Author: Consultant

-

May 17 – The close: Stocks rise but TSX underperforms as speculation grows another BoC rate hike looms

Major stock indexes rose on Wednesday, but the Canadian benchmark underperformed Wall Street as money market traders continued to raise bets that the country’s central bank will hike interest rates another time following a hotter-than-expected inflation report this week.

Gains in North American equity markets were fueled by optimism over a potential deal on the US$31.4 trillion debt ceiling and as a rebound in regional bank shares eased concerns about an escalation in the sector’s troubles.

But the advance was uneven in Toronto. The utilities sector, which is particularly negatively impacted by rising interest rates because of high debt levels among its companies, was down 0.6%, on top of a 1.1% decline on Tuesday when the inflation data was released. But the real estate sector bounced back, rising 0.7%. Industrials and consumer staples sectors were marginally lower, but financials gained 0.8% and energy rose 1.4%.

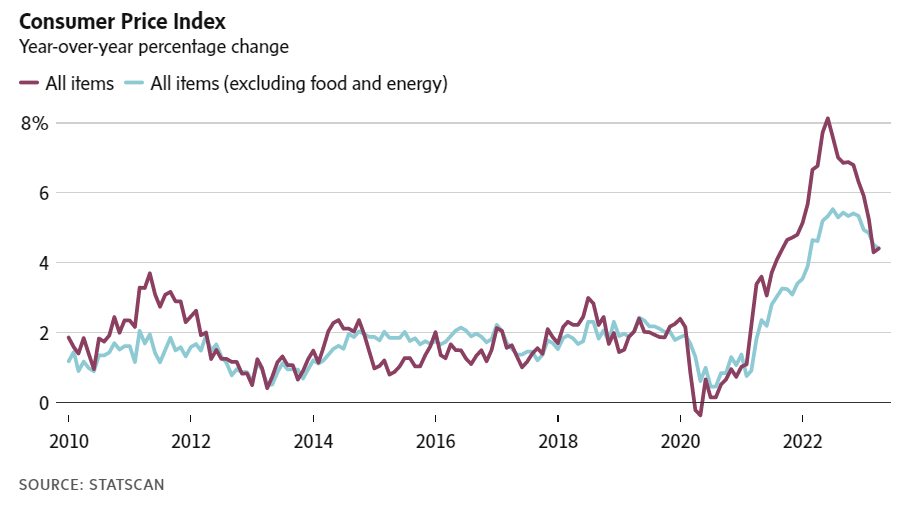

Canada’s annual inflation rate ticked up to 4.4% in April, as higher shelter costs contributed to the first acceleration in the consumer price index in 11 months. The reading surprised the Street, which was looking for a rise of 4.1%.

Interest rate probabilities based on trading in swaps markets immediately priced out any expectations that the Bank of Canada would cut interest rates by the end of this year, and started pricing in a modest risk the bank would hike rates again. Those bets continued to intensify on Wednesday. They now imply a greater than 60% chance of a further quarter-point rate hike by the end of this summer.

While many economists continue to believe the bank will stick to its current overnight rate, some are expressing less confidence. Some market observers believe the bank, which has left the door open to possible further rate hikes if needed, will need to tighten policy further.

“The Bank of Canada will likely be forced into hiking rates on June 7th because the upside risks to its inflation projections are materializing and the downside risks have begun to fade,” Jay Zhao-Murray, FX Analyst at Monex Canada, a foreign currency firm, said in a note.

“Instead of cooling to the point of near-stagnation, the Canadian economy has consistently proved more resilient than the Bank had expected: in April, the Bank revised its Q1 GDP forecast from 0.5% to 2.3%, yet nowcast models point to 3.0% growth for Q1, which suggests the economy has even more excess demand than they had thought,” he said.

Capital Economics, which had been forecasting the Bank of Canada would cut interest rates before the year is out, changed its stance on Wednesday.

