George Weston Ltd. WN-T +2.24%increase reported a profit in its fourth quarter compared with a loss a year ago.

The company, which is the controlling unitholder of Choice Properties Real Estate Investment Trust CHP-UN-T +0.22%increase and the controlling shareholder of Loblaw Companies Ltd. L-T -0.12%decrease, says it earned a profit attributable to common shareholders of $664 million or $5.05 per diluted share for the three months ended Dec. 31.

The company says the result compared with a loss of $38 million or 30 cents per diluted share in the last three months of 2023.

On an adjusted basis, George Weston says it earned $3.15 per diluted share in its latest quarter compared with an adjusted profit of $2.51 per diluted share a year ago.

Revenue for the quarter totalled $15.1 billion, up from $14.7 billion a year earlier.

Chairman and chief executive Galen Weston says the results were driven by the consistent and positive performance of its operating businesses.

“Loblaw’s focus on retail excellence provided unmatched quality and value to Canadians, and Choice Properties’ necessity-based portfolio generated stable and growing cash flows,” Weston said in statement.

“Our businesses are well-positioned to deliver on their strategy and financial objectives in 2025.”

National Bank of Canada NA-T -4.74%decrease reported higher first-quarter profit that beat analysts’ expectations as capital markets and wealth management activity surged amid market volatility, offsetting a jump in provisions for loan defaults.

Major Canadian bank earnings have received a boost this quarter from strong performance in trading activity as equity markets whipsawed in the aftermath of the U.S. presidential election in November. National Bank’s net income rose 8 per cent to $997-million, or $2.78 per share, in the three months that ended Jan. 31.

Adjusted to exclude certain items, including which costs related to the acquisition of Canadian Western Bank, the bank said it earned $2.93 per share. That edged out the $2.66 per share analysts estimated, according to Refinitiv.

“In a context of heightened macroeconomic and geopolitical uncertainty and an evolving credit cycle, we remain committed to maintaining our usual discipline regarding credit, capital and costs,” National Bank chief executive officer Laurent Ferreira said in a statement.

National Bank set aside higher provisions for credit losses – the funds banks reserve to cover loans that may default.

The bank reserved $254-million in provisions, higher than analysts anticipated and more than double the amount the bank allocated in the same quarter last year. This included $196-million against loans that the bank believes may not be repaid – a 33-per-cent increase from the previous year quarter.

The boost was driven by deteriorating loans in commercial and retail banking.

National Bank is the third major Canadian bank to report earnings for the fiscal first quarter. Scotiabank and BMO posted profit that beat analyst estimates. Royal Bank of Canada, Toronto-Dominion Bank and Canadian Imperial Bank of Commerce will close out the week for major bank earnings on Thursday.

Prior to the deal, 80 per cent of National Bank’s personal and commercial business was in Quebec, with 20 per cent outside of the province. By acquiring CWB, 40 per cent of its business comes from outside Quebec.

The bank kept its quarterly dividend unchanged at $1.14 per share.

Total revenue jumped 17 per cent in the quarter to $3.18-billion. Expenses rose 14 per cent to $1.65-billion, driven by a 22-per-cent jump in variable compensation, higher salaries and benefits and technology investments.

Profit from Canadian personal and commercial banking was $290-million, down 14 per cent as provisions surged.

The wealth management division generated $242-million of profit, up 23 per cent as fee-based revenue increased amid market volatility.

Profit from the capital markets division rose 35 per cent to $417-million on higher revenue in global markets.

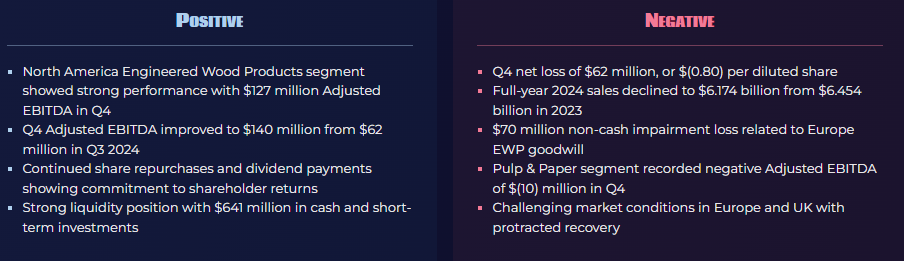

West Fraser Timber (WFG) reported Q4 2024 results with sales of $1.405 billion and a loss of $62 million, or $(0.80) per diluted share. The company’s Q4 Adjusted EBITDA was $140 million, representing 10% of sales. For the full year 2024, sales reached $6.174 billion with a loss of $5 million.

