Gold prices moved higher on Friday thanks to a weak dollar and rising hopes of an interest rate cut by the Federal Reserve next month. Escalating tensions in the Middle East contributed as well to the yellow metal’s gains.

The dollar index dropped to 102.55, down nearly 0.5% from the previous close.

Gold futures for August ended up by $45.50 or about 1.85% at $2,498.60 an ounce. Gold futures gained 2.73% in the week, recording their 3rd successive weekly gain.

Silver futures for August ended up $0.436 or about 1.54% at $28.778 an ounce. Silver futures gained about 4.7% in the week.

Copper futures for August dropped to $4.1140 per pound, down $0.0250 from the previous close.

Markets are now pricing in just a 25% chance of a 50-basis-point cut by the Federal Reserve next month, down from 55% a week ago, according to the CME FedWatch tool.

In economic news today, preliminary data released by the University of Michigan showed consumer sentiment in the U.S. has improved by more than expected in the month of August.

The University of Michigan said its consumer sentiment index rose to 67.8 in August after falling to 66.4 in July. Economists had expected the index to inch up to 66.9.

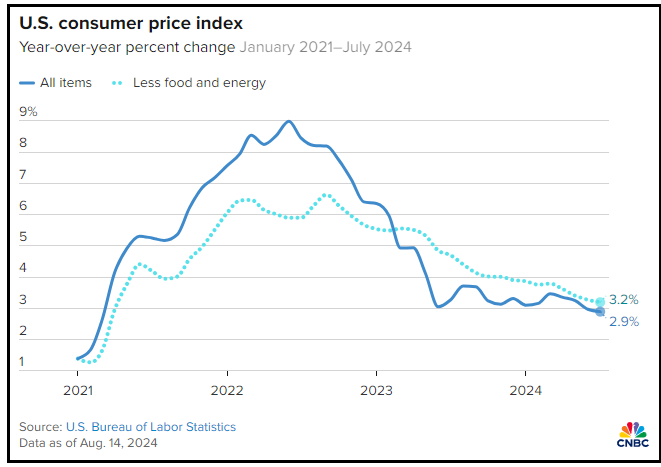

On the inflation front, the report said year-ahead and long-term inflation expectations were both unchanged from the previous month at 2.9% and 3%, respectively.

Meanwhile, a report from the Commerce Department said housing starts plunged by 6.8% to an annual rate of 1.238 million in July after jumping by 1.1% to a revised rate of 1.329 million in June.

Economists had expected housing starts to slump by 1.7% to an annual rate of 1.330 million from the 1.353 million originally reported for the previous month.