Canadian retail sales up 0.7% to $61.8-billion in August; estimate suggests drop in September

Statistics Canada says retail sales rose 0.7 per cent to $61.8-billion in August.

However, the agency says its preliminary estimate for September suggests retail sales fell 0.5 per cent for that month, though it cautioned the figure would be revised.

Retail sales in August rose in six of the 11 subsectors.

Sales at food and beverage stores gained 2.4 per cent for the month, while sporting goods, hobby, book and music stores added 5.0 per cent. Sales at motor vehicle and parts dealers rose 0.6 per cent.

Core retail sales – which exclude gasoline stations and motor vehicle and parts dealers – increased 0.9 per cent.

In volume terms, Statistics Canada says retail sales gained 1.1 per cent in August.

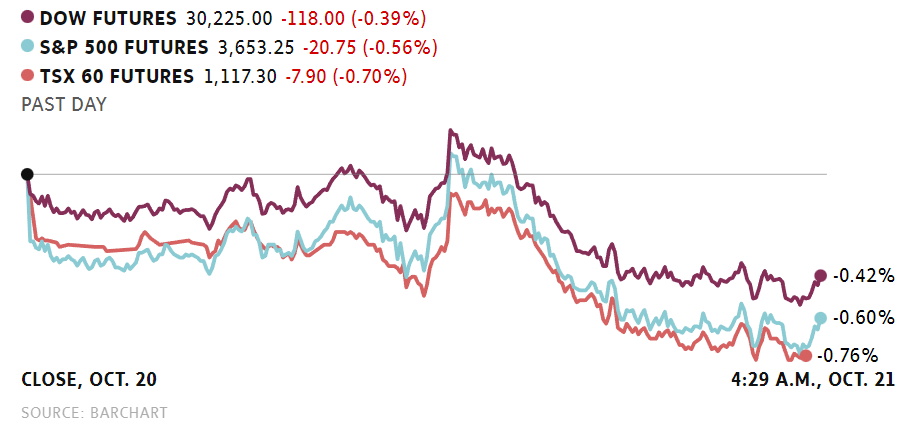

Wall Street futures were down early Friday but key indexes still looked set for weekly gains with corporate earnings and rate concerns high on the agenda. Major European markets were lower with continued political uncertainty in the U.K. in the spotlight. TSX futures were also underwater.

In the early premarket period, futures tied to the Dow, S&P 500 and Nasdaq were all in the red after two straight sessions of losses. However, all three were up roughly 2 per cent on the week thanks to solid gains on Monday and Tuesday. The S&P/TSX Composite Index ended Thusday’s session down 0.51 per cent, reversing gains seen early in the day.

“Once again, few market participants want to hold risk into a weekend with U.S. Treasury 10-year through 4.25 per cent for the first time since 2008,” Stephen Innes, managing partner with SPI Asset Management, said.

“U.S. equities are tormented into the weekend by Federal Reserve officials reigniting fears of stricter monetary tightening and the possibility of a worldwide recession.”

He noted Philadelphia Fed chief Patrick Harker said Thursday that the central bank would likely raise rates to “well above” 4 per cent this year and hold them at restrictive levels, renewing worries about the broader impact of higher borrowing costs.

In this country, investors will get August retail sales figures ahead of the start of trading.

“Our economists don’t expect August retail sales to deviate significantly from Statscan’s preliminary estimate of a 0.4-per-cent month-over-month increase,” Elsa Lignos, global head of FX strategy, said.

“Actual sales volume was likely stronger than that, given offsets from lower prices at gas stations during the month. Sales in September however are expected to flatten out a bit more, according to data from RBC’s own debit and credit spending tracker.”

On the earnings front, Canadian markets will get results from Corus Entertainment. On Wall Street, Verizon is among the big companies reporting.

Overseas, the pan-European STOXX 600 was down 1.52 per cent. Britain’s FTSE 100 fell 0.78 per cent in morning trading as markets now await the outcome of a leadership contest after Prime Minister Liz Truss announced her resignation on Thursday.