Key segment performance in Q4 included Lumber Adjusted EBITDA of $21 million, North America Engineered Wood Products at $127 million, and Europe EWP at $2 million, while Pulp & Paper recorded $(10) million. The company repurchased 311,523 shares for $27 million in Q4 and paid $26 million in dividends.

The company noted continued resilience in NA Engineered Wood Products business, supported by solid new home construction demand. However, high mortgage rates remain an affordability challenge, and potential U.S. tariffs on Canadian exports add uncertainty. For 2025, capital expenditures are expected to be $400-450 million.

West Fraser’s Q4 2024 results reflect the company’s resilience amid challenging market conditions, with the North America Engineered Wood Products segment delivering robust $127 million in Adjusted EBITDA, offsetting weakness in other segments. The 10% EBITDA margin on $1.405 billion in sales demonstrates maintained operational efficiency despite market headwinds.

The balance sheet remains exceptionally strong, with $641 million in cash even after retiring $300 million in senior notes. This financial flexibility positions the company well for both defensive and opportunistic moves in 2025. The continued share repurchases and steady dividend payments signal management’s confidence in sustainable cash flow generation.

Looking ahead to 2025, the operational guidance suggests cautious optimism. The targeted SPF shipments of 2.7-3.0 billion board feet and SYP shipments of 2.5-2.8 billion board feet indicate expectations of stable demand, though potential U.S. tariffs on Canadian exports remain a key risk factor. The $400-450 million projected capital expenditure demonstrates commitment to strategic mill modernization while maintaining financial discipline.

The $70 million non-cash impairment of Europe EWP goodwill reflects ongoing challenges in European markets, but the segment’s gradual recovery potential remains intact as interest rates begin to decline and OSB continues to gain market share from plywood. The company’s portfolio optimization strategy, shifting production from higher-cost to lower-cost mills, shows promise in improving overall cost position and operational efficiency.

(8:15 a.m. ET) Bank of Canada deputy governor Toni Gravelle speaks at the Bank of England Annual Research Conference in London.

(8:30 a.m. ET) U.S. Chicago Fed National Activity Index.

(10:30 a.m. ET) U.S. Dallas Fed Manufacturing Activity.

Earnings include: Domino’s Pizza Inc.; GFL Environmental Holdings Inc.; InterRent REIT; Spin Master Corp.; Topaz Energy Corp.; Zoom Video Communications Inc.

—

Tuesday February 25

Japan machine tool orders

Germany GDP

(8:30 a.m. ET) Canada’s manufacturing sales for January.

(9 a.m. ET) U.S. S&P CoreLogic Case-Shiller Home Price Index (20 city) for December. Estimate is a rise of 0.3 per cent from Novemer and up 4.4 per cent year-over-year.

(9 a.m. ET) U.S. FHFA House Price Index for December. Estimate is an increase of 0.2 per cent from November and a rise of 4.3 per cent year-over-year.

(10 a.m. ET) U.S. Conference Board Consumer Confidence Index for February.

Earnings include: Bank of Montreal; Bank of Nova Scotia; EQB Inc.; Home Depot Inc.; Intuit Inc.; Leon’s Furniture Ltd.; Maple Leaf Foods Inc.; Stantec Inc.; Tamarack Valley Energy Ltd.

—

Wednesday February 26

Germany consumer confidence

(8:30 a.m. ET) Canada’s wholesale trade for January.

(10 a.m. ET) U.S. new home sales for January. The Street is projecting an annualized rate decline of 2.9 per cent.

Also: Canada’s capital expenditures survey.

Earnings include: Capital Power Corp.; Exchange Income Corp.; George Weston Ltd.; Kinaxis Inc.; Lowe’s Companies Inc.; National Bank of Canada; Northland Power Corp.; Nvidia Corp.; Ovintiv Inc.; Salesforce Inc.; TJX Companies Inc.; WSP Global Inc.

—

Thursday February 27

Euro zone economic and consumer confidence

(8:30 a.m. ET) Canada’s current account balance for Q4.

(8:30 a.m. ET) U.S. initial jobless claims for week of Feb. 22. Estimate is 225,000, up 6,000 from the previous week.

(8:30 a.m. ET) U.S. real GDP and GDP deflator for Q4. Consensus projections are annualized rate increases of 2.3 per cent and 2.2 per cent, respectively.

