Elbows UP?

More like pants down!

Compared to Other G7 countries:

Canada ranks as one of the smaller G7 economies by total GDP but performs solidly in several areas, though it lags in per capita terms and productivity growth. The G7 includes Canada, the US, UK, Germany, France, Italy, and Japan. Here’s a comparison based on recent data (primarily 2025–2026 projections from IMF, OECD, and national sources).

Total GDP (Nominal, 2026 Projections)

Canada has the smallest or near-smallest total economy in the G7:

- US: ~$32.4 trillion (by far the largest)

- Germany: ~$5.0–5.5 trillion

- Japan: ~$4.3 trillion

- UK: ~$3.9–4.0 trillion

- France: ~$3.4 trillion

- Italy: ~$2.5–2.6 trillion

- Canada: ~$2.51 trillion (11th globally)

Canada’s economy is resource-heavy (energy, commodities) and closely tied to the US via trade.

GDP Growth

Canada has shown resilience in total GDP growth, often ranking near the top of the G7, largely driven by population growth (immigration).

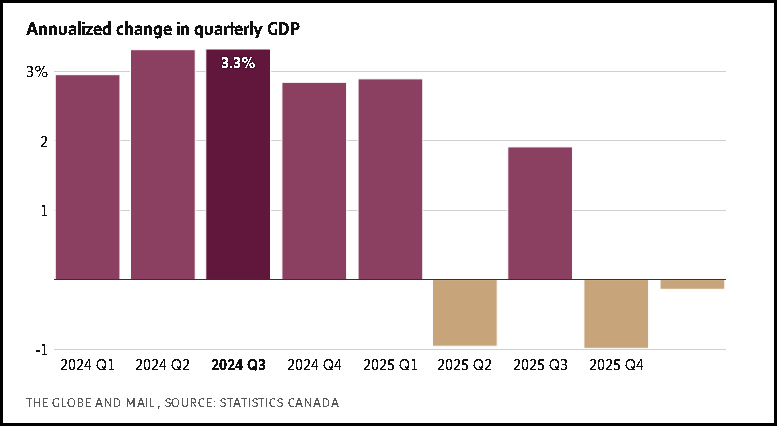

- Recent performance: It entered a TECHNICAL RECSSION with contractions in late 2025 and Q1 2026 (e.g., -1.0% in Q4 2025, -0.1% in Q1 2026 annualized).

- Longer-term: Strong total GDP growth since the 2000s (often 2nd to the US), but this is heavily population-driven.

GDP Per Capita

This is where Canada lags:

- Canada’s per capita GDP (~$60,300 in recent IMF data) is solid but trails the US, UK, and Germany significantly.

- Per capita growth has been weak or negative in recent years due to rapid population increases outpacing output. Canada had the worst per capita GDP growth in the G7 from 2014–2023 in some analyses.

- This reflects lower productivity growth compared to peers.

Unemployment

Canada’s rate is higher than the G7 average:

- Canada: ~6.7–6.9% as of early-mid 2026 (second-highest in G7 behind France in some periods).

- G7 average: ~4.6–5.3%.

- Lower rates in Japan (~2.5%), Germany (~3–4%), and the US.

Canada’s labour market has softened with higher immigration and slower hiring.

Debt and Fiscal Position

- Government debt-to-GDP: Canada ~103–111% (mid-range in G7). Better than Japan (>200%), Italy (~135%), and the US (~121%), but worse than Germany (~64%).

- Canada has a relatively smaller deficit than the US but has seen rising debt burdens in recent years.

Other Factors

- Inflation: Canada has generally managed it better than some G7 peers post-pandemic.

- Strengths: Resource exports, trade ties with the US (USMCA), fiscal soundness relative to some peers, and adaptability.

- Challenges: Productivity stagnation, housing affordability, reliance on immigration for growth, energy price volatility, and recent trade/tariff pressures. Per capita metrics and business investment have been weak.

Summary: Canada has one of the smallest total economies in the G7 but often ranks high in total GDP growth thanks to population gains. It underperforms on per capita growth, productivity, and unemployment compared to top peers like the US and Germany. Its economy remains resilient and resource-rich but faces structural issues around living standards and efficiency. Data can shift with new releases from IMF/OECD/Statistics Canada.

Globe & Mail: May 29/2026

The Canadian economy stalled in the first quarter of the year, posting a small, annualized decline in gross domestic product as the country struggles to grow in the face of trade tensions with the United States.

