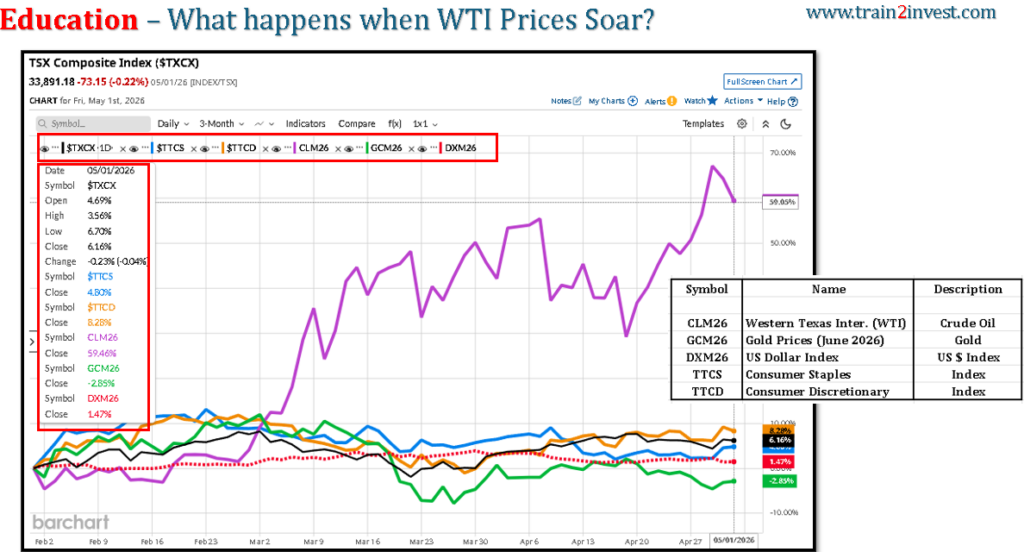

- The chart shows WTI crude (CLM26) rising sharply (~+59%) over ~3 months.

- TSX Composite (TXCX) rises modestly (~+6%), indicating partial positive correlation.

- Consumer Discretionary (TTCD) underperforms → pressured by higher energy costs.

- Consumer Staples (TTCS) is relatively stable → defensive behavior.

- Gold (GCM26) weakens (~−2.8%) while USD (DXM26) rises → typical risk/inflation dynamics.

What the Chart Is Showing (Data Interpretation)

Indexed Performance (approx from chart)

| Asset | Return | Direction |

|---|---|---|

| WTI Crude (CLM26) | +59% | Strong uptrend |

| TSX Composite (TXCX) | +6% | Moderate gain |

| Consumer Discretionary (TTCD) | +8.2% → fading | Weak relative |

| Consumer Staples (TTCS) | +4.8% | Stable |

| Gold (GCM26) | −2.8% | Declining |

| USD Index (DXM26) | +1.5% | Strengthening |

Key Drivers (Macro → Sector Transmission)

1) Macro: Oil Shock (Primary Driver)

- WTI +59% = major supply/demand imbalance

- Typically driven by:

- Geopolitical disruption (e.g., Hormuz risk)

- Supply constraints

Transmission:

- Higher oil → higher inflation expectations

- Central banks → maintain tighter policy

- Consumer purchasing power ↓

2) TSX Impact (Index Level)

- TSX is energy-heavy (~18–20%)

- Oil ↑ → Energy earnings ↑ → lifts index

Why TSX only +6% (not +59%)?

- Gains in energy offset by weakness in other sectors

- Consumer

- Industrials

- Rate-sensitive sectors

3) Sector-Level Effects

A) Consumer Discretionary (TTCD) → Weak

- Negative correlation with oil

Mechanism:

- Fuel costs ↑ → disposable income ↓

- Retail, autos, apparel demand ↓

Chart confirms:

- TTCD initially rises but loses momentum into late period

B) Consumer Staples (TTCS) → Defensive Stability

- Less sensitive to discretionary spending

Behavior:

- Holds value during inflation pressure

- Slight gain (~+4.8%) = capital preservation trade

C) Gold (GCM26) → Unexpected Weakness

- Normally benefits from inflation

Why down here:

- USD ↑ (− correlation with gold)

- Possibly:

- Real yields rising

- Liquidity tightening

D) USD Index (DXM26) → Rising

- Strong USD typically:

- Pressures commodities (except oil in supply shocks)

- Weakens gold

Economic Logic (Cause → Effect Chain)

WTI ↑ sharply →

- Inflation expectations ↑

- Interest rate expectations ↑

- Consumer spending power ↓

- Sector rotation:

- Into: Energy

- Out of: Discretionary

- TSX partially benefits due to energy weight

Valuation / Market Structure Insight

- This is a classic late-cycle / supply-shock setup:

- Energy = earnings upgrade cycle

- Consumer sectors = margin compression + demand risk

- Market is not pricing recession yet (since TSX still positive)

Risks (What Could Change This Relationship)

Short-term

- Oil reversal → immediate sector rotation back

- Weak economic data → TSX declines broadly

Medium-term

- Sustained oil > $100:

- Demand destruction risk

- Broader equity correction

Scenarios

Bull (for TSX)

- Oil stabilizes high but not rising

- Energy continues to lead

→ TSX +3–6%

Base Case

- Oil volatile, range-bound

→ Sector divergence continues

→ TSX flat to slightly positive

Bear Case

- Oil spike triggers recession fears

→ Broad selloff including TSX

→ −8–12%

What Would Disprove This Interpretation

- Discretionary stocks outperform despite rising oil

- Gold rises strongly alongside USD

- TSX declines despite energy strength

Actionable Takeaways

- Oil spikes create clear sector winners/losers:

- Winners: Energy, (sometimes) Financials

- Losers: Discretionary, Transport

- TTCD weakness is structural under oil shocks, not random

- TTCS acts as capital preservation, not growth

Leave a Reply

You must be logged in to post a comment.