Germany’s DAX fell 1.6 per cent. France’s CAC 40 was off 1.7 per cent.

In Asia, Japan’s Nikkei closed down 0.43 per cent. Hong Kong’s Hang Seng lost 0.42 per cent.

Commodities

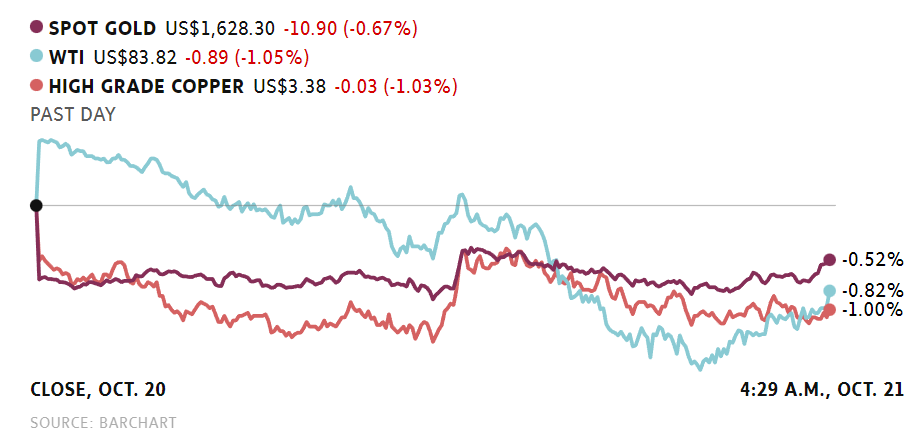

Crude prices were lower as continued concerns about high interest rates and the potential for a global recession offset optimism over reports of easing COVID-19 restrictions in China.

The day range on Brent was US$91 to US$93.06 in the early premarket period. The range on West Texas Intermediate was US$83.15 to US$85.19. Both benchmarks were on track for weekly declines heading into Friday’s session.

“It has been a noisy headline week in the oil patch, but price action has been relatively contained,” SPI Asset Management’s Stephen Innes said in a note.

“There is a feeling of not wanting to fight the Fed until November across many assets, keeping risk-taking grounded.”

Markets drew some support this week from a report that China could soon ease the quarantine period for incoming visitors, easing some concerns over the government’s zero-COVID policy. The reports have not been confirmed by China.

In other commodities, gold prices were lower and looked set for a second consecutive weekly loss.

Spot gold shed 0.4 per cent to US$1,620.79 per ounce by early Friday morning. Gold prices have fallen 1.3 per cent this week.

U.S. gold futures fell 0.7 per cent to US$1,624.60

Currencies

The Canadian dollar was down amid weaker crude prices and negative risk sentiment while its U.S. counterpart edged higher against global currencies and bond yields hit a new 14-year high.

The day range on the loonie was 72.30 US cents to 72.67 US cents in the predawn period.

Investors get August retail sales figures today but markets are now focused on next week’s Bank of Canada rate decision with economists now expecting either a half or three quarter point rate increase.

On world markets, the U.S. dollar index, which tracks the greenback against six major counterparts, advanced 0.2 per cent to 113.130 while the yield on the U.S. 10-year note pushed to a a more than 14-year top of 4.272 per cent by early Friday, according to figures from Reuters.

Britain’s pound fell 0.8 per cent to a weekly low of US$1.11535 as Britain’s ruling Conservative party scrambles to replace Prime Minister Liz Truss.

The euro, meanwhile, fell 0.2 per cent to US$0.97705, after hitting an overnight high of US$0.98455, Reuters reported.

CRA delays cause tax battle to continue for more than 20 years

Last week, I shared examples of how the culture at the Canada Revenue Agency has gone wrong. I referred to an investment that has left the investors – over 2,300 of them – fighting the CRA for more than 20 years. Some investors have passed away during this time, leaving their surviving spouses – widows in many cases – to deal with the CRA in their twilight years. Others have literally grown old waiting for a resolution, which they thought was at hand several years ago.

