(8:30 a.m. ET) U.S. goods trade deficit for February.

(8:30 a.m. ET) U.S. wholesale and retail inventories for February.

(9 a.m. ET) U.S. CoreLogic Case-Shiller Home Price Index (20 city) for January. The Street expects a decline of 0.5 per cent from December but up 2.5 per cent year-over-year.

(9 a.m. ET) U.S. FHFA House Price Index for January. Consensus is a drop of 3.0 per cent month-over-month but a rise of 4.9 per cent year-over-year.

(10 a.m. ET) U.S. Conference Board Consumer Confidence Index for March.

(10 a.m. ET) U.S. Fed Vice Chair for Supervision Michael Barr testifies before the Senate Banking Committee.

Apple CEO Tim Cook on Saturday used his first public remarks on his visit to China to praise the country for its rapid innovation and its long ties with the U.S. iPhone maker, according to local media reports.

Cook is in Beijing to attend the China Development Forum, a government-organized event being held again in full force after the country ended its Covid controls late last year.

Besides Cook, the event is being attended by senior government officials as well as CEOs of firms such as Pfizer and BHP.

“Innovation is developing rapidly in China and I believe it will further accelerate,” Cook was quoted by The Paper news outlet as saying.

His visit comes at a time of rising tensions between Beijing and Washington and as Apple has been looking to reduce its supply chain reliance on China and moving production to new up and coming centres such as India.

Last year, production at the world’s largest iPhone factory run by Apple supplier Foxconn was heavily disrupted after China’s zero-Covid policies fueled worker unrest.

Cook also visited an Apple Store in Beijing on Friday, pictures of which went viral on Chinese social media.

During his speech, Cook also discussed education and the need for young people to learn programming critical thinking skills, announcing that Apple plans to increase spending on its rural education programme to 100 million yuan, the local media reports said.

PUBLISHED FRI, MAR 24 20236:53 AM EDTUPDATED FRI, MAR 24 20233:07 PM EDT

Gold prices ended a volatile week higher on Friday as bank contagion fears bolstered both safe-haven demand and bets on a pause in Federal Reserve rate hikes, adding to the appeal of zero-yield bullion.

U.S. gold futures lost 0.6% to settle at $1,983.80 per ounce. Futures also gained 0.5% for the week, having climbed to its highest level in a year above $2,000 on Monday.

Banking shares were trounced again on Friday, with European giants Deutsche Bank and UBS knocked by worries that regulators and central banks have yet to contain the worst shock to the sector since the 2008 financial crisis.

PUBLISHED THU, MAR 23 202311:17 PM EDTUPDATED FRI, MAR 24 20232:53 PM EDT

Oil prices fell Friday amid declining European banking shares and after U.S. Energy Secretary Jennifer Granholm said refilling the country’s Strategic Petroleum Reserve (SPR) may take several years, dampening demand prospects.

Brent crude fell 95 cents, or 1.3%, to $74.96 a barrel, while West Texas Intermediate U.S. crude futures fell 74 cents, or 1.1%, to $69.22 a barrel.

Both benchmarks, which fell over 4% earlier in the session, were on track to end the week higher, after posting their biggest weekly declines in months last week due to banking sector turmoil and worries about a possible recession.

