Markets face what could be the most important week of summer with Fed, earnings and economic data

- The busiest — and what could be the most important — week of the summer is coming up, with the Federal Reserve expected to deliver another three-quarter point rate hike.

- Second-quarter GDP and other economic reports could provide more clues as to whether the economy is heading for recession, and earnings are expected from Apple, Microsoft, and Alphabet, among others.

- “For me, the real tell will be whether the attitude of investors continues to be that the earnings season is better than feared,” said one strategist.

There’s a head-spinning amount of news for markets to navigate in the week ahead, the biggest of which will be the Federal Reserve’s midweek meeting.

The two largest U.S. companies — Microsoft and Apple — report Tuesday and Thursday, respectively. Google parent Alphabet releases results Tuesday, and Amazon reports Thursday. Meta Platforms, formerly Facebook, reports Wednesday. In all, more than a third of the S&P 500 companies are reporting.

On top of that are several hefty economic reports, which should add fuel to the debate on whether the economy is heading toward, or is already in, a recession.

“Next week, I think, is going to be the most important week of the summer between the economic reports coming out, with respect to GDP, the employment cost index and the Fed meeting — and the 175 S&P 500 companies reporting earnings,” said Leo Grohowski, chief investment officer at BNY Mellon Wealth Management.

Second-quarter gross domestic product is expected Thursday. The Fed’s preferred personal consumption expenditures inflation data comes out Friday morning, as does the employment cost index. Home prices and new home sales are reported Tuesday and consumer sentiment is released Friday.

“I think what those bigger companies say about the outlook will be more important than the earnings they post. … When you combine that with the statistical reports, which will be backward looking, I think it’s going to be a volatile and important week,” Grohowski said.

The run-up to the Fed’s meeting on Tuesday and Wednesday has already proven to be dramatic, with traders at one point convinced a full point rate hike was coming. But Fed officials pushed back on that view, and economists widely expect a second three-quarter point hike to follow the one last month.

“Obviously a 75 basis point hike is baked in the cake for next week,” said Grohowski. “I think the question is what happens in September. If the Fed is continuing to stay too tight for too long, we will need to increase our probability of recession, which currently stands at 60% over the next 12 months.” A basis point equals 0.01%.

The Fed’s rate hiking is the most aggressive in decades, and the July meeting comes as investors are trying to determine whether the central bank’s tighter policies have already or will trigger a recession. That makes the economic reports in the week ahead all the more important.

GDP report

Topping the list is that second-quarter GDP, expected to be negative by many forecasters. A contraction would be the second in a row on top of the 1.6% decline in the first quarter. Two negative quarters in a row, when confirming declines in other data, is viewed as the sign of a recession.

The widely watched Atlanta Fed GDP Now was tracking at a decline of 1.6% for the second quarter. According to Dow Jones, a consensus forecast of economists expects a 0.3% increase.

“Who knows? We could get a back-of-the-envelope recession with the next GDP report. There’s a 50/50 chance the GDP report is negative,” Grohowski said. “It’s the simple definition of two down quarters in a row.” He added, however, that would not mean an official recession would be declared by the National Bureau of Economic Research, which considers a number of factors.

Diane Swonk, chief economist at KPMG, expects to see a decline of 1.9%, but added it is not yet a recession because unemployment would need to rise as well, by as much as a half percent.

“That’s two negative quarters in a row, and a lot of people are going to say ‘recession, recession, recession,’ but it’s not a recession yet,” she said. “The consumer slowed quite a bit during the quarter. Trade remains a huge problem and inventories were drained instead of built. What’s interesting is those inventories were drained without a lot of discounting. My suspicion is inventories were ordered at even higher prices.”

Stocks in the past week were higher. The S&P 500 ended the week with a 2.6% gain, and the Nasdaq was up 3.3% as earnings bolstered sentiment.

“We’re really shifting gears in terms of what’s going to be important next week versus this week,” said Art Hogan, chief market strategist at National Securities. “We really had an economic data that was largely ignored. Next week, it will probably equal the attention we pay to the household names that are reporting.”

Better-than-expected earnings?

Companies continued to surprise on the upside in the past week, with 75.5% of the S&P 500 earnings better than expected, according to I/B/E/S data from Refinitiv. Even more impressive is that the growth rate of earnings for the second quarter continued to grow.

As of Friday morning, S&P 500 earnings were expected to grow by 6.2%, based on actual reports and estimates, up from 5.6% a week earlier.

“We have kind of a perfect storm of inputs, pretty deep economic reports across the board, with things that have become important, like consumer confidence and new home sales,” said Hogan “For me, the real tell will be whether the attitude of investors continues to be that the earnings season is better than feared.”

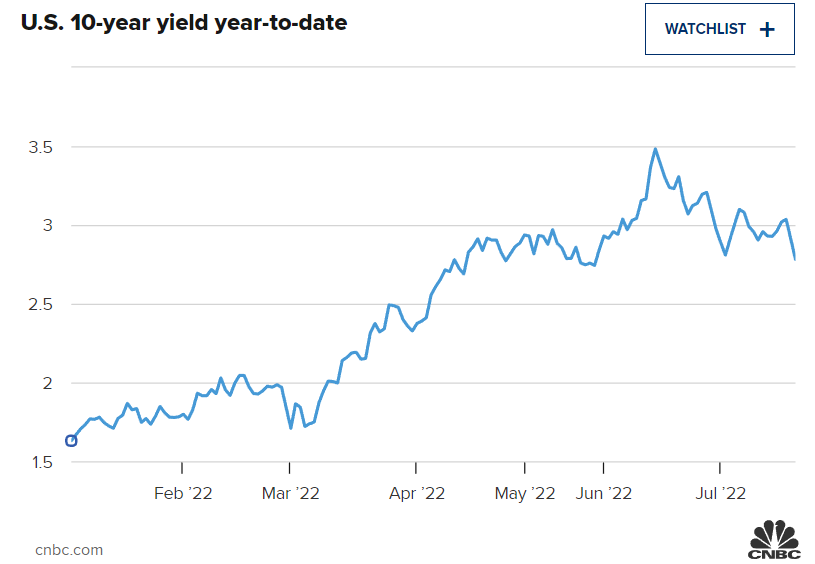

While stocks gained in the past week, bond yields continued to slide, as traders worried about the potential for recession. The benchmark 10-year Treasury yield fell to 2.76% Friday, after weaker PMIs in Europe and the U.S. sent a chilling warning on the economy. Yields move opposite price.

“I do think the market is pivoting,” said Grohowski. “I do think our concerns at least are quickly shifting from persistent inflation to concerns over recession.”

The potential for volatility is high, with markets focused on the Fed, earnings and recession worries. Fed Chair Jerome Powell could also create some waves, if he is more hawkish than expected.

“There are a lot of signs out there about slowing economic growth that will bring down inflation. Hopefully, the Fed doesn’t stay too tight for too long,” said Grohowski. “The chance of a policy error by the Fed continues to increase because we continue to get signs of a rapidly cooling — not just cooling — economy.”