Canada’s gross domestic product grew by 0.4 per cent on a monthly basis in January as economic activity continued the momentum of the last few of months, data showed on Friday.

Economists said part of the growth was helped by an increase in demand for cross-border trade by companies seeking to avoid the impact of U.S. tariffs.

Canada’s economic activity has grown at a brisk pace in the last two quarters, registering an annualized growth of well over 2 per cent, indicating that seven rounds of interest rate cuts has helped boost consumer spending and investment.

But the Bank of Canada has warned that there was a significant gap between the robust hard data seen so far and a survey data of businesses and consumers.

With U.S. tariffs coming on a wide range of products and retaliatory tariffs, spending and investments in Canada could dip considerably, hurting economic growth, the BoC and economists have said.

Analysts polled by Reuters had estimated January growth to be 0.3 per cent from an upwardly revised 0.3 per cent growth in December from an initial 0.2 per cent growth. A flash estimate from Statscan showed that growth in February was likely to be unchanged.

The flat February growth was probably due to the offsetting impacts of growth in manufacturing, finance and insurance and contraction in real estate rental, leasing, oil and gas extraction and retail trade, Statscan said.

The Canadian dollar pared some losses after the data and was trading down 0.1 per cent to 1.4318 against the U.S. dollar, or 69.84 U.S. cents. Yields on the two-year government bond fell 3.6 basis points to 2.521 per cent.

January’s economic activity was boosted by both goods and services sectors, with expansion seen in 13 out of 20 areas, the statistics agency said. Goods-producing industries grew by 1.1 per cent, its largest growth since October 2021.

The mining, quarrying, and oil and gas extraction and manufacturing sectors were the largest contributors to growth. The oil and gas extraction subsector registered the biggest growth amongst them with 2.6 per cent expansion in January.

The manufacturing sector was up 0.8 per cent in January after contracting for two consecutive months. Construction activity continued to expand in January, led by residential construction, which hit its highest level since November 2023.

Retail trade was the only major dampener for January, data showed.

U.S. President Donald Trump imposed 25 per cent tariffs on steel and aluminum earlier this month and on Wednesday slapped 25 per cent tariffs on auto parts and car imports. He has vowed more import duties from next month.

This is likely to wipe off almost all growth projected by the central bank, the BoC has said. It had forecast 2025 growth at 1.8 per cent.

Currency swap markets are seeing a 62 per cent chance of a pause in rate cuts on April 16 after the BoC slashed rates by 225 basis points to 2.75 per cent in the space of nine months.

“Given recent developments on the tariff front this is clearly now old news, and the Bank of Canada will be carefully judging downside risks to growth against a stronger near-term profile for inflation as it makes its next policy decisions,” said Andrew Grantham, senior economist at CIBC Capital Markets.

Statscan said that exports to the United States accounted for 16.8 per cent of Canada’s GDP and over 2.6 million local jobs.

Gold prices rose on Thursday as U.S. auto tariffs ratcheted up global trade tensions ahead of an April 2 deadline for reciprocal tariffs from the world’s largest economy.

U.S. President Donald Trump on Wednesday unveiled a 25% tariff on imported cars and light trucks starting next week, widening the global trade war.

Investors feared that Trump’s reciprocal tariffs, expected to take effect on April 2, might fuel inflation, slow economic growth and heighten trade tensions.

Concerns over Trump’s tariff policies catapulted gold to a record high of $3,057.21 on March 20.

Aakash Doshi, global head of gold at SPDR ETF Strategy, expects gold will breach $3,100 in the second quarter and “the market could potentially push another 8%-10% higher by end-2025 if the current macro and physical market tailwinds sustain for the yellow metal.”

Goldman Sachs on Wednesday raised its end-2025 gold price forecast to $3,300 per ounce from $3,100, citing stronger-than-expected ETF inflows and sustained central bank demand.

Investors await the U.S. personal consumption expenditures data, due on Friday, which could shed more light on the U.S. interest rate path.

Last week, the U.S. central bank held benchmark interest rate steady, but indicated it could cut rates later this year. Non-yielding bullion tends to thrive in a low interest-rate environment.

