Magna International Inc. reported a loss attributable to the company of US$12 million in its latest quarter compared with a profit of US$146 million a year earlier.

The Ontario-based automotive supplier, which keeps its books in U.S. dollars, says the loss amounted to four cents per diluted share for the quarter ended March 31 compared with a profit of 52 cents per diluted share a year ago.

On an adjusted basis, Magna says it earned US$1.38 per share in its latest quarter compared with an adjusted profit of 78 cents US per share a year earlier.

Sales totalled US$10.38 billion for the quarter, up from US$10.07 billion in the first quarter of 2025.

In its updated outlook, Magna says it now expects its sales for 2026 to total between US$41.5 billion and US$43.1 billion, down from its earlier forecast for between $41.9 billion and US$43.5 billion.

Magna is one of the world’s largest automotive suppliers and has operations across 28 countries around the world.

This report by The Canadian Press was first published May 1, 2026.

Here are the top 15 dividend payers in Canada, ranked by estimated total annual dividend payout (total cash dividends paid per year, calculated as dividend yield × market cap). This is the standard way to identify the largest “dividend payers” by absolute dollar amount distributed to shareholders.

These are drawn from the largest Canadian companies by market cap (as of late March 2026 data), excluding non-payers like Shopify. All figures are in billions of CAD (shown as $B), with market caps and TTM (trailing twelve months) net income as the latest available annual profit proxy. Dividend $ per year is an estimate based on current trailing dividend yield.

Key notes:

Dividend $ per year = total company-wide payouts (not per share). This metric highlights the biggest distributors of cash to shareholders.

Latest annual Profit uses TTM net income as the most recent full-year equivalent.

Data reflects March 2026 market conditions; actual payouts can vary with dividend increases, share buybacks, or earnings. Yields and totals are trailing (based on recent dividends).

Classic Canadian dividend heavyweights (big banks + major energy infrastructure/oil producers) dominate the list, as expected. Smaller high-yield names (e.g., some telecoms like Telus or BCE) have lower total payouts due to smaller market caps.

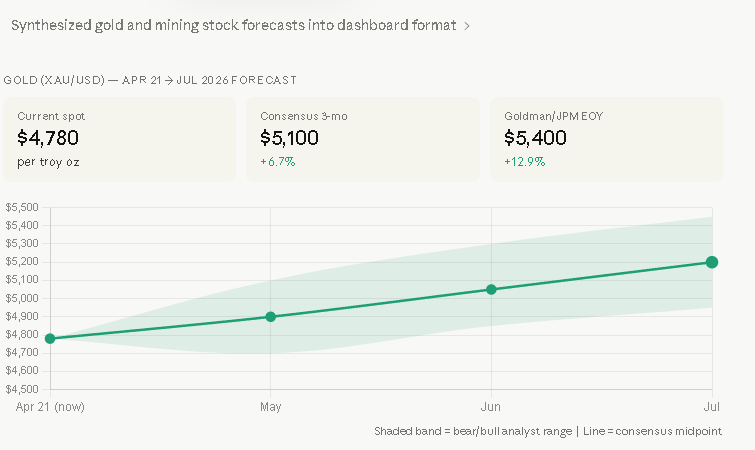

The March pullback (–10%, worst since 2013) was driven by USD strength during the US-Iran flare-up. It’s now holding above the $4,400–$4,600 support zone flagged as technically significant by several institutions. That’s consolidation after a historic run, not a structural break. GoldSilver

3-month consensus path: $4,900 (May) → $5,050 (Jun) → $5,200 (Jul). Goldman Sachs reaffirmed a $5,400 target by end-2026; J.P. Morgan’s updated call is $6,300. Citi raised its short-term target to $5,000, citing heightened geopolitical risks, physical market shortages, and renewed uncertainty over Fed independence. GoldRepublicSBC Gold

Key tailwind: central banks purchased 863.3 tonnes of gold in 2025 — more than double the 2010–2021 annual average — and 95% of respondents to the World Gold Council’s survey expect global reserves to increase over the next 12 months. GoldSilver