“The rapid turnaround in the housing market and the upside surprise to CPI inflation in April have raised the case for another interest rate hike from the Bank of Canada, which we now judge is slightly more likely than not,” said Capital Economics deputy chief North America economist Stephen Brown in a note late in the day.

“The potential for US debt ceiling negotiations to go down to the wire, with negative effects for financial markets in early June, is one reason for the Bank to stay on the side-lines at its meeting next month. But we now anticipate another 25 basis point hike in July and doubt the Bank will cut rates until 2024.

Reflecting the threat of another move higher in the Bank of Canada’s key lending rate as well as action in the U.S. Treasury market Wednesday, bond yields in Canada continued to rise.

The Canadian 2-year yield touched its highest level since March 10 at 4.072% before dipping to 4.058%, up 8.7 basis points on the day. The gap between it and the equivalent U.S. rate was at 9.2 basis points, its narrowest since Sept. 16.

The S&P/TSX composite index ended up 54.36 points, or 0.3%, at 20,296.43.

The health-care sector was up 4.9%. It was boosted by a 24.1% jump in Bausch Health Companies Inc shares after a Delaware court ruling helped guard the patent for the company’s antibiotic drug for traveler’s diarrhea.

Elsewhere, shares of BlackBerry Ltd advanced 5.9% as the company forecast sales jumping as much as 54% in 2026 from 2023 on the back of growth in its cybersecurity business.

President Joe Biden and top U.S. congressional Republican Kevin McCarthy on Wednesday reiterated their determination to strike a deal soon to raise the debt ceiling and avoid an economically catastrophic default.

If an agreement is not reached by June 1, the U.S. Treasury has said it could begin to run out of funds to pay the government’s bills, potentially igniting a recession.

A jump in regional bank shares lifted sentiment, led by a 10.19% surge in Western Alliance Bancorp a day after the bank said deposits grew by more than $2 billion in the quarter ended May 12.

The KBW regional bank shot up 7.28% to notch its biggest one-day percentage gain since Jan. 6, 2021 to close at its highest level since May 1. The S&P 500 banks index also surged 4.46% for its biggest daily percentage gain since Nov. 10.

“It is optimism over the debt ceiling. It is continued optimism the banking crisis is in the rear-view mirror. Every day we go without a new problem, the closer we get to maybe putting it behind us,” said Rick Meckler, partner at Cherry Lane Investments in New Vernon, New Jersey.

“Definitely the catalyst is when you get both Biden and McCarthy to say that we are close the assumption is they probably will go with some kind of agreement.”

The Dow Jones Industrial Average rose 408.63 points, or 1.24%, to 33,420.77; the S&P 500 gained 48.87 points, or 1.19%, to 4,158.77; and the Nasdaq Composite added 157.51 points, or 1.28%, at 12,500.57.

The gains marked the biggest one-day percentage climb for each of the three major indexes since May 5.

Also providing support was a 4.41% advance in Tesla shares after its annual shareholder meeting on Tuesday.

Top boss Elon Musk downplayed market speculation he may step down as CEO of Tesla, touched upon two new mass-market models the company is developing, and reaffirmed that deliveries of its long-delayed Cybertruck pickup would start this year.

In addition, a source with direct knowledge of the matter told Reuters the electric vehicle maker has proposed setting up a factory in India for domestic sale and export.

With the rally the S&P is once again near the top of a recent trading range, at about 4,160, which has acted as a resistance point. Analysts said a major catalyst such as a debt ceiling agreement or clarity on the path of interest rate hikes from the Federal Reserve would be needed to push stocks much higher.

Recent data has indicated slowing in the U.S. economy following a string of Fed rate hikes to fight high inflation. That, along with recent negotiations over the U.S. debt ceiling, has focused attention on when the central bank will pause hiking, or cut interest rates.

While the market is pricing in at least a rate cut by the year-end, recent comments from Fed officials suggested they are not ready to cut rates soon.