Minneapolis Federal Reserve Bank President Neel Kashkari said that while the U.S. central bank has made a lot of progress bringing inflation down, “we have more work to do” to get inflation to the Fed’s 2% target.

U.S. President Donald Trump has threatened to impose “far larger” tariffs on the European Union and Canada if they work together to combat trade tariffs.

“If the European Union works with Canada in order to do economic harm to the USA, large scale Tariffs, far larger than currently planned, will be placed on them both in order to protect the best friend that each of those two countries has ever had!,” Trump posted on social media platform Truth Social on Thursday.

U.S. President Donald Trump says he will enact his long-awaited tariffs on imported vehicles on April 2, defying industry experts who warn that the move will drive up costs for businesses and consumers while undercutting the United States-Mexico-Canada free-trade agreement that he signed in his first term.

Mr. Trump said on Wednesday that automobiles and auto parts imported to the U.S. will face 25-per-cent tariffs. Vehicles imported under the USMCA will be taxed at the same amount based on their non-U.S. content. Auto parts covered by the trade agreement will face tariffs at a later date, also based on their non-U.S. content.

The President has also promised to introduce “reciprocal tariffs” on April 2, which would be an effort to match tariffs and non-tariff barriers that other countries place on U.S. goods.

The automotive tariffs are central to Mr. Trump’s economic nationalist trade policy, which aims to spur domestic manufacturing and persuade foreign companies, especially automakers, to shift production to the U.S. Mr. Trump has said that he wants to “permanently shut down” the Canadian auto industry and annex the country with “economic force.”

The move upends decades of free trade in automobiles between Canada and the U.S., and threatens one of Canada’s key manufacturing sectors. The impact will also be felt by global auto manufacturers that export to the United States.

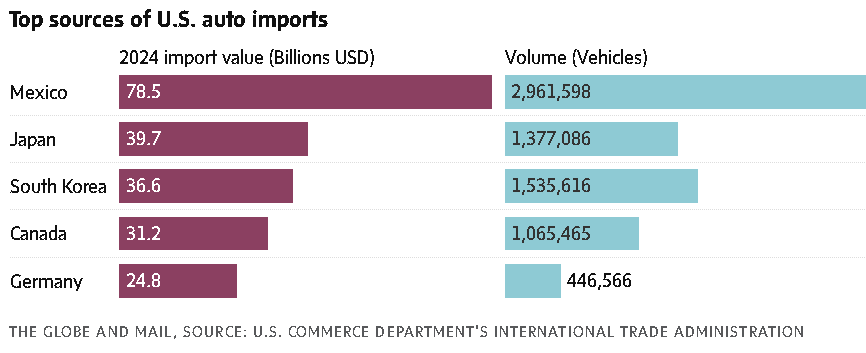

Automakers and parts suppliers employ 125,000 people in this country, mostly in Ontario, and hundreds of thousands more in other businesses. Ontario plants run by Ford, General Motors, Stellantis, Honda and Toyota made a total of 1.6 million passenger vehicles in 2024, according to the Canadian Vehicle Manufacturers’ Association, most of which were exported to the United States.

During a press conference on Wednesday, Mr. Trump said he had spoken with the Detroit-based automakers and said their reaction to the tariffs depended on where they produced their vehicles. “If you have factories here, you’re thrilled,” Mr. Trump said. “If you don’t, you’re going to have to get going and build them, otherwise they have to pay tariffs. It’s very simple.”

The U.S. is relying on Section 232 of the Trade Expansion Act of 1962 to apply the tariffs on imported cars and car parts, deeming the imports a “threat to national security.”

U.S car sales in 2024 totalled 16 million, half of which were imported, according to a White House statement. Of the 8 million made in the U.S., the average domestic content is as low as 40 per cent, the statement reads. “Therefore, of the 16 million cars bought by Americans, only 25 per cent of the vehicle content can be categorized as Made in America,” the statement said.

Ontario Premier Doug Ford condemned the tariff announcement, which hits his province hard, calling it an “early attack” before the April 2 deadline. He said it would cause the price of cars in the U.S. to rise, while forcing U.S. factories to close as the move disrupts the auto industry’s cross-border supply chains.