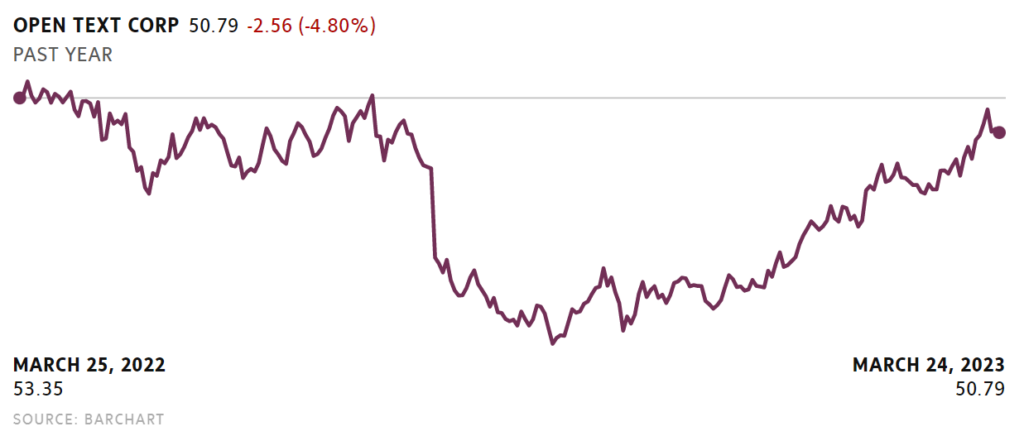

Tuesday’s TSX breakouts: This dividend stock has staged a sharp recovery, forming a bullish ‘golden cross’

Discussed today is a stock that is on the positive breakouts list – Open Text Corp. (OTEX-T -0.53%decrease). Last year, the stock price was in a downtrend. However, in 2023, the share price has rebounded. Year-to-date, the share price has rallied 28 per cent, making it the seventh best performing stock in the S&P/TSX composite index.

This growth stock has an attractive business model with high recurring revenues, high margins, and strong cash flow generation. On a valuation basis, the stock is trading at a discount to its historical average multiple. Management is committed to returning capital to its shareholders, boosting its dividend every calendar year since 2014. The current dividend yield is 2.6 per cent.

A brief outline on Open Text is provided below that may serve as a springboard for further fundamental research when conducting your own due diligence.

Barchart

The company

Waterloo, Ont.-based Open Text is a leading software and services provider of information management solutions. The company’s software helps its customers automate processes and manage supply chains.

Open Text has strong earnings visibility given its high recurring revenue business model. In the second quarter of fiscal 2023 (the company’s fiscal year-end is June 30), total annual recurring revenue (cloud services and subscriptions and customer support) represented 81 per cent of total revenue. Cloud services and subscription revenue alone represented over 45 per cent of total revenue.

In terms of geographic revenue breakdown, in fiscal 2022, 62.6 per cent of its revenue was from the Americas, 29.4 per cent from the Europe, Middle East and Africa (EMEA) and 8 per cent from the Asia Pacific region.

In January, the company completed a sizable acquisition, purchasing Micro Focus International plc for approximately $5.8-billion, funded with cash, debt, and drawing on its revolving credit facility. As a result, the company’s net leverage ratio increased to 3.8 times. Management anticipates this ratio will decline to less than 3 times within the next eight full quarters.

There is seasonality in the company’s business with the first-quarter historically the weakest quarter.

The company is dual-listed, trading on the Toronto Stock Exchange as well as the Nasdaq under the ticker, OTEX.

Investment thesis

Strong leadership

Attractive revenue composition (high recurring revenue) and high margins

Robust earnings growth driven by the acquisition of Micro Focus

Diversified customer base

Reasonable valuation – room for multiple expansion

Strong free cash flow generation

Reliable dividend

Dividend policy

The company pays shareholders a quarterly dividend of 24.299 US cents per share, equating to a current annualized yield of 2.6 per cent.

Management remains committed to returning capital to its shareholders and targets returning 20 per cent of its trailing 12-months of free cash flow.

Quarterly earnings and outlook

After the market closed on Feb. 2, the company reported better-than-expected second quarter fiscal 2023 financial results. Revenue came in at US$897-million, up 2.4 per cent year-over-year (or 7.8 per cent year-over-year on a constant currency basis), and ahead of the consensus estimate of US$868-million. Adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) was US$340.9-million, ahead of the Street’s forecast of US$314-million. Adjusted earnings per share came in at 89 US cents, above the consensus earnings per share estimate of 78 US cents.

