July 12 -The close: TSX hits 16-month low as energy stocks tumble

Canada’s main stock index fell on Tuesday to its lowest level in 16 months as crude oil prices tumbled more than 7% and the U.S. yield curve inverted the most since March 2010, further signals that global investors are bracing for a possible recession.

Wall Street also ended in negative territory as recession jitters kept buyers out of the equities market ahead of a key U.S. inflation report. The data could help guide expectations for further aggressive interest rate hikes by the Federal Reserve.

“For several months we’ve swung back and forth between inflation fears and recession fears, almost on a daily basis,” said Brent Schutte, chief investment officer at Northwestern Mutual Wealth Management Company, in Milwaukee, Wisconsin. “We have really confused investors who have chosen to go on a buyers strike,” Schutte added. “I don’t hear many people saying ‘buy the dip.’”

While the U.S. CPI report is expected to show inflation gathered heat in June, the so-called “core” CPI, which strips away volatile food and energy prices, is seen offering further confirmation that inflation has peaked, which could potentially convince the Federal Reserve to ease on its policy tightening in autumn.

Paul Kim, chief executive officer at Simplify ETFs in New York, expects year-on-year topline CPI to “be in the high eight or potentially even nine percentage range, and with inflation that high, the Fed has only one thing in mind.”

Worries that overly aggressive moves by the Fed to reign in decades-high inflation could push the economy over the brink of recession were exacerbated by the steepest inversion of the 2 year and 10 year Treasury yields since at least March 2010.

The market expects the central bank to raise the key Fed funds target rate by 75 basis points at the conclusion of its July policy meeting, which would mark its third consecutive interest rate hike.