I’m talking about the Sentinel Hill film investment, which raised funds to promote film production in Canada. At the time, promoting film production was a key policy objective for the government. Investors expected good after-tax returns, provided in part by tax savings from deductible business losses that were to be available to investors. Ken Gordon, one of the four principals of Sentinel Hill Ventures Corp. (SHVC), the architect of the Sentinel Hill investment, obtained advance tax rulings from the Canada Revenue Agency for film investments offered in both the years 2000 (known as SH2000) and 2001 (SH2001).

As an aside, an advance tax ruling (ATR) is a written ruling from the CRA that requires the taxpayer to provide extensive details of a strategy that the taxpayer is contemplating, in order to gain the CRA’s written confirmation of the tax consequences of the strategy prior to implementation.

Mr. Gordon and SHVC wanted to assure investors in SH2000 that the tax implications would be as expected. And so, he requested, and the CRA did issue, an ATR on Feb. 21, 2000. The ATR suggested the tax benefits would be available to investors assuming certain conditions were met. Despite those conditions being met, CRA challenged the amounts claimed by investors.

“Some of the threats and allegations made by CRA were egregious,” Mr. Gordon said. “Only the threat of an appearance in court caused the CRA to discuss a settlement – which was reached in 2004,″ he continued. After three years of fighting, investors did receive 91 per cent of the amounts claimed and that were supported by the ATR issued by the CRA. “At that point, we just wanted the battle over with, so we agreed to settle on 91 per cent of the tax benefits we expected, even though we should have received 100 per cent,” Mr. Gordon said.

In the meantime, before the battle over SH2000 began, a second ATR was issued, and more funds were raised for film productions through the 2001 Sentinel Hill film investment (SH2001). The 2001 deal was structured in an identical manner to SH2000, so investors expected that the tax implications would be the same as SH2000 based on the ATRs that had been issued.

Mr. Gordon and SHVC did not want to continue promoting the SH2001 film investment if CRA had concerns about it. “We met with the audit division of CRA on two occasions and had other discussions with the CRA Rulings department in 2001. We met on Sept. 11, 2001 – that’s right, the 9/11 date many of us remember for the terrorist attacks – and CRA said that they had no concerns about SH2001 as it was structured. It turns out that this was false, but the CRA did not communicate any concerns to us.”

Over the next three years, there was silence from the CRA. It should be noted that, after three years following the date on a Notice of Assessment, an individual’s tax return generally becomes statute-barred, which means the CRA can’t typically reassess a person beyond that date (unless there’s been misrepresentation or gross negligence). On the eve of the three-year anniversary for many of the SH2001 investors, in March, 2005, the CRA issued Notices of Determination to the SH2001 partnership (but not to individual investors) essentially denying 40 per cent of the amounts claimed three years earlier.

SHVC, on behalf of the SH2001 partnership, filed Notices of Objection in June, 2005, objecting to the CRA’s position and to protect the interests of the 2,300 investors, but the CRA failed to appoint an appeals officer to review the objections. “We waited four years for CRA to assign an appeals officer, but they never did. There was silence. So, in July, 2009, we filed a Notice of Appeal that would allow our case to be heard at the Tax Court of Canada,” Mr. Gordon said.

When a taxpayer files a Notice of Appeal, the CRA is forced to deal with the matter more quickly because, otherwise, the department will have to prepare for an appearance in court. So, after filing the Notice of Appeal, SH2001 and its investors finally had CRA’s ear.

But the story isn’t over. There is much to be learned from this story, both about tax planning and, importantly, about the culture at the CRA. I’ll finish the story next time.

Tim Cestnick, FCPA, FCA, CPA(IL), CFP, TEP, is an author, and co-founder and CEO of Our Family Office Inc. He can be reached at tim@ourfamilyoffice.ca.

Meanwhile, EU leaders are still debating how to tackle the bloc’s energy crisis as they meet in Brussels, after Germany gave the green light for discussions around a price cap.

The Stoxx 600 is 1.5% down mid-morning, while all sectors and major bourses are in the negative. Retail leads losses, down 4%, followed by construction at 2.4% and household goods at 2.2%.

