With its stock down 11% over the past three months, it is easy to disregard Tourmaline Oil (TSE:TOU). But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. Particularly, we will be paying attention to Tourmaline Oil’s ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

A $400-million lawsuit against four businesses, two of them large corporations, filed on behalf of a group of Mexican migrants who were illegally trafficked across the GTA and housed in York Region, has received a sharp rebuke from Aurora’s Magna International.

At the beginning of March, police announced the shockingly poor living conditions a group of Mexican irregular migrants were forced to withstand as they were trafficked at work places across the GTA.

During a news conference, York Regional Police said 64 Mexicans were illegally brought into the country with promises of well-paying jobs before they were placed in grubby housing in East Gwillimbury and taken across many cities to work places where they were poorly paid and treated.

On March 31, Diamond and Diamond Lawyers announced it is launching a class-action lawsuit on behalf of some of these victims against four businesses, including Magna International and Gwillimdale Farms, alleging the migrants were working at these companies and that the businesses should have known.

“Human trafficking is a reprehensible crime, and we are proud to represent the brave victims in this lawsuit,” Sandra Zisckind, a managing partner at the firm, wrote. “Our goal is to ensure that these corporations are held accountable for their actions and that justice is served for the survivors of this horrific crime.”

Magna and Gwillimdale, along with the other two businesses, “have been accused of being complicit in human trafficking”, she wrote, alleging they either knowingly participated in human trafficking, or chose to “ignore the signs and evidence”.

The other two businesses being sued are a resort in Muskoka and another produce company in northern York Region.

In a statement posted on Magna’s website, spokesperson Tracy Fuerst wrote that in recent weeks, the company has been “voluntarily supporting” the Canadian Border Services Agency in its investigation into human trafficking and illegal migration.

China may already dominate the world’s supply chains of rare earth metals. Even so, it is increasingly worried about securing enough raw materials to feed its vast industrial appetite.

Numbers bear this out. China’s grip on rare earth production has slipped even as other countries have ramped up their own production. Its share of global mining output fell to 58% in 2021, from a high of 98% in 2010. At the same time, its imports of rare earth raw materials have grown, jumping nearly 40% in 2021, according The Rare Earth Observer, an industry newsletter.

The Canadian market extended its winning streak to a sixth session with stocks from technology, consumer discretionary and industrials sectors posting strong gains on Friday.

The mood was bullish as worries about a banking continued to ease, and data showing an expansion in Canadian economic activity in the month of February aided sentiment.

Data showing an unexpected slowdown in the annual rate of core consumer price growth in the U.S. helped as well.

The benchmark S&P/TSX Composite Index ended with a gain of 158.90 points or 0.8% at 20,099.89, after hitting a high of 20,126.54 intraday. The index gained more than 3% in the week, and 3.7% in the January-March quarter.

The Information Technology Capped Index surged 2.36%. BlackBerry (BB.TO) soared 14.4%. Lightspeed Commerce (LSPD.TO) climbed 6.2%, while Quarterhill (QTRH.TO), Hut 8 Mining (HUT.TO) and Haivision Systems (HAI.TO) gained 4.5 to 5.5%. Shopify Inc (SHOP.TO), Constellation Software (CSU.TO), Celestica Inc (CLS.TO), Descartes Systems (DSG.TO) and Kinaxis Inc (KXS.TO) also posted strong gains.

Among consumer discretionary stocks, Canada Goose Holdings (GOOS.TO) gained more than 5%. Linamar Corp (LNR.TO), Pet Valu Holdings (PET.TO), Magna International (MG.TO), Restaurant Brands International (QSR.TO) and Spin Master Corp (TOY.TO) advanced 2.3 to 3.2%.

In the Industrials sector, Snc-Lavalin, Bombardier Inc (BBD.B.TO), Ballard Power Systems (BLDP.TO), Brookfield Business Partners (BBU.UN.TO), Badger International (BDGI.TO), Finning International (FTT.TO), Richelieu Hardware (RCH.TO), WSP Global (WSP.TO), Toromont Industries (TIH.TO) and Air Canada (AC.TO) gained 2 to 4%.

Cogeco Inc (CGO.TO), Docebo Inc (DCBO.TO), Ag Growth International (AFN.TO), Goeasy (GSY.TO), Cargojet (CJT.TO) and Canadian Tire Corporation (CTC.A.TO) were among the other major gainers in the session.

Shaw Communications (SJR.B.TO) gained about 3.3% after the Minister of Innovation, Science and Industry Francois-Philippe Champagne approved the company’s C$20 billion ($14.8 billion) buyout of Shaw Communications.