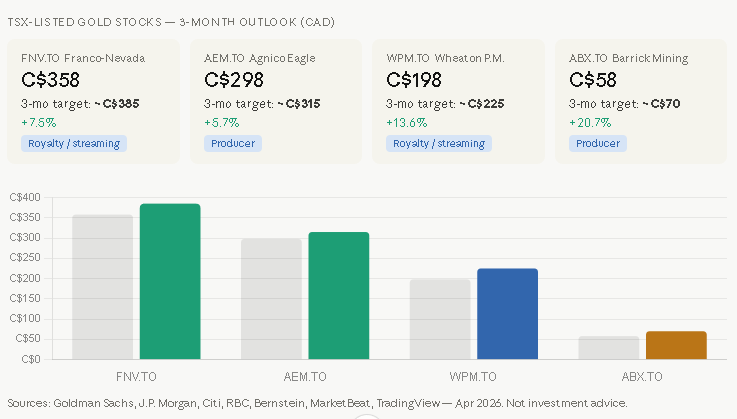

The four TSX stocks

FNV.TO (Franco-Nevada) — C$358 → ~C$385 (+7.5%) The royalty model gives it the cleanest leverage to gold without operational drag. Recent analyst targets sit in the US$280–$305 range. H.C. Wainwright lifted its target to US$305, and BofA moved to US$280 after updating its 2026 metal price forecasts. Lowest near-term upside of the four, but lowest risk profile. Yahoo Finance

AEM.TO (Agnico Eagle) — C$298 → ~C$315 (+5.7%) Analysts hold a Strong Buy consensus (8.5/10), with a median USD target of $205 and a high of $256. At ~C$298 it’s already trading above the USD median, meaning the market has partially priced in the gold rally. Upside is real but capped near-term unless gold breaks $5,200+. Ticker Nerd

WPM.TO (Wheaton Precious Metals) — C$198 → ~C$225 (+13.6%) Hit an all-time high of C$226.68 on March 2, 2026, and has since pulled back ~12%. TradingView analysts peg a CAD range of $204–$357. As a streaming company it has high operational leverage and the best risk-reward near-term among the four. TradingViewTradingView

ABX.TO (Barrick Mining) — C$58 → ~C$70 (+20.7%) The highest potential upside and the most controversy. Bernstein and JPMorgan both raised their targets to C$91; Stifel is at C$95. TradingView consensus sits at C$81.64 (max C$95, min C$55). The stock has significantly underperformed gold itself — copper exposure and operational complexity are the drag. If gold stays above $5,000, the discount closes fast. Markets DailyTradingView

Not investment advice. Analyst targets are 12-month figures; 3-month extrapolations are proportional estimates. CAD prices use ~1.38 USD/CAD.

ECB’s monetary policy meeting and Bank of England rate decision

8:30 a.m. ET: Canada’s monthly real GDP for February. Consensus is a rise of 0.2 per cent from January.

8:30 a.m. ET: Canada’s payroll survey for February.

8:30 a.m. ET: U.S. GDP and GDP price index for Q1. The consensus projections are annualized rate increases of 2.1 per cent and 4.0 per cent, respectively.

8:30 a.m. ET: U.S. personal spending and income for March. The Street expects month-over-month rises of 0.9 per cent and 0.3 per cent, respectively.

8:30 a.m. ET: U.S. core PCE price index for March. Consensus is a gain of 0.3 per cent from February and up 3.2 per cent year-over-year.

8:30 a.m. ET: U.S. employment cost index for Q1. Consensus is a rise of 0.8 per cent from Q4 and up 3.3 per cent year-over-year.

8:30 a.m. ET: U.S. initial jobless claims for week of April 25. Estimate is 212,000, down 2,000 from the previous week.

Crude oil hit its highest level since 2022 amid reports that the U.S. is considering new attacks on Iran and President Donald Trump’s warning that his blockade of Iranian ports could last months. The price surge came as new economic figures show that high oil prices are stoking inflation and hurting growth.

Eurozone inflation rose to 3 per cent in April, up from 2.6 per cent in March. The latest reading surpassed the 2.9 per cent forecast by a Reuters poll of economists. April is the second consecutive month that inflation has exceeded the European Central Bank’s medium-term inflation target of 2 per cent.

Oil’s spike on Wednesday and Thursday seemed to indicate waning hope that the Strait of Hormuz would reopen soon, triggering concerns from some economists that the crippling cost for hydrocarbons could plunge the world into recession. Iran has said it will not reopen the strait until the U.S. ends its blockade on Iranian shipping.

In early London trading, Brent crude, the international benchmark, hit US$126 a barrel before traders pared back the gains to US$116. The two-day rally had lifted prices by about 13 per cent before the late morning price reversal.

The last time oil went above US$120 was in March, 2022, during the early stages of Russia’s invasion of Ukraine.