Japanese yen hits 150 against the U.S. dollar; Asia-Pacific markets lower (Oct 20)

Shares in the Asia-Pacific traded lower on Thursday as economic fears weigh.

The Japanese yen weakened past 150 per U.S. dollar late in Asia’s afternoon, a 32-year low against the greenback. It last traded at 149.85 per dollar.

The Hang Seng index in Hong Kong pared some of its earlier losses and traded 1.33% lower in the final hour of trade after dipping 3%, hitting its lowest level since May 2009. The Hang Seng Tech index was 2.08% lower.

In Japan, the Nikkei 225 lost 0.92% to 27,006.96 and the Topix shed 0.51% to 1,895.41. The S&P/ASX 200 in Australia declined 1.02% to 6,730.70.

South Korea’s Kospi dipped 0.86% to 2,218.09 and the Kosdaq was 1.47% lower at 680.44. The MSCI’s broadest index of Asia-Pacific shares outside Japan was down 0.87%.

The Nasdaq Composite shed 0.85% to close at 10,680.51, while the S&P 500 declined 0.67% to 3,695.16. The Dow Jones Industrial Average lost 99.99 points, or 0.33%, to finish the day at 30,423.81.

UK Prime Minister Liz Truss resigns after less than 2 months in office

Prime Minister Liz Truss resigned Thursday after less than two months in office amid pressure following a reversal of economic policies that led to economic instability.

Truss made the announcement a day after she defiantly declared that she is “a fighter and not a quitter.” Ultimately, however, she said that circumstances have changed.

“Given the situation, I cannot deliver the mandate on which I was elected by the Conservative Party,” Truss said. I have therefore spoken to His

Majesty the King to notify him that I am resigning as leader of the Conservative Party.”

PM Trudeau, Poilievre spar over recession concerns, affordability bill

OTTAWA –

Prime Minister Justin Trudeau and Conservative Leader Pierre Poilievre sparred in the House of Commons on Tuesday over concerns of a looming recession and how the federal government should be tackling inflation, with Trudeau accusing Poilievre of “blocking” the Liberals’ bill to implement housing and dental benefits.

Tuesday’s Question Period saw a back-and-forth between Trudeau and Poilievre, with the Conservative leader accusing Trudeau of “bragging about” the $500 top-up for low-income renters as part of the proposed affordability legislation, while adding “these days, you can’t even rent a dog house in the backyard for that kind of money.”

He, along with several other Conservative MPs, also repeatedly called on the government to end its plans to “triple, triple, triple” the carbon tax.

“It is not a luxury to heat your home in Canada in the winter time, yet the prime minister wants to punish people for doing it,” Poilievre said.

“If he’s not going to back down on his plan to triple the tax, will at least he have the decency to exempt home heating this winter from that tax hike?” he added.

In response, Trudeau said that if Conservatives cared about affordability for Canadians, they would be backing and not blocking Bill C-31. It was a line of attack he repeated throughout the day, starting first in remarks to reporters on his way into a cabinet meeting on Tuesday morning.

“If (Poilievre) actually wanted to support low-income families, he’d step up and support our measures to give more money to low-income families for the cost of dental care to their kids, or to help the 1.8 million Canadians who will benefit from our additional help on the housing benefit,” Trudeau said in the House.

“Not only does the leader of the Opposition not support those measures to help low-income families with real money this fall, he’s blocking their passage in the House, preventing anyone from getting that money,” he added.

Many experts are forecasting a recession, with economists from the Royal Bank of Canada saying last week it’s expected as soon as early 2023.

The Liberals’ Bill C-31 — to provide dental-care benefits for children under 12, and a one-time rental housing benefit for eligible Canadians — has remained at second reading in the House of Commons since it was tabled on Sept. 20.

In a move to see the bill fast-tracked through remaining stages by the end of next week, the government has advanced a motion that would see MPs burning the midnight oil to wrap up their work on the 36-page legislation and pass it into the Senate. The Conservatives and Bloc Quebecois are opposing the government’s attempts to expedite the bill, suggesting more study and consideration is needed on the government’s spending plans.