Canada’s real GDP contracted 0.1 per cent on an annualized basis between January and March, Statistics Canada reported Friday. This was much weaker than the 1.5-per-cent growth predicted by economists at the Bank of Canada and on Bay Street and follows a 1-per-cent decline in the fourth quarter of 2025.

Two consecutive quarters of negative GDP growth is sometimes referred to as a “technical recession.” However, economists cautioned that it may be premature to use the term, as the first-quarter decline was small, and could easily be revised upward.

The last time the country saw back-to-back quarterly declines in GDP was at the outset of the COVID-19 pandemic in 2020. The Canadian economy has now contracted in three of the past four quarters.

“While there will be plenty of debate over whether this constitutes a recession (we would say ‘no, not really’) ???????, there is little debate that the economy has struggled to make any headway over the past year amid the ongoing trade conflict,” Douglas Porter, chief economist at the Bank of Montreal, wrote in a note to clients.

On a per capita basis, GDP rose 0.2 per cent compared with the previous quarter, as the population declined for the second consecutive quarter on the heels of more restrictive immigration policy.

Statscan’s separate monthly GDP report, published Friday, showed a 0.1 per cent month-to-month decline in March. An advanced estimate for April showed 0.4-per-cent growth, suggesting the economy began to pick up steam at the start of the second quarter.

The weak first-quarter number likely reinforces the case for the Bank of Canada to remain on hold in the coming months. The central bank has kept its policy rate at 2.25 per cent for four consecutive decisions. Recently, it has had to balance upside risks to inflation from the global oil price shock with downside risks to inflation stemming from slack in the Canadian economy.

“Overall, this should really throw a wet blanket on rate-hike talk, as the economy is in no condition to deal with higher rates,” Mr. Porter wrote.

Financial markets have pulled back on their expectations for multiple rate hikes from the Bank of Canada this year, but still see one quarter-point hike, in December, according to Bloomberg data.

Geopolitical, trade risks pose rising threat to financial stability, Bank of Canada warns

The first quarter GDP contraction was led by a combination of weak investment and a jump in imports, which are subtracted from the GDP tally.

Government capital investment fell 2.5 per cent quarter-to-quarter, as Ottawa slowed its pace of spending on new weapons systems.

Business capital investment fell 0.7 per cent – the fifth consecutive quarterly decline – with higher spending on machinery and equipment and mineral exploration offset by a decline in spending on engineering structures.

“Business investment continues to be the Achilles’ heel of the Canadian economy,” Marc Desormeaux, economist and vice-president of policy at the Business Council of Canada, said in an interview.

“The big thing is uncertainty – uncertainty around trade policy, uncertainty around geopolitical developments,” he said, pointing to the upcoming review of the United States-Mexico-Canada trade agreement.

Meanwhile, the soggy housing market continued to be a drag, with resale housing activity down 9.9 per cent in the first quarter, following a 3.4-per-cent decline in 2025 overall.

A big jump in imports compared with exports also dragged down the GDP calculation in the first quarter. Imports were up 2.9 per cent, driven by imports of gold, passenger cars and industrial machinery and equipment. By contrast, exports were down 0.1 per cent in the quarter, with fewer shipments of cars and trucks heading to the U.S. because of tariffs.

Consumer spending grew 0.4 per cent in the quarter, following a 0.7-per-cent increase in the fourth quarter of 2025. Increases in spending on financial services and food were offset by lower spending on vehicles.

“Overall this was a very weak report from most angles that shows that trade uncertainty and tariffs are continuing to hold back growth, while consumers have little ammunition left for spending ahead, and interest-sensitive sectors are lagging,” Katherine Judge, senior economist with Canadian Imperial Bank of Commerce economist, wrote in a note to clients.

“Our base case also assumes progress towards reducing some tariffs (namely aluminum and possibly steel) in the coming months, and if the oil price shock starts to fade over that period as well, GDP will return to sustainable growth for the rest of the year,” she wrote.

Conservative MPs pounced on the report Friday to criticize the Liberal government’s economic record, leaning into the notion that the country is in a “technical recession.”

Mark Carney “has been Prime Minister for four quarters now. The economy has shrunk in three of those quarters,” Conservative Leader Pierre Poilievre told reporters.

Finance Minister François-Philippe Champagne defended the government’s record in Friday’s Question Period, saying “Canadians understand that the world is facing some headwinds.”

With a report from Bill Curry

{NOTE: Bill Curry is a veteran parliamentary reporter with Liberal Bias}

Jonathan Chandran

President/CEO

TRAIN2INVEST

The Power To Prosper

Tel.: 204-488-3559

Email: admin@train2invest.com