Kevin Carmichael: Brace for more big hikes because the Bank of Canada is far from finished

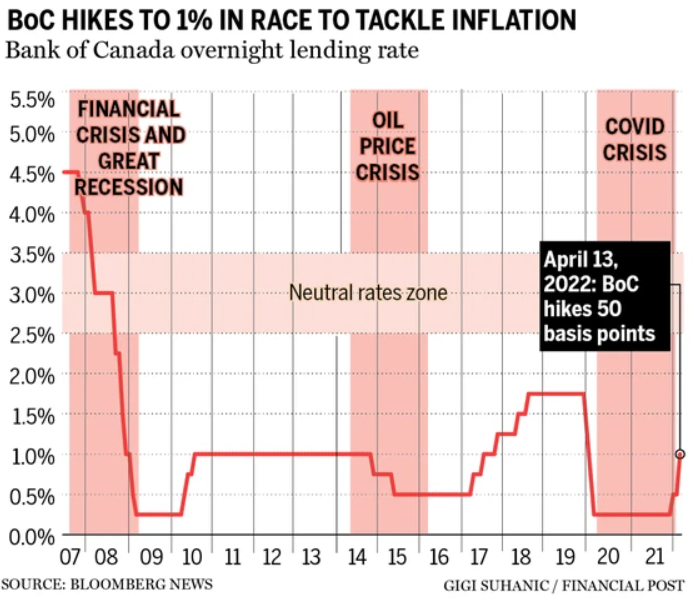

Governor Tiff Macklem and his deputies raised the benchmark interest rate by half a percentage point on April 13, an aggressive move since central banks generally prefer to move in quarter-point increments.

Policy-makers also said they would initiate “quantitative tightening,” which means the central bank will remove itself as an active participant in the bond market. The Bank of Canada purchased hundreds of billions of dollars of bonds during the recession to put additional downward pressure on interest rates, and had been reinvesting what it earned when those assets matured. The reinvesting will now stop.

The outsized increase in borrowing costs, which took the benchmark interest rate to one per cent, was widely anticipated; the central bank had telegraphed that stronger-than-forecast inflation would force it to accelerate its march to a more normal interest-rate setting.

Less anticipated, perhaps, was the extent to which the economy is straining on the central bank’s reins. Macklem’s new quarterly economic forecast has gross domestic product increasing at an annual rate of six per cent in the second quarter, which is a rate of growth you would expect in the earliest days of a recovery, not when the recovery is over and the jobless rate at a modern low.

“The Canadian economy is strong,” he said in the opening statement at his quarterly press conference. “The economy has fully recovered from the pandemic, and it is now moving into excess demand.”

By “excess demand,” Macklem meant the central bank’s forecast suggests the economy is now growing faster than its capacity to generate goods and services without stoking inflation. The Bank of Canada revised its estimate of the “output gap,” an important concept in central banking, if mostly meaningless to the rest of us, to between -0.25 per cent and 0.75 per cent, compared with an estimate of -0.75 per cent and 0.25 per cent in January.

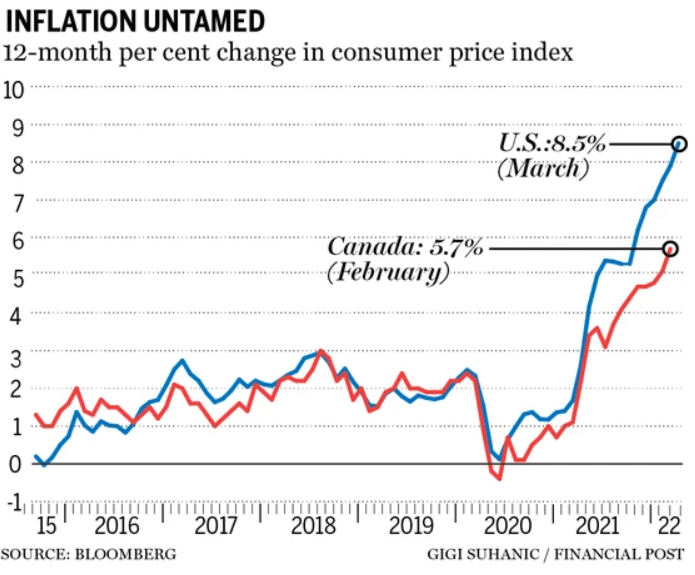

All that growth would be something to cheer if it wasn’t paired with equally strong inflation. The Bank of Canada acknowledged it underestimated how much the consumer price index would increase in the first quarter, and now predicts an average monthly gain of 5.6 per cent, compared with the 5.1 per cent it forecasted in January.

Policy-makers expect average headline inflation of 5.8 per cent in the second quarter, and forecast that price increases will remain well above the high end of their comfort zone — one per cent to three per cent — for the rest of the year.

“Today’s decision suggests the BoC is going on offence,” Charles St.-Arnaud, chief economist at Alberta Central and a former Bank of Canada staffer, said in a note to clients. “The door remains open to further (half-point) hikes.”

The Bank of Canada said the war in Ukraine was the primary reason it underestimated inflation. Russia and Ukraine are big exporters of oil, natural gas, wheat and other commodities, and prices for those important inputs have soared since Russian President Vladimir Putin’s invasion of Ukraine on Feb. 24.

As a result, the economy came out of the downturn firing on all cylinders. That’s creating more demand than there is supply, putting extra pressure on prices amid a war, drought, COVID-19 lockdowns and sundry other disruptions that have already put upward pressure on prices.

The Bank of Canada emphasized it is far from finished. Its new forecast discovered the economy is probably now operating at a level that exceeds estimates of what it can produce without stoking inflation. And yet the benchmark rate is still below its pre-pandemic level.

A second half-point increase when the central bank next updates its policy rate on June 1 would surprise no one.

Policy-makers said they are worried households and businesses will absorb current inflation as the new normal. The Bank of Canada is relying on its credibility with the public to keep expectations anchored.

Leave a Reply

You must be logged in to post a comment.