President Trump is at it again.

His 25 per cent tariffs on cars and light trucks will do nothing more than increase costs for hard-working American families. U.S. markets are already on the decline as the president causes more chaos and uncertainty. He’s putting American jobs at…— Doug Ford (@fordnation) March 26, 2025

David Adams, president of Global Automakers of Canada, which represents Toyota, Honda and several other manufacturers, said the announcement undercuts Mr. Trump’s campaign promises to tackle affordability and inflation.

“It’s hard to see a good outcome for Canadians or Americans from this announcement,” Mr. Adams said in an interview, predicting that the tariff will reduce Ontario auto production.

“The reality is at some point you’re going to be selling fewer vehicles into the U.S. market, which means that there may have to be production adjustments at some point down the line,” Mr. Adams said. “The longer these tariffs stay in place, the more challenging it becomes for vehicle producers here in Canada.”

Fraser Johnson, a professor at Western University’s Ivey Business School, said the tariffs will have “significant repercussions” for the Canadian automotive industry and the investments the companies make. However, he said car makers will not move their Ontario plants south, given the billions of dollars and years of planning involved.

He said the levies will drive up costs for businesses, car buyers and workers in Canada and the U.S. “This is not good news for anybody,” Prof. Johnson said by phone. “It’s not good news for Canadian companies and workers. It’s also not good news for the U.S. auto sector.”

The tariffs will cause Canadian job losses in the long term, Prof. Johnson said, but the unsustainable damage they cause in the U.S. will eventually spur their removal. However, Mr. Trump gave no indication that he would back down.

The Trump administration had already imposed a 25-per-cent tariff on Canadian and Mexican goods on March 4, with a lower 10-per-cent levy for energy products, critical minerals and potash. Two days later, he offered a month-long reprieve on tariffs for products that comply with the USMCA. At the time, the President said he offered the break to give automakers time to rejig their supply chains.

U.S. President Donald Trump speaks to the media in the Oval Office at the White House, on March 26.Evelyn Hockstein/Reuters

On March 12, Mr. Trump imposed 25-per-cent tariffs on steel and aluminum imports, including from Canada.

When asked about the “reciprocal tariffs” that are set to go into effect next week, Mr. Trump said they would be imposed on all countries, but that they would be “very lenient.”

“I think people are going to be surprised. In many cases, it’ll be less than the tariffs they’ve been charging us for decades,” said Mr. Trump.

In retaliation for U.S. levies, Canada has implemented tariffs on some $60-billion worth of U.S. goods.

On the federal election campaign trail, party leaders announced their own plans on Wednesday to protect Canada’s auto manufacturing industry.

Earlier in the day, before the tariffs were announced, Liberal Leader Mark Carney promised that a Liberal government would protect Canada’s auto sector in the face of U.S. tariff threats. He pledged a $2-billion fund to boost competitiveness in the sector, “protect manufacturing jobs, support workers to upskill their expertise in the industry, and build a fortified Canadian supply chain – from raw materials to finished vehicles.”

After the U.S. President’s press conference, Mr. Carney called the latest tariffs a “direct attack” on Canada and Canadian auto workers. He said ties between the two countries are “in the process of being broken” by Mr. Trump. He called a meeting Thursday of the cabinet committee on Canada-U.S. relations.

Conservative Leader Pierre Poilievre said Mr. Trump had a history of changing his mind on tariffs. “The message to President Trump should be to knock it off,” he said.

“He should lift these tariffs. But whether or not he does – because he’s changed his mind before, he’s done this twice, puts them on, takes them off, and we can suspect that that may well happen again – we have to become more self reliant and have new and different markets so that we no longer rely on or depend on what is becoming an increasingly undependable customer.”

Mr. Trump has set various tariff deadlines for Canada and Mexico over the past few months, only to change his mind and pause the levies. This has confounded businesses, which rely on certainty when planning their operations.