(8:30 a.m. ET) U.S. durable and core orders for January. Consensus estimates are month-over-month rises of 2.2 per cent and 0.5 per cent, respectively.

(10 a.m. ET) U.S. pending home sales for January. Estimate is a decline of 2.0 per cent from December.

Also: Alberta’s budget and Ontario election.

Earnings include: Atco Ltd.; Athabasca Oil Corp.; Canadian Imperial Bank of Commerce; Canadian Utilities Ltd.; Chartwell Retirement Residences; Parkand Fuel Corp.; Pembina Pipeline Corp.; Royal Bank of Canada; Stella-Jones Inc.; Toronto-Dominion Bank

—

Friday February 28

China manufacturing and composite PMI

Japan CPI, retail sales and industrial production

ECB’s three-year CPI expectations

Germany retail sales and employment

(8:30 a.m. ET) Canada’s real GDP and chain prices for Q4. Consensus estimates are annualized rate increases of 1.8 per cent and 2.3 per cent, respectively.

(8:30 a.m. ET) Canada’s monthly GDP for December. The Street expects a rise of 0.3 per cent from November.

(8:30 a.m. ET) U.S. personal spending and income for January. Consensus projections are month-over-month rises of 0.3 per cent and 0.4 per cent, respectively.

(8:30 a.m. ET) U.S. core PCE price index for January. The Street is forecasting a rise of 0.3 per cent from December and 2.6 per cent year-over-year.

(8:30 a.m. ET) U.S. goods trade deficit for January.

(8:30 a.m. ET) U.S. wholesale and retail inventories for January.

Bank of Canada Governor Tiff Macklem warned that a full-blown trade war with the United States would permanently weaken the Canadian economy and cautioned that the central bank has few tools to respond to a structural shift toward protectionism that would both hamper growth and increase inflation.

He also said that now is not the right time for the central bank to change its 2-per-cent inflation target, even as it embarks on a five-year review of its monetary policy mandate.

“In the pandemic, we had a steep recession followed by a rapid recovery as the economy reopened. This time, if tariffs are long-lasting and broad-based, there won’t be a bounce-back,” Mr. Macklem said in a speech on Friday in Mississauga. “We may eventually regain our current rate of growth, but the level of output would be permanently lower. It’s more than a shock; it’s a structural change.”

Since returning to the White House, U.S. President Donald Trump has threatened to impose a 25-per-cent tariff on imports from Canada, with lower levies on energy products, although he delayed implementation until March 4. He has also announced 25-per-cent tariffs on steel and aluminum that take effect on March 12, and threatened additional tariffs on cars, lumber and other products.

A trade war would put the Bank of Canada in a difficult position. Widespread tariffs would likely push Canada’s fragile economy into a recession. But a trade conflict would also increase consumer prices in Canada, as Ottawa retaliated with its own tariffs, the loonie depreciated against the greenback and businesses rejigged supply chains.

That would force the central bank to choose between cutting interest rates to support growth and employment, and raising interest rates – or at least holding them steady – to keep inflation in check and prevent a one-time jump in prices from becoming entrenched in consumer and business psychology.

“Provided the inflationary impact of tariffs is not too big, monetary policy can help smooth the adjustment by supporting demand so it doesn’t weaken too much more than supply. But how much support monetary policy can provide is constrained by the need to control inflation,” Mr. Macklem said.

He suggested the aggressive monetary-policy-easing the bank delivered during the COVID-19 pandemic – cutting interest rates to near zero and buying hundreds of billions of dollars worth of government bonds to suppress interest rates – wouldn’t be appropriate this time around. “We can’t let a tariff problem become an inflation problem,” he said.

Inflation has fallen sharply over the past two years and is currently running below the bank’s 2-per-cent target, coming in at an annual rate of 1.9 per cent in January. That has allowed the central bank to cut interest rates at six consecutive meetings, bringing its benchmark policy rate to 3 per cent last month.

After the speech, financial markets put the odds of another rate cut at the bank’s next rate decision on March 12 at around 40 per cent, according to LSEG data. Looking further ahead, investors are pricing in two more cuts before the end of 2025.

“Macklem’s comments are consistent with our view that the Bank of Canada would cut rates roughly 50 to 100 basis points more than otherwise if 25-per-cent U.S. tariffs materialize,” Royce Mendes, head of macro strategy at Desjardins, wrote in a note to clients. (A basis point is 1/100th of a percentage point).