Hormuz, through which 20 per cent of the world’s oil and liquefied natural gas (LNG) shipments pass, has been almost totally closed since Feb. 28, when the U.S. and Israel began their bombing campaign against Iran. The Islamic Republic in response mined the strait and attacked some ships, preventing all but a few tankers from reaching world markets.

Sporadic peace talks since then have gone nowhere. A ceasefire has been in place since April 8.

Axios reported late on Wednesday that U.S. Central Command has drawn up a plan for “short and powerful” strikes on Iran that could include infrastructure targets. Admiral Brad Cooper, head of Central Command, is due to brief Mr. Trump on Thursday, boosting speculation that attacks are imminent. Mr. Trump told Axios that he plans to keep the U.S. blockade of Iranian ports intact.

“Trump has ripped away the security blanket the market was clinging to — the hope that the war was about to end,” said Robert Rennie, head of commodity research at Westpac Banking Corp. “Traders are now being forced to confront a much uglier reality: both sides still think they are winning, neither side has a clear incentive to negotiate, and energy prices are starting to accelerate higher.”

Asian markets lost ground as oil climbed. Hong Kong’s Hang Seng was down 1.28 per cent and Japan’s Nikkei lost 1 per cent. By Thursday mid-day Germany’s DAX index was up marginally and London’s FTSE 100 was up 1 per cent.

Hormuz’s shutdown removes about 20 million barrels a day of oil from the Persian Gulf. Some of the missing oil can be made up by higher production from other OPEC countries, inventory drawdowns and releases from government-controlled strategic petroleum reserves in the U.S. and elsewhere. But those efforts nowhere near cover the full loss, which is why prices have been rising.

In a new blog post, Oxford Economic said that oil prices could go to US$190 a barrel if Hormuz remained shut for six months. That price would surpass the all-time high of US$147 a barrel in 2008, just ahead of the global financial crisis.

Diesel and aviation fuel prices have climbed even faster. Many airlines are cutting back their flight schedules for fear of fuel shortages, and raising ticket prices and adding fuel surcharges. In the U.S., diesel has climbed almost US$2 a gallon over their average price a year ago, according to the AAA Fuel Prices monitor.

Rising fuel prices are stoking inflation everywhere. U.S. annual inflation climbed to 3.3 per cent in March.

Economic expansion is also slowing. New figures show that Eurozone growth slowed to 0.1 per cent in the first quarter of the year following growth of 0.2 per cent in previous quarter. Germany’s growth remained intact but France’s was stagnant.

Since the first quarter included only one month of the war on Iran, economists are warning that the second quarter figures could be weaker.

On April 20, economist Paul Krugman, a former New York Times columnist, said in his Substack, “In my view, a full-on global recession is more likely than not if the strait remains closed for, say, another three months, which seems all too possible.”

The International Energy Agency said the Hormuz shutdown has delivered the world the biggest energy supply shock in history.

Hormuz’s shutdown is putting agriculture markets under stress. Between 20 and 30 per cent of global fertilizer exports normally pass through the strait. Shortages of natural gas-derived urea and ammonia are pushing prices up.

“Higher prices could reduce fertilizer use and lower crop yields if the disruption persists, posing significant food security risks,” the International Food Policy Research Institute said in an early April report. “Most vulnerable are countries heavily dependent on Persian Gulf fertilizer and natural gas, especially in Africa and South Asia.”

Pembina Pipeline (PPL-T +1.25%increase, Monday’s close: $58.17) advanced from $38.79 in October 2023 to $60.72 in November 2024 (A–B), supported by a rising trendline (dotted) and its rising 40-week moving average (40WMA).

stock

Following this advance, the stock settled in a consolidation phase, trading largely within a horizontal range between $49 and $58 (dashed lines). The recent move above the upper boundary of this range signals a breakout and suggests the start of a new uptrend toward higher targets (C).

Trend indicators, including the rising 40WMA, continue to confirm a bullish outlook. The stock is currently undergoing a modest pullback toward its moving average, offering a potentially favourable entry point. Only a sustained decline below the 40WMA (currently near $54–55) would weaken this positive view.

CGI Inc. GIB-A-T -14.80%decrease says it earned $444.7-million in its second quarter compared with a profit of $429.7-million a year earlier.

The business and technology consulting firm says the profit amounted to $2.09 per diluted share for the quarter ended March 31, up from $1.89 per diluted share in the same quarter last year.