Retailers Target Corp and TJX Companies Inc forecast current-quarter profit below expectations despite beating estimates for the first quarter.

Shares of Target rose 2.58%, while TJX Companies closed 0.93% higher after a choppy session. The gains, along with Tesla’s rally, helped lift the consumer discretionary sector about 2%.

Volume on U.S. exchanges was 10.35 billion shares, compared with the 10.59 billion average for the full session over the last 20 trading days. Advancing issues outnumbered decliners on the NYSE by a 2.95-to-1 ratio; on Nasdaq, a 2.45-to-1 ratio favored advancers. The S&P 500 posted 20 new 52-week highs and 14 new lows; the Nasdaq Composite recorded 69 new highs and 123 new lows.

-

Stock futures rise as Wall Street focuses on debt ceiling negotiations: Live updates

UPDATED WED, MAY 17 2023 7:08 AM EDT

Stock futures rose Wednesday as investors awaited news of developments in the negotiations between congressional leaders and President Joe Biden on the U.S. debt ceiling.

Futures tied to the Dow Jones Industrial Average added 133 points, or 0.4%. S&P 500 futures and Nasdaq-100 futures gained 0.4% and 0.2%, respectively.

The White House said Tuesday that Biden has directed staff to meet daily on outstanding issues. The president also canceled the second leg of an upcoming international trip given the negotiations, the White House said. House Speaker Kevin McCarthy said that a “better process” is now in place for further talks. He also said that it’s “possible to get a deal by the end of the week.”

Tuesday’s “meeting between President Biden and House Speaker McCarthy went as well as could have reasonably been hoped for,” wrote Citi chief U.S. economist Andrew Hollenhorst, in a note. “We continue to expect a long-term debt ceiling deal.”

Concerns over the potential of default weighed on investors in Tuesday’s regular session. The Dow led the major indexes down with a 1% drop, followed by the S&P 500 and Nasdaq Composite with respective losses of about 0.6% and 0.2%.

Treasury Secretary Janet Yellen reiterated her warning that the government needs to raise the limit immediately as the country faces the possibility of defaulting as early as June 1.

Disappointing quarterly revenue and a lower forecast for full-year performance from Dow member Home Depot also soured investor sentiment in Tuesday’s session. On the economic front, April retail sales were weaker than anticipated by economists polled by Dow Jones.

In addition to tracking any updates on debt ceiling negotiations, investors will watch for data on housing starts and building permits on Wednesday.

-

Canada ‘extremely concerned’ about fate of Line 5 pipeline in Wisconsin, embassy says

Canada is “extremely concerned” about the potential fate of the Line 5 pipeline, emissaries warned Tuesday in advance of a Wisconsin court hearing that threatens to shut down what they call a vital cross-border oil and gas corridor.

The warning from Canada’s embassy in Washington comprised Ottawa’s first formal comments about the pipeline in months – a lengthy, measured statement that nonetheless made plain its fears for Line 5′s future.

And it leaned hard into three areas always sure to get attention in the U.S.: protecting American jobs and growth, defending continental energy security, and honouring treaty obligations to an important and trusted ally.

“The energy security of both Canada and the United States would be directly impacted by a Line 5 closure,” the statement from the Canadian embassy in Washington said.

“At a time of heightened concern over energy security and supply, including during the energy transition, maintaining and protecting existing infrastructure should be a top priority.”

The economic argument is one the pipeline’s proponents have been making for years: a shutdown would cause “significant economic disruption” across the U.S. Midwest, where it provides feedstock to refineries in Michigan, Ohio and Pennsylvania.

Line 5 also supplies refineries in Ontario and Quebec, and is vital to the production of jet fuel for some of Canada’s busiest airports. Some 33,000 U.S. jobs and US$20-billion in economic activity would be imperilled, the embassy warned.

The source of the alarm is a court dispute in Wisconsin between the pipeline’s owner, Alberta-based Enbridge Inc., and the Bad River Band of the Lake Superior Chippewa, through whose territory Line 5 runs.