Mr. Mendes added that he expects the bank to hold rates steady next month, then continue cutting in April, “whether or not tariffs are introduced by then, given the domestic population and mortgage challenges facing the Canadian economy.”

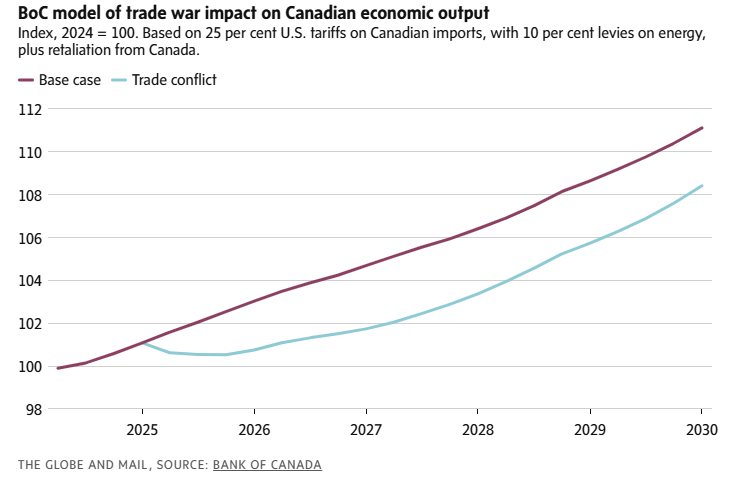

Mr. Macklem outlined new Bank of Canada modelling on the potential impact of Mr. Trump’s threat to impose a 25-per-cent tariff on Canadian imports, along with a lower 10-per-cent tariff on energy, together with retaliation from Canada.

In this scenario – which Mr. Macklem emphasized is not a forecast – Canada’s exports would fall by 8.5 per cent, consumer spending would contract by more than 2 per cent by 2027 and business investment in the country would decline by almost 12 per cent by early 2026.

“In our January projection with no tariffs, we forecast growth of about 1.8 per cent in both 2025 and 2026. But in the tariff scenario, the level of Canadian output falls almost 3 per cent over two years. That implies tariffs would all but wipe out growth in the economy for those two years,” Mr. Macklem said.

Worryingly, a major trade war would leave the Canadian economy on a permanently weaker footing. Even if the rate of growth rebounded, economic output would remain 2.5 per cent lower than a no-tariff scenario, Mr. Macklem said.

With the central bank constrained in how it could respond to a tariff-induced recession, Mr. Macklem suggested that governments at every level in Canada need to step up and do more to drive growth. That means removing rules that restrict interprovincial trade, speeding up timelines for regulatory approvals and improving east-west transportation links to help get Canadian products to overseas markets.

Mr. Macklem also used the speech to outline priorities for the coming Bank of Canada mandate review with the federal government, which takes place every five years and will be finalized next year. In the past, the bank has looked at whether its 2-per-cent inflation target should be changed. Mr. Macklem said he did not favour reopening this debate this time around. “In my view, now is not the time to question the anchor that has proven so effective in achieving price stability,” he said.

But he said the bank will be looking at a range of issues, including how monetary policy interacts with Canada’s unaffordable housing market, whether the bank needs a “richer playbook” to deal with supply-side shocks and whether it should use a broader range of inflation indicators.

Canadian Tire Corp. Ltd.CTC-A-T -1.86%decreaseCTC-T -0.04%decrease has agreed to sell its global outdoor and activewear brand Helly Hansen in a nearly $1.3-billion deal, as the company seeks to reinvest in the Canadian retail business at a time of “market uncertainty.”

The Toronto-based retailer announced on Wednesday that it reached a deal to sell Helly Hansen to Kontoor Brands Inc., the U.S.-based owner of the Lee and Wrangler denim brands. The deal comes six years after Canadian Tire acquired the Norway-based clothing line from Ontario Teachers’ Pension Plan for $985-million.

The company plans to use the proceeds of the sale to pay down debt, to buy back shares and to invest in its retail stores. The funds also give Canadian Tire “additional flexibility for general corporate purposes, including to address market uncertainty,” according to a press release issued on Wednesday.

Canadian Tire’s chief executive officer was vocal about that uncertainty last week, saying that U.S. President Donald Trump’s threats to impose widespread tariffs on Canadian imports have “substantially erased” any nascent signs of improving consumer sentiment in this country.