The Liberals promised to focus on affordability and the rising cost of living this fall by passing two pieces of legislation: Bill C-30 to temporarily double the GST credit, which passed through the Senate and received Royal Assent on Tuesday, and the dental and housing benefit bill. Connected to the Liberal-NDP supply-and-confidence deal, there is some urgency from the government benches, as Trudeau pledged to the NDP that the government would get both cost-of-living bills passed into law, and the benefits out to eligible Canadians, before the end of the year.

While the NDP is helping the Liberals advance Bill C-31, getting in on the affordability conversation during question period NDP Leader Jagmeet Singh accused the Liberals of having no plan to deal with a looming recession, especially when it comes to employment insurance and support for Canadians who may lose their jobs.

Oil up in tight market as U.S. sets release of more reserves

Oil prices rose on Wednesday as caution over tightening supply countered the negative impact of uncertain demand, and news that the United States will release more crude from its reserves.

Brent crude futures for December settlement ended up $2.38, or 2.6%, to $92.41 a barrel. U.S. West Texas Intermediate crude (WTI) for November, which is expiring on Thursday, ended at $85.55 a barrel, up $2.73, or 3.3%.

“Realistically an SPR release is near-term bearish, long-term bullish because eventually you’re going to have to buy it back,” said Gary Cunningham, director of market research at Tradition Energy. “Overall the market continues to swing wildly and chop around on erratic news.”

In the previous session, the benchmarks hit a two-week low after U.S. President Joe Biden said he plans to release 15 million barrels of oil from the Strategic Petroleum Reserve (SPR).

Biden, in remarks Wednesday, noted U.S. plans to repurchase oil for the reserve if prices fall enough. The reserve release would be the last sale from the planned sale of 180 million barrels of oil announced shortly after Russia invaded Ukraine in February.

Oil prices have rallied since the Organization of the Petroleum Exporting Countries agreed to reduce its production target by roughly 2 million barrels a day – though that is expected to only include about 1 million barrels of actual output declines.

“They want Brent around $90, so they’re going to get it and going to continue to cut output to hold that number,” Cunningham said.

U.S. crude inventories fell unexpectedly last week – down 1.7 million barrels, weekly government showed, against expectations for a build of 1.4 million barrels. SPR levels fell 3.6 million barrels to just over 405 million, the lowest since May 1984.

A pending European Union ban on Russian crude and oil products and the output cut from the Organization of the Petroleum Exporting Countries and other producers including Russia, a group known as OPEC+, of 2 million barrels per day also supported prices.

The EU’s sanctions on Russian crude takes effect in December, and sanctions on oil products will take effect in February.

Canadian dollar pares decline as hot inflation bolsters rate hike bets

The Canadian dollar CADUSD +0.14%increase weakened against its U.S. counterpart on Wednesday as investor sentiment soured, but the currency’s decline was capped as hot domestic inflation data led to raised bets on another jumbo interest rate hike by the Bank of Canada.

Canada’s annual inflation rate inched down to 6.9 per cent in September, Statistics Canada data showed.

That was the third consecutive monthly deceleration but a notch ahead of analyst forecasts of 6.8 per cent, while measures of underlying price pressures failed to ease.

Money markets see a 66 per cent chance that the Bank of Canada would raise interest rates by three-quarters of a percentage point at its next policy decision on Oct. 26, up from about 30 per cent before the data.

U.K. inflation was also hot, which pressured global financial markets and helped drive gains for the safe-haven U.S. dollar against a basket of major currencies.

The Canadian dollar was down 0.2 per cent at 1.3770 to the greenback, or 72.62 U.S. cents, after trading in a range of 1.3719 to 1.3800.

Meanwhile, U.S. crude oil prices were up 0.7 per cent at $83.37 a barrel as bullish signals like falling U.S. crude stocks were countered by bearish factors such as uncertain Chinese demand growth. Oil is one of Canada’s major exports.

Canadian government bond yields were higher across the curve, tracking the move in U.S. Treasuries. The 10-year rose 11.8 basis points to 3.474 per cent, approaching the top of its range since June.