The Detroit-based automakers have been lobbying against the tariffs, which they said would cause disruption and add billions in expenses. The companies operate plants in Canada and Mexico, and move components across borders several times before a vehicle’s final assembly.

James Farley, Ford Motor’s chief executive officer, warned in February that the tariffs will “blow a hole” in the U.S. industry, leading to “cost and chaos.”

Business and labour leaders expressed outrage at the tariffs.

“These new tariffs on Canada, one of our closest allies and largest trading partners, are unjust and will have lasting negative impacts on American and Canadian workers,” said Brian Bryant, international president of the 600,000-member International Association of Machinists and Aerospace Workers.

Candace Laing, head of the Canadian Chamber of Commerce, said the tariffs will costs tens of thousands of jobs on both sides of the Canada-U.S. border, driving jobs to other countries.

“This tax hike puts plants and workers at risk for generations, if not forever,” Ms. Laing said. “With this latest tariff, the U.S. administration has committed to taxing America’s automotive manufacturers and increasing the production cost of a car.”

The Canadian dollar CADUSD -0.20%decrease pulled back from an earlier one-month high against its U.S. counterpart on Wednesday as investors braced for expected U.S. auto tariffs and weighed minutes from the Bank of Canada’s latest meeting.

The loonie was trading nearly unchanged at 1.4283 per U.S. dollar, or 70.01 U.S. cents, after earlier touching its strongest level since Feb. 24 at 1.4236.

U.S. President Donald Trump will announce plans for long-promised tariffs on automotive imports at a news conference on Wednesday, widening the global trade war.

Canada sends about 75 per cent of its exports to the United States including oil and autos.

Canadian Prime Minister Mark Carney said if the ruling Liberals won an April 28 election, his government would create a C$2 billion ($1.40 billion) fund to boost the auto sector’s competitiveness.

The Bank of Canada saw less evidence of downward pressure on inflation even as it decided to cut rates by 25 basis points on March 12, a summary of monetary policy deliberations showed.

“Policymakers are extremely sensitive to upside inflation risks after the past few years, especially with fiscal stimulus likely playing a role in the response to the trade war,” Benjamin Reitzes, Canadian rates & macro strategist at BMO Capital Markets, said in a note.

“That won’t keep the BoC from cutting rates if tariffs worsen, but it suggests any further easing won’t be aggressive and limits how low the Governing Council is willing to go.”

The U.S. dollar added to recent gains against a basket of major currencies, while the price of oil settled 0.9 per cent higher at $69.95 a barrel.

Canadian bond yields moved higher across the curve, tracking moves in U.S. Treasuries. The 10-year was up 4 basis points at 3.12 per cent, after earlier touching its highest level since Feb. 24 at 3.142 per cent.

Canadian powersports vehicle maker BRP Inc. DOO-T +7.31%increase has swung to a loss for its latest quarter and suspended financial forecasts for the coming year, the latest company to pull its projections in the face of a rapidly shifting global trade environment.

The Valcourt-Que.-based manufacturer, known for its Ski-Doo snowmobiles and Can-Am offroad vehicles, saw a major sales boost during the COVID-19 pandemic but has since been reeling from softer demand. Dealers have been hesitant to carry a lot of inventory and promotions have increased to stimulate sales.

The company on Wednesday reported a net loss of $44.5-million or $0.60 per share for the three months ended Jan. 31, reversing a profit of $302.8-million or $3.95 per share the year before. Revenue fell nearly 20 per cent in the fourth quarter to $2.1-billion.

The results beat analyst expectations. On the basis of adjusted earnings per share, BRP reported $0.98 cents versus analyst predictions of $0.88 while revenue also came in slightly higher than forecasts.

“Looking ahead to fiscal 2026, the ongoing global tariff disputes have created economic uncertainty, making financial projections more challenging at this time,” BRP chief executive José Boisjoli said in a statement. “This uncertainty has also had a negative impact on consumer demand.”

The company’s decision last fall to put its boat business up for sale and focus resources on its snowmobile and off-road vehicles should allow it to solidify its industry leadership, the CEO said. Its deliberate effort to reduce shipments in recent quarters has protected the brand and should also better align deliveries with retail sales, he said.

