago.

Economists surveyed by Reuters expected China’s consumer price index to rise 0.3% year-on-year after marking a two-year low of 0.1% in April. Month-on-month, economists predicted a 0.1% decline.

Recent economic data pointed to a disappointing recovery from China’s strict Covid lockdown measures as the economy struggles with softening demand and falling exports.

Canada’s exports jumped 2.5 per cent in April and hit an all-time high by volume, while imports declined 0.2 per cent partly because of a fall in energy products, Statistics Canada said on Wednesday.

As a result, the country’s trade surplus with the world widened to $1.94-billion in April, more than double analysts’ forecasts of a C$900-million surplus. March’s surplus was downwardly revised to $231-million from $972-million.

The Canadian economy has largely been outperforming expectations despite record-paced interest rate hikes by the Bank of Canada between March 2022 and January this year.

The bank on Wednesday raised its key overnight benchmark rate to a 22-year high of 4.75 per cent on increasing concerns that inflation could get stuck significantly above its 2 per cent target amid persistently strong economic growth.

Stuart Bergman, chief economist at Export Development Canada, said April’s data was good but cautioned that the exports level may not be sustainable.

“”At face value the headline number is fairly good but as you dig a little bit deeper there is cause for some concern as to whether we would expect to see these export gains repeated in May and June,” Bergman said.

The surge in exports was driven by metal and non-metallic mineral products as well as energy products, Statscan said. By volume, exports were up 2.8 per cent and surpassed pre-COVID-19 pandemic levels.

The rise in metal product exports included higher transfers of gold assets from Canadian financial institutions to the United States in a sign economic uncertainty is making investors favour the safe-haven metal, the agency said.

“The cautionary note is many of those volume shipments reflect those truckloads of gold being shipped down to the U.S. and so certainly that’s not something that we would expect to see repeated in future months,” Bergman said.

Imports declined for a third consecutive month, in part due to lower crude shipments from Saudi Arabia and the United States. Imports of refined petroleum products also contributed to the decrease. By volume, total imports increased 1 per cent.

Last week, data showed that Canada’s economy benefited from favourable international trade and expanded faster than expected in the first quarter ended March and likely accelerated further in April. Annual inflation also came in hotter than anticipated in April, accelerating for the first time in 10 months to 4.4 per cent, more than double the BoC’s 2 per cent target.

The decision lifts the policy rate to 4.75 per cent, the highest level since May, 2001, pushing up mortgage rates and squeezing household budgets.

The central bank’s campaign had been on hold since January as it waited to see if borrowing costs were high enough to get inflation under control. However, a run of stronger-than-expected data over the past month called that “conditional pause” into question and brought the bank off the sidelines.

Deputy governor Paul Beaudry will deliver an economic progress report on Thursday outlining the bank’s rationale for this week’s decision. The speech to the Victoria Chamber of Commerce starts at 3:25 p.m. ET, with a press conference 4:45 p.m. It will be Mr. Beaudry’s last appearance before he retires from the bank in July.

The Bank of Canada’s next rate decision is on July 12, when it will also publish an updated projection for economic growth and inflation.

Statistics Canada will release May Labour Force Survey data on Friday. Central bankers will be watching this closely for signs that the labour market is weakening. This could mean an uptick in unemployment or a slowdown in the pace of wage growth. May consumer price index data –which tracks inflation – will be published on June 27.

The U.S. Federal Reserve’s next rate announcement is on June 14. Chair Jerome Powell suggested last month that the central bank could pause its rate-hike campaign at the next meeting. However, stronger-than-expected economic data has kept open the possibility of a least one more rate increase this summer.

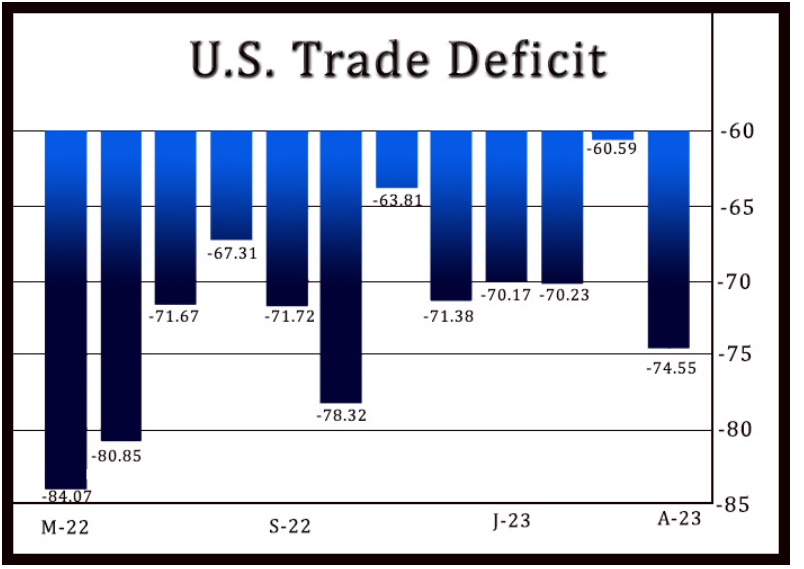

A report released by the Commerce Department on Wednesday showed the U.S. trade deficit widened significantly in the month of April.

The Commerce Department said the trade deficit increased to $74.6 billion in April from a revised $60.6 billion in March.

Economists had expected the trade deficit to jump to $75.2 billion from the $64.2 billion originally reported for the previous month.

The trade deficit in April marked the biggest since the deficit reached $78.3 billion in October 2022.

