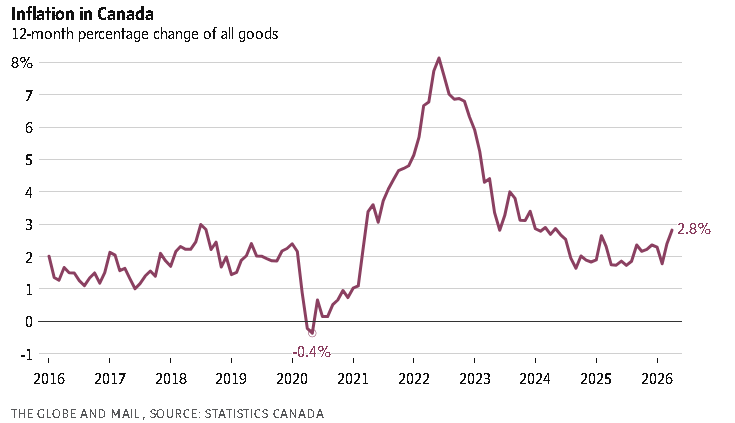

Higher gas prices driven mainly by the war in Iran pushed the annual rate of inflation up to 2.8 per cent in April, Statistics Canada said Tuesday – the fastest pace of price hikes in almost two years.

StatCan said the cost of gasoline was 28.6 per cent higher year-over-year last month as conflict in the Middle East disrupted global oil shipments, sending costs soaring at the gas pumps. April also marked the switch to more expensive summer gasoline blends at gas stations in Canada.

The agency noted the federal government’s move to suspend the fuel excise tax mid-month helped moderate the April price increase.

StatCan’s April report marks a jump from March’s inflation rate of 2.4 per cent, though a Reuters poll of economists had expected inflation would accelerate even more to top three per cent. The April figures mark the highest annual inflation rate since May, 2024.

Ottawa’s decision to remove the consumer carbon price a year earlier meanwhile skewed the annual price comparison higher in April.

Nixing the carbon price took roughly 18 cents off the price of a litre of gas in April, 2025. While that move took some steam out of the headline inflation rate over the past 12 months, that reduction has now fallen out of the annual comparison – pushing inflation higher rather than depressing it.

Prices for clothing and footwear rose two per cent in April, coming off a decline of 0.4 per cent in March.

StatCan said an 11 per cent annual price drop for travel tours in April and a slowdown in rent inflation nationally helped offset rising energy costs. Rent hikes have especially eased in British Columbia as its population shrinks; StatCan noted the province was the only one that didn’t see its inflation rate accelerate in April.

CIBC senior economist Andrew Grantham said in a note to clients Tuesday that higher prices for airfares tied to spiking fuel costs were not captured in the April inflation data, because those transactions are recorded when the flight is taken – not when the ticket is purchased. He said he expects to see those pressures show up more in the summer inflation readings.

Food inflation also eased to 3.5 per cent in April, down from four per cent in March, as grocery items such as chicken, fresh vegetables, coffee and tea saw their pace of price hikes slow following sharp increases earlier in the year.

The April figures mark the Bank of Canada’s last look at inflation data before the bank makes its next interest rate decision on June 10.

The central bank has held its policy rate steady at 2.25 per cent in its last four decisions.

TD senior economist Leslie Preston said in a note that knock-on effects from the Iran war oil shock are not yet showing up in non-energy segments of the consumer basket.

The Bank of Canada’s closely watched core inflation metrics cooled more than expected in April, Preston said, offering “little argument” for rate hikes from the central bank.

Grantham said the soft core inflation readings suggest there’s slack in the Canadian economy, which will continue to keep a lid on inflation even as higher gas prices work their way through other components in the months ahead.

“Because of that, we continue to see the Bank of Canada holding interest rates steady at their current level throughout 2026,” Grantham said.