Spring flooding has washed away significant portions of the riverbank where Line 5 intersects the Bad River, a meandering, 120-kilometre course that feeds Lake Superior and a complex network of ecologically delicate wetlands.

The band has been in court with Enbridge since 2019 in an effort to compel the pipeline’s owner and operator to reroute Line 5 around its traditional territory – something the company has already agreed to do.

But the flooding has turned a theoretical risk into a very real one, the band argued in an emergency motion last week, and it wants the pipeline closed off immediately to prevent catastrophe.

“There can be little doubt now that the small amount of remaining bank could be eroded and the pipeline undermined and breached in short order,” the band’s lawyers argued.

“Very little margin for error remains.”

Line 5 meets the river on Indigenous territory just past a location the court has come to know as the “meander,” where the riverbed snakes back and forth multiple times, separated from itself only by several metres of forest and the pipeline.

At four locations, the river was less than 4.6 metres from the pipeline – just 3.4 metres in one particular spot – and the erosion has continued in recent days at an “alarming” rate, the motion said.

In one case, so-called “monuments” installed to measure the losses show that where there was more than 10 metres of riverbank in early April before the flooding began, only 3.7 metres remained as of last Tuesday.

“Significant erosion is continuing as of the filing of this motion, and the evidence strongly suggests that further bank loss could be substantial and result in exposure and rupture of the pipeline.”

Wisconsin district court Justice William Conley is expected to hear oral arguments on the motion Thursday. It’s not clear if he’ll reserve judgment or rule immediately whether to order Enbridge to shut down the pipeline and purge its contents.

But Justice Conley has already indicated a reluctance to shut down the pipeline, citing the potential economic and foreign-policy consequences, suggesting Tuesday’s statement from the embassy was aimed squarely at him.

“I think Canada is saying, ‘Please be aware,’ ” said Kristen van de Biezenbos, a professor of energy law at the University of Calgary.

Because there are no alternatives to Line 5 for shipping fossil-fuel energy to Ontario and Quebec, the stakes of a shutdown would likely be higher for Canada than for the U.S., she added.

“Even knowing that it’s not a great idea to be largely dependent on just one source of oil, there hasn’t been anything done to change that,” Prof. van de Biezenbos said.

“It would be a serious problem for Canada if Line 5 was shut down – not just because of the wider economic impacts for the oil patch in Alberta, but also because that is the main source of crude oil products for Eastern Canada.”

Later Tuesday, lawyers for Enbridge began filing a raft of affidavits and sworn statements from pipeline safety experts, scientists, environmental engineers and even the company’s own director of tribal engagement, all in opposition to the request for an injunction.

One of them, from a Vancouver hydrologist named Hamish Weatherly, acknowledged that the threat of a rupture caused by erosion is higher than it was at the end of last year, but still far from critical.

“It is thus my opinion based on my knowledge, training and experience that there is not an ‘emergency’ or ‘imminent threat’ of a release at the meander,” Mr. Weatherly’s declaration reads.

A separate declaration from David Stafford, the company’s U.S. pipeline compliance manager, said the U.S. Pipeline and Hazardous Materials Safety Administration has been kept apprised of all the latest developments.

“Since receiving notification of the erosion at the meander, PHMSA has not expressed any concern regarding the safety of Line 5 at this location,” Mr. Stafford asserts in the document.

Tuesday’s filings also included a string of affirmations from senior executives across the Canadian energy sector from companies such as Suncor, Cenovus, Imperial Oil, Shell Canada and Superior Gas, among others.

Canada has already invoked a 1977 pipelines treaty with the U.S. in both Wisconsin and Michigan, where that state’s Attorney-General is also in court trying to get the pipeline shut down.

Talks under that treaty have been continuing for months, with the latest session taking place last month in Washington.