But a big storm cloud is casting a shadow over the business. BRP is particularly exposed to tariffs that the Trump administration has either imposed or threatened.

Essentially all of the company’s manufacturing is outside the United States, with about 75 per cent of units produced in Mexico and the rest in Canada and Europe. It began shifting operations to the Spanish-speaking country nearly 20 years ago to capitalize on a large pool of young, reliable and low-cost workers and has since expanded capacity there several times.

The Trump tariffs have exposed the hazards of concentrating production in one country and laid bare the fragility of a North American trade pact now at the mercy of a president’s political impulses. National Bank of Canada analyst Cameron Doerksen has said BRP is the corporation “most at risk” from tariffs among the transportation and industrial companies he researches.

New tariffs stand to increase the price U.S. consumers pay for BRP vehicles at dealerships, hurting demand and potentially putting the company at a disadvantage against competitors that have manufacturing footprints in the United States.

Tariffs could also provoke a recession in Canada and other markets if the economy slows. That in turn would reduce sales of BRP vehicles, which are typically seen as a discretionary purchase that people cut during tough times.

Citi analyst James Hardiman sees BRP in an untenable situation, with its cost of goods sold coming into the United States via Mexico equating to more than US$1-billion in tariff impacts. Its tariff exposure is far greater than its earnings power, he said in a research note this month.

U.S. rival Polaris would also get hit but to a lesser extent, the analyst said as he recommended investors sell shares of both companies.

“Were 25-per-cent tariffs on Mexican and Canadian imports to be levied indefinitely (an unlikely but distinct possibility), we believe that both companies would immediately incur significant losses, impacting their long-term prospects,” Mr. Hardiman said. “Even in the absence of this scenario, however, the weakening of fundamentals in conjunction with the incremental Chinese tariffs is enough to weigh on valuations going forward.”

After a bright start, the Canadian market retreated a bit, but remains in positive territory about an hour past noon on Tuesday, thanks to gains in materials, healthcare, consumer staples and energy sectors.

The mood is positive amid optimism about some tariff exemptions by the Trump administration. The U.S. President said on Monday that not all proposed levies would be enforced by April 2, with some countries potentially receiving exemptions.

The benchmark S&P/TSX Composite Index, which climbed to 25,454.86 at the start, was up 89.80 points or 0.35% at 25,393.91 a little while ago. +89.80(+0.35%)

Sandstorm Gold is rising nearly 7.5%. Eldorado Gold is up 6.5%, while Ngex Minerals, Torex Gold Resources, Birchcliff Energy, New Gold, Oceanagold, Wesdome Gold Mines and Equinox Gold are up 4 to 5%.

Lundin Mining, SSR Mining, Osisko Gold, Baytex Energy, B2Gold Corp, Alamos Gold, Agnico Eagle Mines, Brookfield Business Partners, Dundee Precious Metals and Peyto Exploration are gaining 2 to 3.1%.

Descartes Systems Group is up by about 2.5% after the company said that it has acquired 3GTMS, a provider of transportation management solutions, for approximately $115 million.

Belgium Business Confidence Unexpectedly Erodes FurtherMarch 25, 2025 11:46 ETBusiness confidence in Belgium continued to fall in March, driven by the weakness in all sectors except trade, survey data from the National Bank of Belgium showed on Tuesday.

UK Retail Sales Decline Sharply In March: CBIMarch 25, 2025 07:44 ETUK retail sales declined sharply in March amid weaker confidence, the Distributive Trades survey results from the Confederation of British Industry showed on Tuesday. The retail sales balance fell to -41 percent in March from -23 percent in February. The balance was worse than forecast of -28 percent….

Polish Jobless Rate Remains Stable At 3.4%March 25, 2025 06:58 ETThe unemployment rate in Poland remained stable in February after rising in the previous three months. The unemployment rate came in at 5.4 percent in February, the same as in the previous month. In the corresponding month last year, the unemployment rate was also 5.4 percent. The number of registered unemployed people rose to 846,600 in February from 837,600 in January.