Rogers Communications and Shaw Communications announced today that their historic merger is expected to close prior to the outside date of April 7

On the economic front, the Canadian economic activity likely increased by 0.3% over a month earlier in February 2023, preliminary estimates showed.

In January, the GDP increased by 0.5%, following a slight 0.1% contraction in December.

Several OPEC+ members on Sunday announced intentions to voluntarily cut a further combined 1.16 million barrels per day of production, in a move independent from the broader bloc’s output strategy.

The reductions will challenge consumer governments, such as the U.S., which are already tackling high inflation and volatility in the banking sector.

A formal meeting of an OPEC+ technical committee takes place Monday to review the group’s existing strategy. It cannot change policy.

Canada’s Teck Resources Ltd TECK-B-T +0.80%increase said on Monday that its board has unanimously rejected an unsolicited acquisition proposal from Swiss commodity firm Glencore Plc.

U.S.-listed shares of Teck rose 10 per cent in premarket trading.

The offer would see Glencore acquiring Teck and subsequently creating two businesses which would expose Teck shareholders to thermal coal and oil trading, the Canadian copper miner said in a statement.

The proposed separation into Teck Metals and Elk Valley Resources is in the best interest of Teck and all its stakeholders, it added.

“The board is not contemplating a sale of the company at this time,” Teck Chair Sheila Murray said.

Rogers Communications Inc. RCI-B-T -2.88%decrease paying $20-billion to buy Shaw Communications Inc.SJR-B-T +3.27%increase is among the largest ever made-in-Canada corporate takeovers, but the windfall for the many bankers, lawyers and other professionals who advised on the deal is even more historic.

When the transaction was first announced more than two years ago, Rogers estimated in regulatory filings at the time that total fees – including everything from charges for financial advisers, lawyers, accountants and proxy solicitors to printing and mailing costs – would be roughly $100-million.

And that was before racking up tens of millions of dollars in legal fees fending off regulatory opposition and paying lenders hundreds of millions of dollars to extend the deadline for the deal to get done.

Just resolving the legal dispute with the federal Competition Bureau generated more than $30-million in legal fees, according to regulatory submissions.

Rogers declined to comment on how much the company ultimately expected to pay in total. However, public records show the amount will be substantial simply because of the sheer number of advisers involved and the complexity of the transaction itself.

Bank of America Corp., for example, served as a financial adviser to Rogers since the proposal was first announced in March, 2021 and, at the same time, provided the company with a $19-billion bridge. That money represented one of the largest bridge loans in Canadian history.

One year later, when Rogers replaced that loan with proceeds from U.S. and Canadian bond sales totalling US$7.05-billion and $4.25-billion, respectively, BofA was joined by Citigroup Inc., JPMorgan Chase & Co. and Royal Bank of Canada in managing that debt offering. Rogers also committed to a $6-billion term loan from an unnamed group of banks.

In August, 2022, the company paid its lenders $557-million to extend the deadline on those bonds, according to its latest annual report. When the deal had still not closed by the end of last year, Rogers was required to pay its lenders another $262-million.

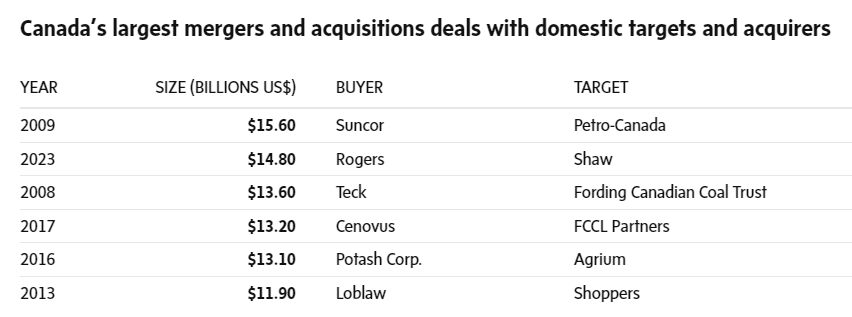

Another aspect of this deal that made it especially lucrative to Bay Street is the fact that both buyer and seller are Canadian, meaning the vast majority of fees were paid to domestic advisers. According to data from the Institute for Mergers, Acquisitions and Alliances, Rogers buying Shaw counts as the second-most-valuable instance of one Canadian company buying another since Suncor Energy Inc. acquired Petro-Canada in 2009.

Suncor, in its pursuit of Petro-Canada, also managed to avoid many of the lengthy delays and regulatory battles that plagued the Rogers-Shaw transaction.