“Canada invoked the treaty’s dispute settlement provisions because actions to close Line 5 represent a violation of Canada’s rights under the treaty to an uninterrupted flow of hydrocarbons in transit,” the embassy said.

“If a shutdown were ordered because of this specific, temporary flood situation, Canada expects the United States to comply with its obligations under the 1977 Transit Pipelines Treaty, including the expeditious restoration of normal pipeline operations.”

The key word there is “temporary,” Prof. van de Biezenbos said.

“The pipeline treaty makes it clear that you can order temporary shutdown of international pipelines between the U.S. and Canada for public safety reasons,” she said.

“If there is a shutdown that’s ordered because of the flooding, then as soon as the flood risk has been abated, then the pipeline has to be brought back online.”

-

Inflation ticks higher in April, testing Bank of Canada rate pause

Canada’s annual inflation rate ticked higher in April, a surprise acceleration that shows the road back to price stability could be long and bumpy.

The Consumer Price Index rose 4.4 per cent in April from a year earlier, after a 4.3-per-cent increase in March, Statistics Canada reported on Tuesday. Financial analysts were expecting an inflation rate of 4.1 per cent. Adjusted for seasonality, consumer prices rose 0.6 per cent in April from March.

The annual inflation rate has nearly halved since hitting a peak of 8.1 per cent last June. However, wrestling inflation back to the Bank of Canada’s 2-per-cent target is unlikely to be a smooth process.

While the central bank projects inflation will simmer to around 3 per cent this summer, it has also warned that price increases in the services sector could prove sticky. The bank forecasts a return to 2-per-cent inflation by late 2024.

The CPI numbers, combined with a tight labour market, will test whether the Bank of Canada thinks interest rates are sufficiently high enough to restrain inflation.

“One month does not a trend make. We have still cut inflation almost in half from where it stood at the peak,” said Avery Shenfeld, chief economist at CIBC Capital Markets.

However, Mr. Shenfeld said the Canadian economy will need to experience a material slowdown – notably in the hot labour market, which has a near-record-low unemployment rate – to bring inflation under control.

“Even though a lot of the inflation has melted away, we can’t really expect to get to 2 per cent without seeing any economic pain whatsoever,” he said.

The latest CPI numbers were heavily influenced by gasoline and some aspects of the housing market. Gas prices rose 6.3 per cent in April, which Statscan pinned on an OPEC+ decision to reduce oil output, thereby raising prices. Crude prices have tumbled since mid-April, which should help lower the headline inflation rate in May.

Mortgage interest costs rose 28.5 per cent on an annual basis in April as more homeowners dealt with sharply higher borrowing rates. Rents jumped 6.1 per cent from a year earlier. Statscan said higher interest rates may be contributing to more demand for rental units as would-be buyers get priced out of home ownership.

On the other hand, there was progress at the supermarket. Prices for groceries rose 9.1 per cent in April from a year earlier, down from 9.7 per cent in March. Grocery inflation appears to have peaked at more than 11 per cent in recent months. Cost increases at earlier stages of the supply chain – for instance, the prices received by farmers – have slowed dramatically of late, which should influence consumer prices in the months to come.

The short-term trend for inflation was less favourable last month. Expressed at an annualized rate, three-month core inflation – excluding food and energy – was 4.2 per cent in April, up from 3.1 per cent in March.

Bank of Canada officials have repeatedly stressed in recent communications that the final leg of restoring price stability – getting inflation to 2 per cent from 3 per cent – could prove challenging.

To successfully bring inflation under control, several things will need to happen, Governor Tiff Macklem said in a recent speech at the Toronto Region Board of Trade. These include a moderation in wage growth, a normalization of corporate pricing behaviour and lower expectations of near-term inflation.

Despite the inflation uptick on Tuesday, the Bank of Canada is widely expected to hold its policy rate at 4.5 per cent at its next decision on June 7. Over less than one year, the central bank raised its benchmark interest rate at eight consecutive meetings before pausing in March. The Bank of Canada is intentionally trying to slow the economy to bring supply and demand into better balance. However, that pause is not set in stone.