On an adjusted basis, CGI says it earned $2.27 per diluted share in its latest quarter, up from an adjusted profit of $2.12 per diluted share a year earlier.

Revenue for the quarter totalled $4.16-billion, up from $4.02-billion in the same quarter last year.

Bookings for the quarter totalled $4.31-billion, while CGI’s backlog stood at $31.50-billion at March 31.

CGI has 94,000 consultants and professionals across the globe that provide business and technology consulting services.

IF you have been wondering what meaning to attach to that irritating phrase the Carney Liberals use to describe themselves, “Canada’s New Government” – which was irritating enough when it was first employed, under Stephen Harper, when it was actually a new government – wonder no longer. As this Spring Economic Update makes abundantly clear, it means nothing whatever. Or next to nothing.

Well, I suppose it depends on whether you are looking at things in static or dynamic terms. So whereas the Trudeau government did all sorts of things that steadily made matters worse, fiscally and economically speaking, the all-new Carney government will do almost nothing to make them better.

This is, remember, the Carney government’s second crack at it. The first, last fall’s budget, was extravagantly hyped beforehand, but delivered very little. Tuesday’s update, by contrast, came with next to no advance hype, and delivered very little. So the government is at least managing expectations better than it was. But in substance it amounts to more of the same.

The basic issues in front of the government are, not coincidentally, also unchanged. They are 1) the deteriorating state of the country’s finances, and 2) the snail-like pace of economic growth, a problem that has been growing steadily worse for decades.

On the deficit and debt situation, things are if anything worse than before. The Trudeau government ran through a series of fiscal “guardrails,” later changed to “anchors,” each one more forgiving than the last. Balanced budgets, of course, are but a fond memory. So is the “declining debt-to-GDP ratio” that replaced them. Ditto for “deficits smaller than one per cent of GDP.”

The Carney government set even less exacting targets for itself. Now it’s a steadily declining deficit-to-GDP ratio, plus that mumbo-jumbo about achieving “day-to-day operating balance” (a concept nowhere defined), eventually, while continuing to borrow for capital spending (also undefined), more or less indefinitely.

But the deficit for fiscal 2026, at 2.1 per cent of GDP, was higher, proportionately, than it was in fiscal 2025, and is projected to remain at similarly elevated levels this year and next. What’s the fastest-growing government program? Interest on the debt, projected to cost, four years out, more than $80-billion, or 13 cents of every tax dollar. Four years ago it was just 6 cents.

The new government, like the old, cannot even be bothered to present the current figures in a meaningful fashion. The federa

The provinces’ net debts, collectively, are north of 30 per cent. The combined federal-provincial debt, according to a recent report from the C.D. Howe Institute, is at about 75 per cent of GDP today, on its way to 82 per cent by fiscal 2029.

On what basis, then, does the government continue to insist that Canada’s all-government net debt-to-GDP ratio is at just (checks notes) 10.2 per cent? By subtracting the assets held by the Canada Pension Plan and Quebec Pension Plan, funds that appear on neither the federal nor the provincial governments’ balance sheets – and, more important, are not available to either to pay off their debts.

The picture is even bleaker on the growth side. Yes, things could be worse. The tariff shock is wearing off. Inflation is contained. Interest rates are falling. But the government’s own long-term projection is for growth averaging 1.7 per cent after inflation. That’s a third as fast as we grew in the 1950s and 60s. It’s half as fast as in the 1970s and 80s.

That’s a major contributor to high deficits. But high deficits also hurt growth, crowding out productive private investment. So do high tax rates and unnecessary regulation – especially the kind that protects cozy industrial oligopolies from competition, such as those that now stifle the telecoms, financial services and airline industries.

What, then, does “Canada’s New Government” propose to do about these? Sweeping, pro-investment tax reforms? Radical steps to open protected sectors to competition? No and no. It’s more of the same incremental noodling and state-directed wheel-spinning that got us here. Complacency on taxes, “sector strategies” for every industry under the sun, etc. etc. etc.

A “whole of government competition plan” sounds promising, until you discover that it’s just more hedge-trimming: a watery promise to “limit to the extent possible the potential negative impacts on competition that can, often inadvertently, stem from government policies.” I say, how frightfully stimulating.

Oh, and there’s the Canada Strong Fund, advertised as “Canada’s first sovereign wealth fund,” about which more on another occasion.

There’s no use being disappointed. By this stage, we should all be managing our own expectations. Canada’s New Government is no more interested in arresting our economic decline than Canada’s Old Government.