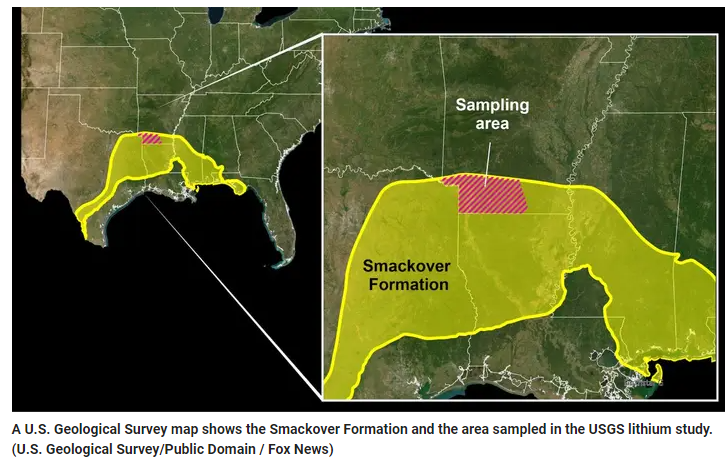

A new study led by the U.S. Geological Survey (USGS) found a large amount of lithium reserves in southwestern Arkansas that could help meet rising demand for lithium in electric vehicle car batteries.

USGS worked with the Arkansas Department of Energy and the Environment’s Office of the State Geologist to examine a geological unit known as the Smackover Formation to determine the amount of lithium in brines that are co-produced during oil and gas exploration.

The study estimated that there are between 5 million and 19 million tons of lithium reserves present in the formation. While that estimate was of the amount of lithium in place and didn’t assess how much of that is technically recoverable, if the reserves can be recovered commercially, the low-end estimate of 5 million tons would be enough to meet the world’s projected 2030 demand for lithium batteries in electric vehicles nine times over.

Lithium is a critical mineral that has seen global demand surge in recent years, a trend that’s expected to continue as the transition from fossil fuels to electric and hybrid vehicles accelerates in the years ahead given its use in rechargeable EV batteries. The mineral is also used in the production of glass and aluminum products, and it can be found in portable electronic devices, electric tools and has energy grid storage applications.

“Our research was able to estimate total lithium present in the southwestern portion of the Smackover in Arkansas for the first time. We estimate there is enough dissolved lithium present in that region to replace U.S. imports of lithium and more,” said Katherine Knierim, a hydrologist and the study’s principal researcher.

“It is important to caution that these estimates are an in-place assessment. We have not estimated what is technically recoverable based on newer methods to extract lithium from brines,” Knierim added.

USGS used machine learning, a type of artificial intelligence (AI), to analyze samples from the Smackover Formation that it compared against USGS databases of samples of brines and water from hydrocarbon production.

The machine learning model then used that data to predict lithium concentrations across the region and generate maps, even of areas from which lithium samples haven’t been collected.

“Lithium is a critical mineral for the energy transition, and the potential for increased U.S. production to replace imports has implications for employment, manufacturing and supply-chain resilience. This study illustrates the value of science in addressing economically important issues,” said USGS Director David Applegate.

The U.S. currently imports more than 25% of its lithium. A USGS report noted that from 2019 to 2022, U.S. lithium imports came primarily from Argentina (51%) and Chile (43%), with notably smaller amounts imported from China (3%) and Russia (2%).

Australia’s lithium mines were the world’s most productive, followed by Chile and China, per the USGS report. The world’s largest lithium reserves were Chile with 9.3 million tons, Australia with 6.2 million tons, Argentina with 3.6 million tons and China with 3 million tons, according to the January 2024 report. For comparison, U.S. reserves were 1.1 million tons of lithium.

Measured and indicated lithium resources in the report were 14 million tons for the U.S., less than Bolivia’s 23 million tons and Argentina’s 22 million tons, though that figure exceeded Chile’s 11 million tons, Australia’s 8.7 million tons and China’s 6.8 million tons.

The USGS report noted that around the world, lithium’s main end use is for batteries (87%), followed by ceramics and glass (4%), lubricating greases (2%), air treatment (1%), continuous casting mold flux powders (1%), medical (1%) and other uses (4%).