The wider trade deficit came as the value of exports plunged by 3.6 percent to $249.0 billion in April after surging by 1.8 percent to $258.2 billion in March.

The sharp pullback by exports reflected a steep drop in exports of industrial supplies and materials, including crude oil, as well as a notable decrease in exports of consumer goods.

Meanwhile, the report said the value of imports jumped by 1.5 percent to $323.6 billion in April after tumbling by 1.6 percent to $318.8 billion in March.

Imports of automotive vehicles, parts and engines led the rebound, with imports of industrial supplies and materials also showing notable growth.

“Net exports will likely be a drag on Q2 US GDP as resilient consumer spending keep imports elevated,” said Matthew Martin, U.S. Economist at Oxford Economics.

He added, “That said, we expect imports to weaken in the months ahead as consumers continue to normalize spending patterns and businesses investment feels the pinch of tighter lending conditions and higher interest rates.”

The Commerce Department also said the goods deficit spiked to $96.1 billion in April from $81.6 billion in March, while the services surplus rose to $21.6 billion from $21.0 billion.

After leaving interest rates unchanged for two straight meetings, the Bank of Canada on Wednesday announced it has decided to once again raise rates.

The Bank of Canada increased its target for the overnight rate by 25 basis points to 4.75 percent, citing stubbornly high inflation and stronger than expected economic growth.

Canada’s central bank said the rate hike reflects its view that monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2 percent target.

The Bank of Canada also said it is continuing its policy of quantitative tightening, which it said is complementing the restrictive stance of monetary policy and normalizing the bank’s balance sheet.

The bank’s Governing Council said it will continue to assess the dynamics of core inflation and the outlook for consumer price inflation.

The Bank of Canada reiterated that it remains resolute in its commitment to restoring price stability for Canadians.

The Canadian market is down marginally around late morning on Wednesday, with investors digesting the Bank of Canada’s decision to raise interest rates by 25 basis points.

The Canadian central bank this morning increased its target for the overnight rate by 25 basis points to 4.75%, citing stubbornly high inflation and strong than expected economic growth.

The BoC, which had left interest rates unchanged for two straight meetings, said the rate hike reflects its view that monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target. The central bank reiterated that it remains resolute in its commitment to restoring price stability for Canadians.

The bank’s Governing Council said it will continue to assess the dynamics of core inflation and the outlook for consumer price inflation.

Technology stocks are notably lower. Several stocks from healthcare, consumer staples and consumer discretionary sectors are also weak. Energy stocks are gaining, tracking higher crude oil prices.

The benchmark S&P/TSX Composite Index is down 37.00 points or 0.19% at 20,018.60 a few minutes before noon. The index, which climbed to 20,149.95 just before the announcement of the rate decision, dropped to 19,994.29 subsequently.

The Canadian market is down marginally around late morning on Wednesday, with investors digesting the Bank of Canada’s decision to raise interest rates by 25 basis points.

The Canadian central bank this morning increased its target for the overnight rate by 25 basis points to 4.75%, citing stubbornly high inflation and strong than expected economic growth.

The BoC, which had left interest rates unchanged for two straight meetings, said the rate hike reflects its view that monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target. The central bank reiterated that it remains resolute in its commitment to restoring price stability for Canadians.

The bank’s Governing Council said it will continue to assess the dynamics of core inflation and the outlook for consumer price inflation.

Technology stocks are notably lower. Several stocks from healthcare, consumer staples and consumer discretionary sectors are also weak. Energy stocks are gaining, tracking higher crude oil prices.

The benchmark S&P/TSX Composite Index is down 37.00 points or 0.19% at 20,018.60 a few minutes before noon. The index, which climbed to 20,149.95 just before the announcement of the rate decision, dropped to 19,994.29 subsequently.

Among technology stocks, Hut 8 Mining Corp (HUT.TO) is down 3.7% and Shopify Inc (SHOP.TO) is lower by about 3.1%. BlackBerry (BB.TO), Quarterhill (QTRH.TO), Open Text Corp (OTEX.TO) and Descartes Systems Group (DSG.TO) are down 2 to 2.2%. Kinaxis (KXS.TO) and Converge Technology Solutions (CTS.TO) are also notably lower.

Healthcare stocks Tilray Inc (TLRY.TO) and Canopy Growth Corporation (WEED.TO) are down 2.5% and 2%, respectively. Bausch Health Companies (BHC.TO) is down 0.7%.

Consumer discretionary stocks Sleep Country Canada Holdings (GOOS.TO), Restaurant Brands International (QSR.TO) and MTY Food Group (MTY.TO) are down 2.4%, 2.2% and 1.9%, respectively.

Data from Statistics Canada showed, Canada posted a trade surplus of C$ 1.94 billion in April of 2023, wider than the downwardly revised surplus of C$ 0.23 billion in the previous month. Exports jumped by 2.5% to C$ 64.8 billion, while imports fell by 0.2% to C$ 62.9 billion.

Exports fell 7.5% in May from a year ago, far worse than the 0.4% decline predicted by a Reuters poll.

Imports for May dropped by 4.5% from a year ago — less than the 8% plunge forecast by Reuters.

The decline was so sharp that export volumes are below their levels at the start of the year, after accounting for seasonality and changes in export prices, Julian Evans-Pritchard, head of China Economics, at Capital Economics, said in a note.

Top Biotech IPOs Of 2021 That Soared As Much As500%Top Biotech IPOs Of 2021 That Soared As Much As 500%-Share Story

Top Biotech IPOs Of 2021 That Soared As Much As500%Top Biotech IPOs Of 2021 That Soared As Much As 500%-Share Story