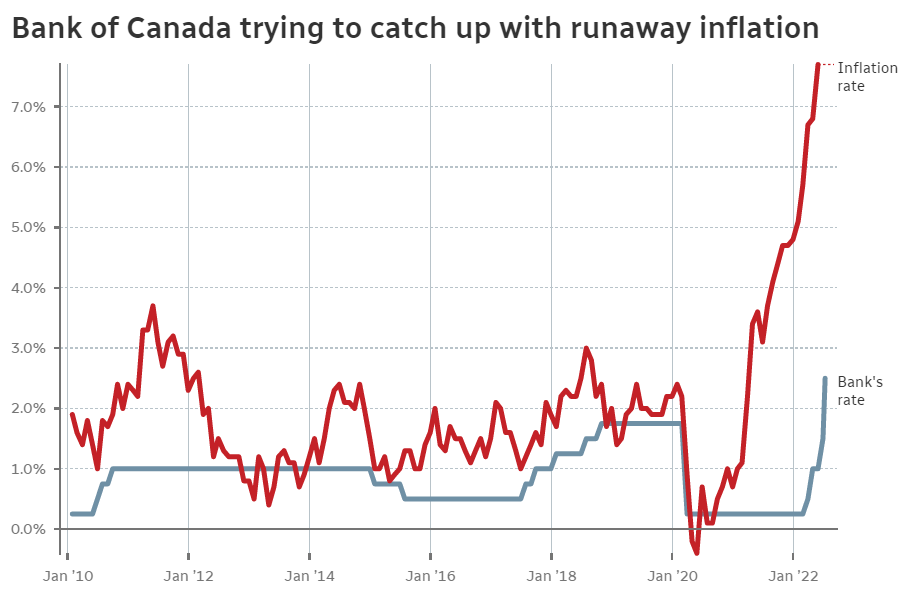

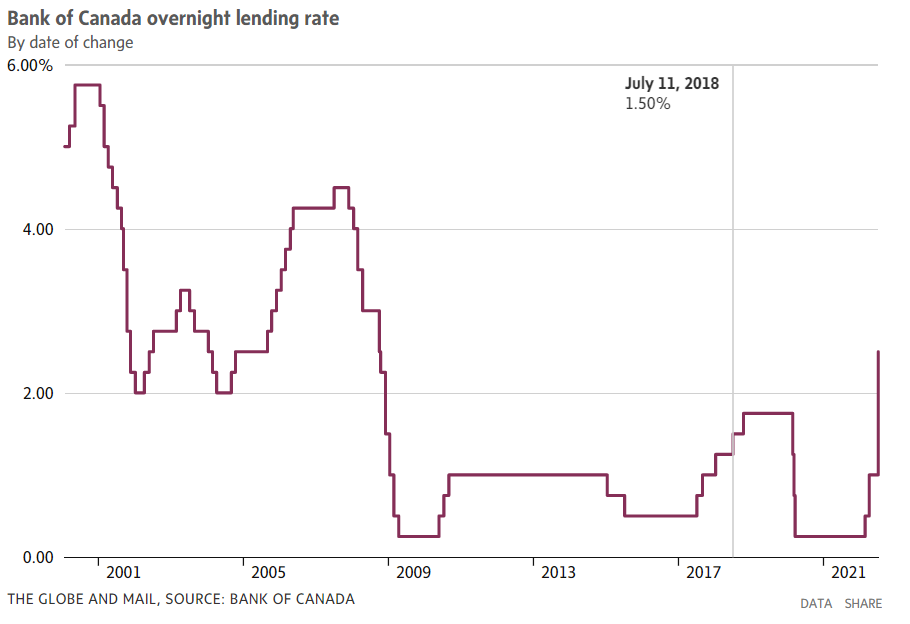

Canada’s central bank is expected to tighten by three-quarters of a percentage point on Wednesday, which would be its biggest hike in 24 years.

The Toronto Stock Exchange’s S&P/TSX composite index ended down 138.16 points, or 0.7%, at 18,678.64, its lowest closing level since March 2021.

The energy sector fell 3.4% as U.S. crude prices settled 7.9% lower at $95.84 a barrel, with demand-sapping COVID-19 curbs in top crude importer China adding to fears of a global economic slowdown.

Oil prices are facing extreme pressure “as a defensive posture continues with consumer sentiment still in a depressed mode along with a COVID re-surface in China,” said Dennis Kissler, senior vice president for trading at BOK Financial.

A record high dollar is triggering more selling liquidation, Kissler added. Oil is generally priced in U.S. dollars, so a stronger greenback makes the commodity more expensive to holders of other currencies.

The dollar index, which tracks the currency against a basket of six counterparts, on Tuesday climbed to 108.56, its highest level since October 2002. Investors tend to view the dollar as a safe haven during market volatility.

Investors have been dumping petroleum-related derivatives at one of the fastest rates of the pandemic era as recession fears intensify. Hedge funds and other money managers sold the equivalent of 110 million barrels in the six most important petroleum-related futures and options contracts in the week to July 5.

The Dow Jones Industrial Average fell 192.51 points, or 0.62%, to 30,981.33, the S&P 500 lost 35.63 points, or 0.92%, to 3,818.8 and the Nasdaq Composite dropped 107.87 points, or 0.95%, to 11,264.73.

All 11 major sectors in the S&P 500 fell, with energy shares suffering the largest percentage loss.

The second-quarter reporting season will hit full stride later in the week as JPMorgan Chase & Co, Morgan Stanley , Citigroup and Wells Fargo & Co post results.

As of Friday, analysts saw aggregate annual S&P earnings growth of 5.7% for the April to June period, down from the 6.8% forecast at the beginning of the quarter, according to Refinitiv.

PepsiCo got the ball rolling this week by beating its quarterly earnings estimates and announced it could increase prices amid resilient demand.

Shares of Boeing Co jumped 7.4% after the plane maker’s June aircraft deliveries hit the highest monthly level since March 2019.

That news, along with falling energy prices, helped the S&P 1500 Air Lines index rise 6.1%.

Apparel retailer Gap Inc fell 5.0% following its announcement that its CEO would step down, and that margins would stay under pressure in the second quarter due to input costs.

Software provider Service Now plunged 12.7% after its CEO’s remarks about macro headwinds and currency pressures. Other software companies, including Salesforce.com, Paycom Software, Intuit and Microsoft, were also down.

Declining issues outnumbered advancing ones on the NYSE by a 1.37-to-1 ratio; on Nasdaq, a 1.19-to-1 ratio favored decliners. The S&P 500 posted one new 52-week high and 30 new lows; the Nasdaq Composite recorded 13 new highs and 145 new lows. Volume on U.S. exchanges was 9.86 billion shares, compared with the 12.79 billion average over the last 20 trading days.

In credit markets, the Canadian government bond yields were lower across the curve, tracking the move in U.S. Treasuries. The 10-year yield eased 5.7 basis points to 3.187%.