The American job market continues to show surprising strength, shrugging off the high costs of the Iran war.

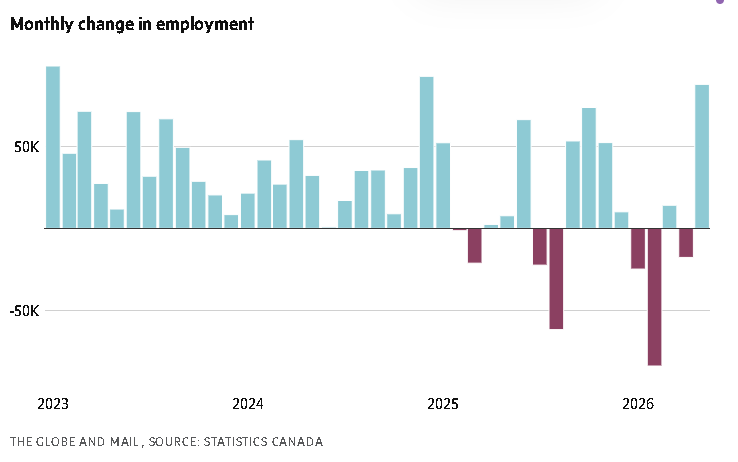

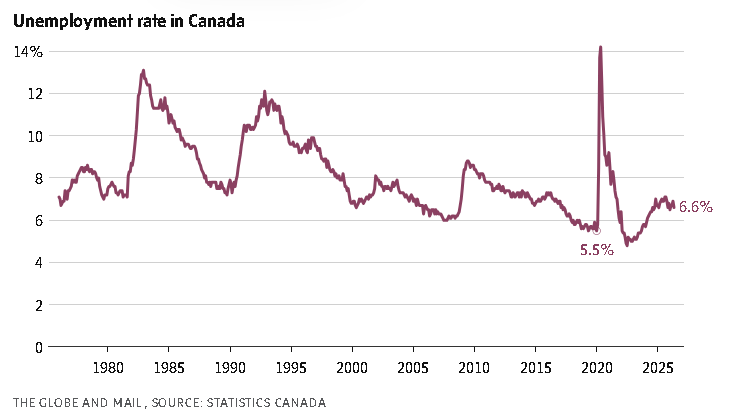

Employers added 172,000 jobs in May – roughly double what forecasters had expected – and the unemployment rate remained at a low 4.3 per cent.

The Labor Department reported Friday that job growth was down slightly last month from a revised 179,000 in April. The unemployment rate stayed at a low 4.3 per cent.

Hiring has bounced back this year from a miserable 2025, showing resilience in the face of economic uncertainty and painfully high energy prices caused by the Iran war.

The job gains last month were broad-based. Local governments added 55,000 workers, restaurants and bars 48,000, health care companies 35,000.

In another sign of job market strength, Labor Department revisions added a combined 93,000 jobs in March and April. Job growth averaged 188,000 a month from March through May, marking the best three months of hiring since early 2024.

“The hiring recession is over. American firms are hiring again,” said Heather Long, chief economist at Navy Federal Credit Union. “The job rebound is happening in almost every industry … This is encouraging news for job seekers and for the U.S. economy. The labour market has stabilized and is showing early signs of a genuine rebound.’’

Despite the pickup in hiring, wage gains were modest, which could reassure the inflation fighters at the Federal Reserve. Average hourly wages rose 0.3 per cent from April and 3.4 per cent from May, 2025, consistent with the Fed’s 2-per-cent inflation target.

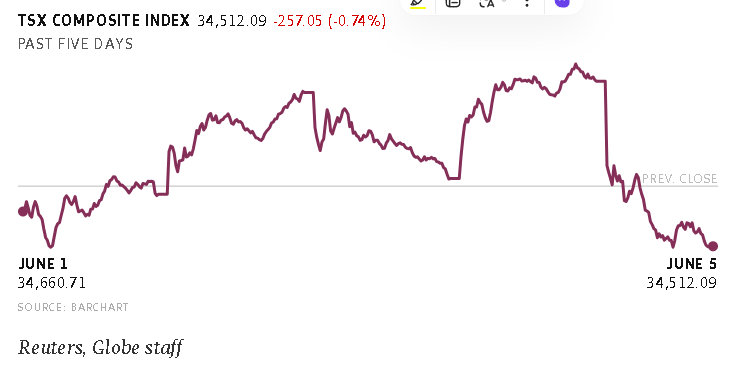

Financial markets retreated after the report came in, likely reflecting expectations that the Fed won’t see a need to cut interest rates this year because hiring is so healthy.

Workers, jobseekers and employers have been stuck in an awkward “no-hire, no-fire’’ labour market. “Those who have jobs are clinging to them, while those without are left wanting,” Diane Swonk, chief economist at the tax and consulting firm KPMG, wrote in a commentary ahead of the jobs report. “The result is a sense of being frozen or left in a sort of labour market purgatory.’’

Many young people are finding it tough to break into a stagnant job market. And workers who have been laid off struggle to get back to work. Nearly 28% of the unemployed in April had been jobless for more than six months, biggest share since December, 2021.

Seeing their prospects diminished, Americans are reluctant to leave their jobs and seek something better elsewhere. In April, the number of people who quit dropped to the lowest level since the frightening days of August, 2020, when the COVID-19 was running rampant.

Last year, employers added 9,700 jobs a month, fewest outside a recession since 2002.

This year, hiring has rebounded, averaging 114,000 new jobs a month from January through May. Big tax refunds – the product of President Donald Trump’s 2025 tax cuts – have given the economy a lift, offsetting the impact of higher energy prices since the United States and Israel attacked Iran in late February. But the refunds have mostly been pocketed, and gasoline prices remain above US$4 per gallon.

Healthcare companies have been driving much of hiring over the past year.

Martha Gimbel and Ryan Nunn of Yale University’s Budget Lab note that strong healthcare hiring isn’t surprising as Americans age and need more prescriptions and trips to the doctor. In fact, the industry’s job growth is in line with Labor Department predictions from a decade ago. “The question is not why healthcare has kept hiring–it is why other industries have not,’’ they wrote in a report published Tuesday, suggesting that one explanation might be an immigration crackdown that has reduced the supply of foreign-born workers.

At least the United States doesn’t need as many new jobs as it used to. The drop in immigrants and rising Baby Boomer retirements mean that fewer people are competing for work. As a result, the so-called break-even point – the number of new jobs required to keep the unemployment rate stable – has likely dropped to near zero, from the 155,000 new jobs per month that was typical two or three years ago, according to a Federal Reserve report.

Some analysts fear that artificial intelligence will wipe out entry-level jobs. But economists Gregory Daco and Lydia Boussour of the tax and consulting firm EY-Parthenon wrote in a commentary Tuesday that AI “adoption is proving more gradual and costly than many anticipated. Firms are increasingly using AI to enhance productivity and control labour costs.’’ But AI, they wrote, has reduced hiring rather than “triggering broad-based layoffs.″

And a new study by the Federal Reserve Bank of New York identified a different culprit for young people’s struggle to land jobs after college: the rise of remote work. Businesses, it seems, are reluctant to hire new grads for work-at-home jobs because it is harder to train and mentor them when they aren’t coming into the office.