“If we start to see signs that inflation is likely to get stuck materially above our 2-per-cent target, we are prepared to raise rates further,” Mr. Macklem said in his speech.

Mr. Shenfeld of CIBC doesn’t think we’ve hit that threshold yet, a view that was widely shared on Bay Street on Tuesday. It can take time – 18 to 24 months – for rising interest rates to fully transmit to the economy. Moreover, there are ample signs that economic growth has slowed to a tepid pace in recent months.

At the same time, employers are continuing to churn out thousands of jobs by the month, which has kept the unemployment rate at 5 per cent, just shy of a record low.

“If we look at inflation overall, it’s still twice as hot as the Bank of Canada wants to see,” Mr. Shenfeld said. “We’re not going to get resistance to higher prices until we have incomes growing more slowly.”

-

Home Depot hits the brakes:

Three-year robust sales run ends amid pull back on home improvements

Home Depot couldn’t keep its protracted robust sales streak going any longer. The home improvement chain reported a dismal quarter as consumer spending on home improvement projects – which was buoyed by the stay-at-home pandemic lifestyle – come to a screeching halt.

The retailer posted disappointing sales for its first quarter and lowered its outlook for the year after customers slowed their spending. Home Depot (HD) said sales fell 4.5% at stores open at least a year during its latest quarter, and its income decreased 6.4% from the same stretch a year ago.

Total revenue for the quarter slipped 4.2% versus a year ago, to $37.3 billion. The retailer also cited falling lumber prices and weather-related challenges, including heavy rains in California during the period, for denting its sales.

“After a three-year period of unprecedented growth for our sector, during which we grew sales by over $47 billion, we expected that fiscal 2023 would be a year of moderation for the home improvement market,” Home Depot CEO Ted Decker said Tuesday.

The company also lowered its sales expectations for the year. It expects sales to decline between 2% and 5% in 2023 from a year prior.

-

Stellantis halts battery plant construction over dispute with Canadian government

Automaker Stellantis has stopped all construction at a more-than C$5 billion ($3.74 billion) electric vehicles battery manufacturing plant in Windsor, Canada, over a disagreement with the federal government about subsidies, a spokesperson for the company said on Monday.

“Effective immediately, all construction related to the battery module production on the Windsor site has stopped,” the spokesperson said.

A spokesperson for Canada’s Innovation Minister, Francois-Philippe Champagne, did not immediately respond to a request for comment.

The move comes days after the carmaker and South Korea’s LG Energy Solution Ltd (373220.KS) said they were implementing “contingency plans” related to a more-than C$5 billion ($3.74 billion) battery plant investment in Canada.

Champagne, who described the deal as Stellantis’s largest ever in the Canadian auto sector when it was announced, on Friday said the “auto industry is crucial to the Canadian economy and to the hundreds of thousands of Canadian workers”.

LGES and Stellantis announced their battery plant investment in the country last year, aiming for an annual production capacity in excess of 45 gigawatt hours (GWh) and expected to create an estimated 2,500 new jobs in the Windsor area.

In April, Canada had also agreed to provide up to C$13 billion in subsidies and a C$700 million grant to lure Volkswagen AG into building its North American battery plant in the country.

Canada’s deal with the German automaker for a battery gigafactory, announced this year, is the biggest single investment ever in the country’s electric-vehicle supply chain.

-

Turkey’s Erdogan faces toughest test yet in landmark election — with high stakes for the world

- Turkey’s presidential and parliamentary elections on May 14 could hardly come at a more polarized moment for the country of 85 million.

- Incumbent President Recep Tayyip Erdogan is in the fight for his political life after two decades in power.

- Opposition leader Kemal Kilicdaroglu is gaining in polls as Turks face a cost-of-living crisis and the current government is accused of becoming increasingly authoritarian.