Then there was the Rogers family feud that erupted just a few months after the Shaw acquisition was first proposed, pitting Edward Rogers, the only son of company founder Ted Rogers, against his mother and two of his sisters.

Ken McEwan, founding partner of McEwan Partners LLP, represented Mr. Rogers in the dramatic legal battle that ended in November, 2021, when the Supreme Court of British Columbia reaffirmed his authority to overhaul the company’s board of directors.

Mr. Rogers also retained crisis communications firm Navigator Ltd. throughout the dispute and Walied Soliman, chair of Norton Rose Fulbright Canada LLP, was hired by his sister – Melinda Rogers-Hixon – to oppose him.

Beyond fees paid by Rogers directly, other corporate players made major contributions to the Bay Street payday related to this deal. Quebecor Inc., which will see its Videotron division acquire Shaw’s Freedom Mobile for $2.85-billion as part of the transaction, hired Bennett Jones LLP to represent its interests in the recent dispute at the Competition Tribunal, which public filings show came at a cost of roughly $2-million.

“If the fees are a high number, it reflects the reality of what it takes to get a complex transaction done in a highly regulated industry where there are significant issues,” said John Clifford, chief operating officer at McMillan LLP and a partner in the firm’s merger and acquisition practice, who was not directly involved in the deal.

“We are talking a lot these days in the M&A world about increased scrutiny on transactions by regulators, particularly the competition and antitrust authorities, making it more difficult to get complicated deals done. And that just means more advisers and more costs,” Mr. Clifford said.

“It is a reflection of the effort required, particularly as it relates to the lawyers who charge by the hour as opposed to the investment bankers who charge a percentage of the deal price.”

Goodmans LLP served as the legal adviser for Rogers over the course of the Shaw transaction while Shaw retained Davies Ward Phillips & Vineberg LLP as well as Wachtell, Lipton, Rosen & Katz.

Oil prices soared as much as 8% at the open after OPEC+ announced it was slashing output by 1.16 million barrels per day.

The voluntary cuts will start from May to end 2023, Saudi Arabia announced, saying it was a “precautionary measure” targeted toward stabilizing the oil market.

DUBAI (Reuters) – Saudi Arabia and other OPEC+ oil producers on Sunday announced further cuts in their production amounting to around 1.16 million barrels per day in a surprise move they said was aimed at supporting market stability.

The development comes a day before a virtual meeting of an OPEC+ ministerial panel, which includes Saudi Arabia and Russia, and which had been expected to stick to 2 million bpd of cuts already in place until the end of 2023.

Oil prices last month fell towards $70 a barrel, the lowest in 15 months, on concern that a global banking crisis would hit demand. Still, further action by OPEC+ to support the market was not expected after sources downplayed this prospect and crude recovered towards $80.

The latest reductions could lift oil prices by $10 per barrel, the head of investment firm Pickering Energy Partners said on Sunday.

Sunday’s pledges bring the total volume of cuts by the Organization of the Petroleum Exporting Countries, Russia and other allies to 3.66 million bpd according to Reuters calculations, equal to 3.7% of global demand.

“OPEC is taking pre-emptive steps in case of any possible demand reduction,” Amrita Sen, founder and director of Energy Aspects, said on Sunday.

Last October, OPEC+ had agreed to an output cut of 2 million bpd from November until the end of the year, a move that angered Washington as tighter supply boosts oil prices.

The U.S. has argued that the world needs lower prices to support economic growth and prevent Russian President Vladimir Putin from earning more revenue to fund the Ukraine war.

Sunday’s unexpected voluntary cuts start from May.

Saudi Arabia said it would cut output by 500,000 bpd while Iraq will reduce its production by 211,000 bpd, according to official statements.

The UAE said it would cut production by 144,000 bpd, Kuwait announced a cut of 128,000 bpd while Oman announced a cut of 40,000 bpd and Algeria said it would cut its output by 48,000 bpd. Kazakhstan will also cut output by 78,000 bpd.

Russia’s Deputy Prime Minister Alexander Novak also said on Sunday that Moscow would extend a voluntary cut of 500,000 bpd until the end of 2023. Moscow announced those cuts unilaterally in February following the introduction of Western price caps.

An OPEC+ source said Gabon would make a voluntary cut of 8,000 bpd and not all OPEC+ members were joining the move as some are already pumping well below agreed levels due to a lack of production capacity.

After Russia’s unilateral reductions, U.S. officials said its alliance with other OPEC members was weakening, but Sunday’s move shows the cooperation is still strong.

The Saudi energy ministry said in a statement that the kingdom’s voluntary cut was a precautionary measure aimed at supporting the stability of the oil market.