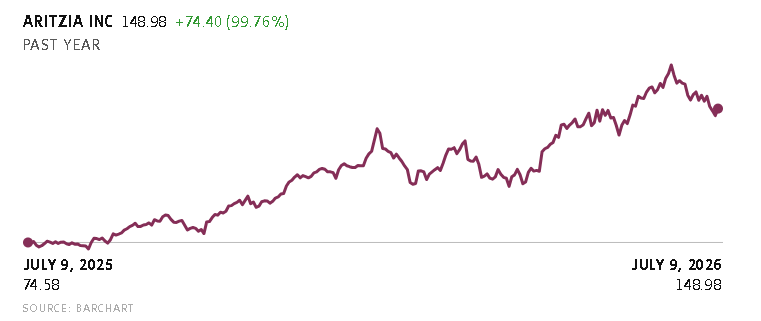

Canadian fashion retailer Aritzia Inc. ATZ-T +7.43%increase reported a year-over-year doubling of its profits in the first quarter, and it boosted its sales forecasts for this year, as the brand’s styles continue to prove popular with shoppers.

“It starts with product. Product is central, and it’s the heart of what we do, and we’ve gotten the product right,” chief executive officer Jennifer Wong said on a conference call on Thursday to discuss the company’s earnings.

Aritzia’s spring and summer collections have performed well, allowing the stores to sell fewer items on markdown. The company has also been investing more in marketing to win over new shoppers, and to maintain awareness among its existing customers.

The retailer has developed a healthy balance between new styles and recurring bestsellers, which is continuing to attract people to the stores, Ms. Wong said, along with an ability to keep up with trends.

“An integral part of our business model is our ability to flex our inventory in-season to meet demand,” she said.

The Vancouver-based clothing maker reported net income of $117.3-million, or 99 cents per diluted share, in the quarter ended May 31, compared to $42.4-million, or 36 cents per diluted share, in the same period last year.

Aritzia has been expanding its store footprint in the United States, and the country accounted for roughly two-thirds of its revenues in the first quarter. Sales grew faster south of the border than in Aritzia’s home market, but Canadian net revenue still increased by 25 per cent.

The company reported its total revenue grew by 43 per cent compared to the same period last year, to $951-million.

Comparable sales – a metric that tracks sales growth only in stores open for more than one year to exclude the impact of new store openings – increased by 35 per cent in the quarter.

On Thursday, the company also updated its forecast for the current fiscal year, reporting that it expects annual sales to jump by 23 per cent to 28 per cent, to a range of $4.55-billion to $4.75-billion. Its previous forecast had predicted revenue for the year in the range of $4.4-billion to $4.6-billion.

“I’ve never been more confident in the business than I am right now,” Ms. Wong said.

Some of that growth will be driven by continued store expansion, with 12 to 13 new locations planned for this year, and four to five updates to existing stores, either through renovations or relocations. Most of the new stores will be in the U.S.

In May, Aritzia opened a new distribution centre in British Columbia to support its expansion plans. New stores have been earning back their investment in under a year on average, Ms. Wong said, which has outpaced the company’s expectation of 12 to 18 months.

Aritzia locations have also been getting bigger, which helps each store to generate more sales: Roughly a decade ago, its locations averaged roughly 6,000 square feet, while new stores now average more than 10,000 square feet.

When the company opens new stores, it also sees an approximate 70-per-cent lift in e-commerce sales in the surrounding area in the first year on average, chief financial officer Todd Ingledew said during the call.

“So it continues to be very meaningful contributor to our overall growth, and we’re really pleased with the performance of the new stores,” he said.