For the third quarter of fiscal 2023, management guided to revenue of between US$1.18-billion and US$1.22-billion, of which between US$310-million and US$325-million is from Micro Focus.

For fiscal 2023, management is targeting total revenue growth of between 28 per cent and 30 per cent (organic growth of between 1 per cent and 2 per cent), an adjusted EBITDA margin between 32.5 per cent and 33.5 per cent, and free cash flow of between US$500-million and US$600-million. For fiscal 2024, management is targeting total revenue growth of between 33 per cent and 35 per cent (organic growth of between 1 per cent and 2 per cent), an adjusted EBITDA margin of between 36 per cent and 38 per cent, and free cash flow between US$800-million and US$900-million. For fiscal 2026, management is targeting total revenue growth of between 2 per cent and 4 per cent (organic growth of between 2 per cent and 4 per cent), an adjusted EBITDA margin of between 38 per cent and 40 per cent, and free cash flow of over US$1.5-billion.

Analysts’ recommendations

This technology stock is covered by 10 analysts, of which eight analysts have buy recommendations and two analysts (Citi’s Steven Enders and CIBC’s Stephanie Price) have ‘neutral’ recommendations.

The firms providing research coverage on the company are as follows in alphabetical order: ARC Independent Research, Barclays, BMO Nesbitt Burns, CIBC World Markets, Eight Capital, National Bank Financial, Scotiabank, Raymond James, RBC Dominion Securities and TD Securities.

Revised recommendations

Last month, six analysts revised their target prices.

ARC’s Kadambari Daptardar to $50 from $45.

BMO’s Thanos Moschopoulos to US$39 from US$34.

CIBC’s Stephanie Price to US$40 from US$35.

Citi’s Steven Enders to US$35 (the low on the Street) from US$33.

Raymond James’ Steven Li to US$42 from US$48.

TD’s Daniel Chan to US$50 from US$40.

Financial forecasts

The Street is forecasting EBITDA of US$1.435-billion in fiscal 2023 and US$2.14-billion in fiscal 2024. The consensus earnings per share estimates are US$3.06 in fiscal 2023, rising to US$4.43 in fiscal 2024.

Given the recent acquisition of Micro Focus International plc that was completed in January, earnings forecasts have increased materially for fiscal 2024. Three months ago, the consensus EBITDA and EPS estimates were US$1.325-billion and US$3.29, respectively.

Valuation

Analysts commonly value the stock on an enterprise value-to-EBITDA multiple basis.

According to Bloomberg, the stock is trading at an EV/EBITDA multiple of 8.8 times the fiscal 2024 consensus estimate, which is well below the five-year historical average multiple of 11 times.

The average one-year target price is US$44.13, implying the share price may appreciate nearly 17 per cent over the next 12 months.

Insider transaction activity

On Feb. 7, executive vice-president of IT and chief information officer Renee McKenzie sold 2,061 shares at an average price per share of approximately US$34.599 with 4,961 shares remaining in this particular account. Proceeds totaled over US$71,000, not including trading fees.

Chart watch

At the beginning of the month, the stock formed a bullish “golden cross” with the 50-day moving average crossing above the 200-day moving average.

Year-to-date, the share price has rallied 28 per cent, making it the seventh best performing stock out of 235 stocks in the S&P/TSX composite index. Should the positive price momentum continue, the stock faces an initial ceiling of resistance around $55. After that, there is overhead resistance between $62.50 and $63. Looking at the downside, there is strong technical support around $44, near its 200-day moving average (at $44.03).

After coming under pressure early in the session, Canadian stocks showed a significant turnaround over the course of the trading day on Friday.

The benchmark S&P/TSX Composite Index climbed well off its worst levels of the day, eventually closing up 41.57 points or 0.2 percent at 19,501.49.

The early weakness came amid renewed concerns about the health of the banking sector, with U.S.-listed shares of Deutsche Bank (DB) moving sharply lower in early trading amid a spike by the German lender’s credit default swaps.