In 2022, the company announced the launch of a $3.4-billion, four-year plan it called “Better Connected,” designed to increase sales across its banners. But economic headwinds caused Canadian Tire to slow that spending plan. Canadian Tire has said it will provide an update on its corporate strategy on March 6.

Under Canadian Tire’s leadership, Helly Hansen has significantly increased sales and profits, the company reported. At the time of the acquisition in 2018, the brand generated $500-million in annual revenue and $50-million in earnings before interest, tax, depreciation and amortization (EBITDA), according to the company. Last year, Helly Hansen reported $894-million in worldwide revenue and $102-million in EBITDA.

“As our strategy becomes more singularly focused on great Canadian retail, it is time to pass this iconic brand into global hands,” Canadian Tire president and CEO Greg Hicks said in a statement.

The retailer will continue to stock Helly Hansen products, which are already sold in Canadian Tire, Marks and Sport Chek stores, under a new multiyear supply agreement with Kontoor.

Helly Hansen was founded by a Norwegian sea captain and his wife in 1877. Helly Juell Hansen and Maren Margarethe created water-resistant clothing for sailors by soaking linen in linseed oil. Over the years, the company expanded into raincoats, fleeces and base layers, parkas and footwear. The bulk of the business is in outerwear and activewear, including apparel for winter sports and hiking; while roughly 25 per cent of the business is in work wear such as coveralls and high-visibility jackets.

While Helly Hansen has grown under Canadian Tire’s ownership, its profit margins have lagged some of its global peers. Kontoor executives said on Wednesday that they see an opportunity to double Helly Hansen’s operating margin, including by taking advantage of the company’s existing global sourcing, logistics and distribution capabilities.

“It is an incredibly talented organization at all levels, but it has also been operating as a standalone business without global scale,” Kontoor president, CEO and chairman Scott Baxter told analysts on a conference call Wednesday morning to discuss the deal.

“While Helly has been executing at a high level on its own, we are highly confident it will see significant benefits under our ownership as a more synergistic global brand operator.”

Canadian Tire Corporation, Limited (TSX: CTC) (TSX: CTC.A) (CTC or the Company) today announced results for its fourth quarter and full year ended December 28, 2024.

Strong December sales drove a return to comparable sales growth in Q4.

Triangle spend per member was up in Q4, as members earned and redeemed at higher levels than last year.

Q4 Diluted Earnings Per Share (EPS) was $7.37; Q4 Normalized Diluted EPS was up 20.4% to $4.07.

Full-year Diluted EPS was $15.92; Full-Year Normalized Diluted EPS1 was up 21.7% to $12.62.

Cameco Corp. (CCJ) on Thursday reported fourth-quarter net income of $96.5 million.

The Saskatoon, Saskatchewan-based company said it had profit of 22 cents per share. Earnings, adjusted for non-recurring costs, came to 26 cents per share.

The results surpassed Wall Street expectations. The average estimate of three analysts surveyed by Zacks Investment Research was for earnings of 23 cents per share.

The uranium producer posted revenue of $845.5 million in the period.

For the year, the company reported profit of $125.5 million, or 28 cents per share. Revenue was reported as $2.29 billion.

Cameco shares have fallen slightly more than 9% since the beginning of the year. The stock has climbed 12% in the last 12 months.

_____

This story was generated by Automated Insights (http://automatedinsights.com/ap) using data from Zacks Investment Research. Access a Zacks stock report on CCJ at https://www.zacks.com/ap/CCJ

Teck Resources Ltd. reported a $748-million loss from continuing operations attributable to shareholders in its latest quarter as it took a one-time asset impairment charge related to its Trail operations.

The Vancouver-based mining company says its loss amounted to $1.45 per diluted share for its third quarter compared with a loss of $48 million or nine cents per share a year earlier.

Revenue for the quarter totalled $2.86 billion, up from $1.99 billion in the same quarter last year.

In its outlook, Teck says it now expects its 2024 copper production to amount to 420,000 to 455,000 tonnes, down from earlier guidance for 435,000 to 500,000 tonnes. The company also lowered its 2024 guidance for molybdenum and refined zinc production and reduced its expectations for zinc net cash unit costs.

On an adjusted basis, Teck says it earned 60 cents per diluted share for its latest quarter, up from an adjusted profit of 16 cents per diluted share a year earlier.

The average analyst estimate had been for a profit of 37 cents per share, according to LSEG Data & Analytics.

This report by The Canadian Press was first published Oct. 24, 2024.