German Ifo Business Confidence At 8-Month HighMarch 25, 2025 06:31 ETGerman business confidence improved to an eight-month high in March as defense and infrastructure spending plans offset concerns about US trade policies, survey data from ifo Institute showed on Tuesday. The business climate index hit 86.7 in March, up from 85.3 in the previous month. The score was seen at 86.8. The reading was the strongest since last July.

Spain Producer Price Inflation At 2-Year HighMarch 25, 2025 05:19 ETSpain producer prices increased at the fastest pace in two years in February on higher energy prices, the statistical office INE reported Tuesday. Producer price inflation advanced to 6.6 percent in February from 2.6 percent in January. This was the fastest growth since February 2023, when prices…

Sweden’s Producer Price Inflation Slows Slightly To 3.4%March 25, 2025 04:44 ETProducer prices in Sweden decreased somewhat in February from a nearly 2-year high in the prior month. Producer prices in Sweden decreased somewhat in February from a nearly 2-year high in the prior month. Prices for energy-related products alone grew 8.4 percent from last year, and those for capital and consumer goods rose by 1.6 percent and 3.2 percent, respectively.

Finland Jobless Rate Falls To 9.4%March 25, 2025 02:46 ETFinland’s unemployment rate decreased marginally in February after rising to an 8-month high in the previous month. The jobless rate among the 15-74 age groups dropped to 9.4 percent in February from 9.5 percent in January. In the same month last year, the unemployment rate was 7.8 percent.

Europe New Car Registrations Fall For Second MonthMarch 25, 2025 02:39 ETEurope’s new car registrations declined for the second straight month in February due to sharp reductions in Germany and Italy, the European Automobile Manufacturers’ Association, or ACEA, said on Tuesday. New car sales were down 3.4 percent on a yearly basis in February, after a 2.6 percent drop in January. The German market reported the biggest monthly fall of 6.4 percent.

European Economic News Preview: German Ifo Business Confidence DueMarch 25, 2025 01:53 ETBusiness confidence survey data from Germany is the top economic news due on Tuesday, headlining a light day for the European economic news. At 4.00 am ET, Spain’s INE publishes producer prices for February. Prices had increased 2.6 percent annually in January.

Hong Kong Trade Gap Narrows In FebruaryMarch 25, 2025 06:43 ETHong Kong’s trade deficit decreased in February from a year ago as exports grew faster than imports. The trade shortfall dropped to HK$36.3 billion in February from HK$41.6 billion in the same month last year. In January, the trade balance showed a surplus of HK$2.1 billion. The annual rise in exports was 15.4 percent in February versus only a 0.1 percent rise in January.

Taiwan Industrial Output Growth Quickens, Retail Sales FallMarch 25, 2025 05:14 ETTaiwan’s industrial production growth rebounded sharply in February, while retail sales fell for the first time in four months. Industrial production advanced 17.91 percent yearly in February, much faster than the 4.87 percent growth in January. Retail sales fell 3.84 percent in February, in contrast to a 5.51 percent in January.

Malaysian Leading Index Rises In JanuaryMarch 25, 2025 03:53 ETMalaysia’s leading index continued to improve in January, indicating that the economy remains on a positive trajectory. The leading index for Malaysia, which measures future economic activity, improved by 0.4 percent annually to 112.5 in January from 112.1 in December. The double-digit risess in the real imports of semiconductors and the number of housing units approved were the contributors.

BoJ Minutes On Tap For TuesdayMarch 24, 2025 17:59 ETThe Bank of Japan will on Tuesday release the minutes from its monetary policy meeting on January 23-24, highlighting a modest day for Asia-Pacific economic activity. At the meeting, the central bank raised its short-term interest rate to the highest in 17 years, aiming for a price stability target…

South Korea Consumer Sentiment Index Ebbs In March – BoKMarch 24, 2025 17:14 ETSouth Korea’s Composite Consumer Sentiment Index for March stood at 93.4, the Bank of Korea said on Tuesday – dipping from 95.2 in February. Consumer sentiment for current living standards was unchanged at 87, and the outlook was at 92, one point lower than in February. Consumer sentiment for future…