Credit Suisse (CS) and UBS Group (UBS) also came under pressure after a report from Bloomberg said they are among banks under scrutiny in a Justice Department probe into whether financial professionals helped Russian oligarchs evade sanctions.

UBS’ state-backed acquisition of troubled rival Credit Suisse for 3 billion Swiss francs, or $3.2 billion, helped ease concerns about recent banking industry turmoil earlier in the week.

Selling pressure waned over the course of the session, however, as traders felt the banking concerns may have been overdone amid optimism the Federal Reserve is nearing the end of its tightening cycle

Interest rate-sensitive utilities stocks turned in a strong performance, resulting in a 1.8 percent jump by the S&P/TSX Capped Utilities Index.

Gold stocks also moved notably higher on the day despite a decrease by the price of the precious metal, driving the S&P/TSX Global Gold Index up by 1.5 percent.

On the economic front, a report from Statistics Canada said Canadian retail sales surged 1.4 percent to C$66.4 billion in January.

The increase was led by higher sales at motor vehicle and parts dealers and gasoline stations and fuel vendors

Months of simmering tensions over a nearly $170-million debt owed by Peguis First Nation to failed lender Bridging Finance Inc. have boiled over, with critics in the community accusing the band council of arbitrarily writing down the debt to just $25-million ahead of an April band council election.

The writedown was revealed in financial statements posted last week on the website of Peguis First Nation, raising concerns from its members and accounting experts about whether the writedown disguises the size of the debt facing the community.

Peguis, a First Nation that has a registered population of 11,000 and whose main reserve is located about 190 kilometres north of Winnipeg, has borrowed millions from Bridging.

A Toronto-based lender, Bridging was placed into court-ordered receivership in April, 2021, at the request of the Ontario Securities Commission over allegations that Bridging managers funnelled millions to themselves at investors’ expense.

Receiver PricewaterhouseCoopers Inc. is now working to wind down Bridging operations and recover funds for Bridging investors through negotiations or through legal action, including lawsuits against Peguis.

In December, PwC filed claims in Ontario and Manitoba courts, seeking to recover nearly $170-million in principal and interest owed by Peguis First Nation and related entities.

According to a statement of claim filed Dec. 30, 2022, in the Court of King’s Bench in Manitoba, Peguis in 2017 arranged three separate credit facilities through Bridging: $19-million to build new homes and $3-million to renovate existing ones; $6-million to build two new gas bars in Winnipeg and Selkirk; and $30.6-million to replace credit facilities Peguis previously had with Bank of Montreal.

The amount available through those credit facilities was increased on several occasions at Peguis’s request, according to the statement of claim. As of Dec. 29, 2022, the housing facility was sitting at $58.4-million (including a $40-million mortgage initially issued by BMO); the gas-bar loan was at $6.9-million; and the new credit facility was at $48-million, for a principal balance of$113.4-million. Fees and interest of$56.4-million pushed that total to $169.8-million.

A court action in the Ontario Superior Court of Justice, filed Dec. 30, 2022, claims the same amounts: $113.4-million in principal plus $56.4-million in interest.

In January, news of the Ontario court action began spreading among Peguis members. A dissident group, 269 Silent No More, held a rally and meeting that month in the community of Peguis to highlight the Ontario court action – handing out copies to band members – and to call for more transparency from the chief and council. (269 is Peguis’s band number under the federal Indian Act.)

Then, last week, updated financial statements for the band were posted on the Peguis website.

According to those financial statements, the chief and council sought legal advice in the wake of the receiver’s Manitoba lawsuit to review the documentation and terms of the Bridging loans, including whether the loans complied with provisions of the Indian Act.

Under the Indian Act, on-reserve property and assets are in general protected from seizure by creditors, but those provisions can be waived. Peguis says its legal counsel believes that some of the Bridging loans required Bridging to obtain fresh waivers under the act, as opposed to relying on those previously obtained by BMO for its loans, and Peguis claims Bridging did not take that step.

