The Bank of Canada held its benchmark interest rate steady on Wednesday, but warned that interest rates may need to change depending on the duration of the oil price shock and the outcome of trade talks with the United States and Mexico.

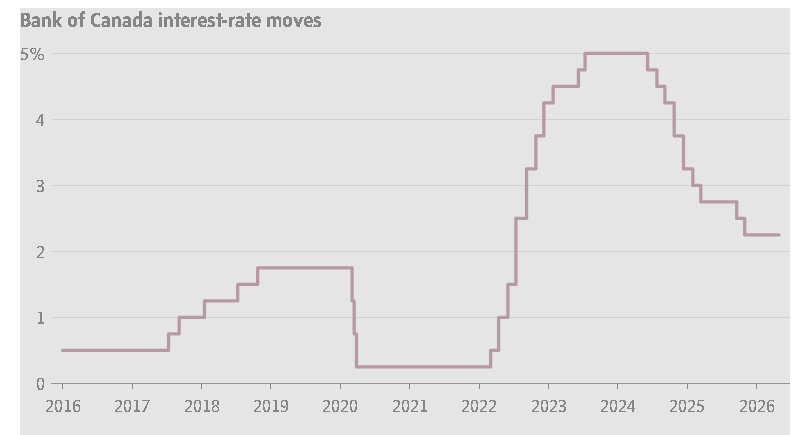

As widely expected, the bank’s governing council kept its policy rate at 2.25 per cent for the fourth consecutive time, even as the conflict in the Middle East has pushed energy prices sharply higher and squeezed Canadian consumers at the gas pump.

Governor Tiff Macklem said his team decided to “look through” the energy price shock in the near term. But he said the trajectory of monetary policy will depend to a significant degree on how long oil prices remain elevated – something that’s contingent on the outcome of peace talks between the United States and Iran.

“Our baseline forecast assumes oil prices will come down and U.S. tariffs will remain at current levels. If this holds true, a policy rate close to current settings looks appropriate,” Mr. Macklem said, according to the prepared remarks from his press conference opening statement.

Live updates on the Bank of Canada rate decision

In this situation, the bank may still need to adjust rates, but changes “can be expected to be small,” he said, in unusually candid remarks about the direction of monetary policy.

But the bank is also considering a scenario where oil prices remain elevated and start bleeding into other consumer prices, becoming generalized inflation.

“If this starts to happen, monetary policy will have more work to do – there may be a need for consecutive increases in the policy rate,” Mr. Macklem warned.

Global oil prices have gyrated wildly in recent weeks, reacting to each new headline from the U.S.-Iran peace talks. The price of a barrel of Brent crude hit US$117 on Wednesday morning, while West Texas Intermediate reached US$105. In January, the bank expected Brent would remain around US$60 over the next two years.

The energy price shock has pushed up gasoline prices in Canada and raised headline inflation in March to 2.4 per cent from 1.8 per cent the previous month. The bank expects headline inflation to increase to about 3 per cent in April.

“So far, there is little evidence that higher oil prices have fed through to other goods and services prices more broadly. But it is early days and we will be watching this closely,” Mr. Macklem said.

Oil prices aren’t the only source of uncertainty for the Canadian economy and for monetary policy. Mr. Macklem also highlighted the six-year review of the United States-Mexico-Canada trade agreement, which is scheduled to happen on July 1.

Officials from all three countries have said they expect negotiations to continue past the summer deadline, and the future of the trilateral agreement remains uncertain.

“If the United States imposes significant new trade restrictions on Canada, we may need to cut the policy rate further to support economic growth,” Mr. Macklem said.

The two-sided uncertainty is unfolding against the backdrop of a sluggish Canadian economy that’s been battered by U.S. tariffs but supported by resilient consumers and increased government spending at both the provincial and federal level.

The bank’s baseline forecast, published in its quarterly Monetary Policy Report (MPR) on Wednesday, sees Canadian gross domestic product growing 1.2 per cent in 2026 and 1.6 per cent in 2027 – slightly higher than the January forecast.

GDP is expected to grow by 1.5 per cent in the first quarter at an annualized pace – slower than the 1.8 per cent expected in January.

Meanwhile, the bank upgraded its forecast for consumer price index inflation due to the energy price shock. The bank expects headline inflation to average 2.3 per cent in 2026, up from the previous forecast of 2 per cent. It expects inflation to peak at around 3 per cent in April, before declining to 2.5 per cent in June and 2 per cent by early 2027.

Both the GDP and inflation forecasts are heavily contingent on fragile assumptions about oil prices and tariffs.

The baseline forecast – based on oil futures markets – assumes that Brent crude prices will gradually decline from US$90 a barrel in the second quarter to US$75 by mid-2027. The average tariff rate on Canadian goods shipped to the United States is assumed to remain at 5.1 per cent.

“If the United States imposes new trade restrictions on Canada, GDP growth would be weaker and inflationary pressures lower,” the bank said in the MPR. “But if the war in the Middle East continues and global energy prices rise further and stay high for longer, price pressures could broaden and become more persistent.”

The energy price shock is expected to have a mixed impact on the Canadian economy. Higher oil prices boost exports and generate profits for energy companies and tax revenues for Ottawa and the provincial governments. At the same time, consumers are squeezed at the gas pump, leaving them with less discretionary income to spend.

“Higher global oil prices are expected to have little impact on overall growth but will affect its composition,” the MPR said.

Alongside its main forecast, the bank outlined an “illustrative” scenario where oil prices remain at US$100 for the next few years. In this situation, GDP growth is similar to the baseline scenario, but interest rates are higher as the bank is forced to react to inflationary pressures.

“There are many possible outcomes. Monetary policy may need to be nimble,” Mr. Macklem said.

Leave a Reply

You must be logged in to post a comment.