The chief and council therefore passed a band council resolution to write down the loan to $25-million, the financial statements say.

Chief and council planned to discuss the new financial statements at a community meeting in Peguis on March 20, but that discussion was put off after protesters disrupted the gathering, calling on council to delay the discussion until after the band council election.

In a statement released later that day, Chief Glenn Hudson, who is running for re-election, said the protesters’ actions “were a total breach of the democratic rights of all Peguis members” to have access tofactual, transparent and accountable information on the First Nation’s finances.

Mr. Hudson has not responded to requests for comment from The Globe and Mail. But he has publicly stated that the PwC legal actions were only made for procedural reasons and that he and council are working with PwC on a negotiated settlement.

Members of 269 Silent No More allege Mr. Hudson is using the financial statements to play down Peguis’s debt to improve his chances of re-election.

“It’s a complete and utter joke for the current chief and council to think that a band-council resolution, like a magic wand, will somehow make the debt magically disappear,” said Stan Bird, a member of 269 Silent No More who is running for chief against Mr. Hudson.

“It is yet another attempt to mislead the people.”

In an e-mail, PwC spokeswoman Chiara Battaglia said Bridging receivership proceedings are still under way and that PwC does not publicly comment on active proceedings.

The financial statements come with a “qualified” opinion from the Winnipeg office ofBaker Tilly Canada, an accounting firm,that cites several issues, including uncertainty related to the Bridging debt.

When an auditor has an “unqualified” opinion, it believes the financial statements fairly present the financial condition of the company or entity that put them out. An auditor “qualifies” its opinion when it finds issues that prevent it from saying that.

The financial statements also include a “going concern” note. Companies or other entities prepare financial statements under the assumption that they will continue to operate and be a “going concern.” If there is meaningful doubt about that, they or their auditors must insert a warning to the people reading the financial statements.

Baker Tilly said it was unable to comment on the Peguis statements.

Shanker Trivedi, an associate professor of accounting at Schulich School of Business, said he was struck by the large amount of money that falls under the umbrella of the qualified audit opinion, including more than $100-million in relation to the Bridging debt and $22-million related to what is identified as a “bad debt” in connection to loans to a company affiliated with Peguis.

Prof. Trivedi, who said he reviews many such statements for universities and other groups, also questioned how Peguis handled the Bridging debt. He noted that how the debt is presented in financial statements has a significant impact on the overall financial picture for the band.

“I mean, usually people write off what people owe them. … Nobody writes off loans that you owe to others, especially when nobody has told you that we are going to forgive the loan that you owe us,” Prof. Trivedi said.

A nationwide strike in France to protest a rise in the retirement age drew more than a million people onto the streets on Thursdaybefore ending in violent clashes with police in Paris and other cities.

The protest followed a strike of a similar magnitude in January and days of smaller walkouts and demonstrations in between. And more industrial action is planned for next week.

What’s making the French so angry is a new retirement age that will still be one of the lowest in the industrialized world.

Under a new law, pushed through parliament without a vote last week, the retirement age for most French workers will be raised from 62 to 64.

That will still keep France below the norm in Europe and in many other developed economies, where the age at which full pension benefits apply is 65 and is increasingly moving towards 67.

In the United States and the United Kingdom, the retirement age is between 66 and 67, depending on the year you were born. Current legislation envisages a further rise from 67 to 68 in Britain between 2044 and 2046 (although the timing of this increase is being reviewed and could change).

Russian President Vladimir Putin on Saturday said the country planned to station tactical nuclear weapons in Belarus in retaliation for the U.K.’s decision to provide Ukraine with armor-piercing rounds containing depleted uranium.

Russia falsely claimed these rounds have nuclear components.

Putin said the construction of the storage facilities for the weapons in the Russian-allied country, which borders Ukraine and three NATO countries – Latvia, Lithuania and Poland – would be completed by the beginning of July.