Suncor Energy SU-T -3.56%decrease on Tuesday beat analysts’ estimates for second-quarter adjusted profit, helped by higher crude price realizations and stronger refining margins.

Oil prices, boosted by the Iran war, have strengthened earnings prospects for Suncor and its oil sands peers, with Brent’s climb toward US$100 a barrel reinforcing Canada’s pitch as a safer, chokepoint-free alternative to Gulf crude.

Suncor’s refinery crude oil throughput rose to a second-quarter record of 470,600 barrels per day from 442,300 barrels per day, while its refinery utilization increased to 92 per cent from 87 per cent.

However, its total upstream production fell to 760,900 barrels per day from 808,100, partly due to a planned Firebag turnaround.

The Calgary, Alberta-based company posted adjusted operating earnings of $3.23 per share for the quarter ended June 30, above analysts’ average estimate of $3.07 per share, according to data compiled by LSEG.

Aug. 5: Chorus Aviation Inc. (CHR-T), Flagship Communities REIT (MHC-UN-T), Kinaxis Inc. (KXS-T), Doman Building Materials Group Ltd. (DBM-T), Propel Holdings Inc. (PRL-T), Xanadu Quantum Technologies Ltd. (XNDU-T), Thinkific Labs Inc. (THNC-T), AirBoss of America Corp. (BOS-T), Kits Eyecare Ltd. (KITS-T), Galaxy Digital Holdings Ltd. (GLXY-T), Pizza Pizza Royalty Corp. (PZA-T), Aurora Cannabis Inc. (ACB-T), Savaria Corp. (SIS-T), Dorel Industries Inc. (DII-B-T), Sprott Inc. (SII-T)

Aug. 6: NFI Group Inc. (NFI-T), Enerflex Ltd. (EFX-T), Interfor Corp. (IFP-T), Cascades Inc. (CAS-T), Plaza Retail REIT (PLZ-UN-T), Rogers Sugar Inc. (RSI-T), Cronos Group Inc. (CRON-T), Profound Medical Corp. (PRN-T), TerrAscend Corp. (TSND-T), Premium Brands Holdings Corp. (PBH-T), Altus Group Ltd. (AIF-T), Goeasy Ltd. (GSY-T), Alaris Equity Partners Income Trust (AD-UN-T), Medical Facilities Corp. (DR-T), VitalHub Corp. (VHI-T), Knight Therapeutics Inc. (GUD-T)

Aug. 7: Superior Plus Corp. (SPB-T), Docebo Inc. (DCBO-T), Trulieve Cannabis Corp. (TRUL-CN), Slate Grocery REIT (SGR-UN-T), DRI Healthcare Trust (DHT-UN-T), Fiera Capital Corp. (FSZ-T)

Aug. 10: Cargojet Inc. (CJT-T),Silvercorp Inc. (SVM-T), Altius Minerals Corp. (ALS-T)

Aug. 11: Neo Performance Materials Inc. (NEO-T), Pason Systems Inc. (PSI-T), Minto Apartment REIT (MI-UN-T), BTB REIT (BTB-UN-T), Cineplex Inc. (CGX-T), Pet Valu Holdings Ltd. (PET-T), Hemlo Mining Corp. (HMMC-T), Westport Fuel Systems Inc. (WPRT-T), Cipher Pharmaceuticals Inc. (CPH-T), Organigram Global Inc. (OGI-T)

Aug. 12: Maple Leaf Foods Inc. (MFI-T), Western Forest Products Inc. (WEF-T), BSR REIT (HOM-U-T), AutoCanada Inc. (ACQ-T), North American Construction Group Ltd. (NOA-T), Ascend Wellness Holdings, Inc. (AAWH-U-CN), Sagicor Financial Company Ltd. (SFC-T), HLS Therapeutics Inc. (HLS-T)

Aug. 13: Total Energy Services Inc. (TOT-T), Pollard Banknote Ltd. (PBL-T), Bird Construction Inc. (BDT-T), Automotive Properties REIT (APR-UN-T), True North Commercial REIT (TNT-UN-T), RFA Financial Inc. (RFA-T), Pro REIT (PRV-UN-T), Calian Group Ltd. (CGY-T), Boston Pizza Royalties Income Fund (BPF-UN-T), Quarterhill Inc. (QTRH-T), Auxly Cannabis Group Inc. (XLY-T)

AMD forecast quarterly revenue above Wall Street estimates on Tuesday, banking on strong demand for its chips from massive data-centre capacity expansions to power AI technologies.

Yet, its shares fell more than 7 per cent in extended trading, suggesting that investors were looking for an even stronger outlook after the stock more than doubled this year spurred on by AI optimism.

“AMD is now in a similar position to Nvidia NVDA-Q and the hyperscalers, where investors are looking for evidence that AI infrastructure investments will continue translating into accelerating returns,” said Jacob Bourne, an analyst at Emarketer.

The Santa Clara, California-based company is regarded as chip giant Nvidia’s closest rival in the market for graphics processing units, as major technology companies and governments worldwide ramp up spending on AI infrastructure.

Adv Micro Devices

518.58+304.42 (142.15%)

Year to date

Dec. 30, 2025

214.16

Aug. 4, 2026

518.58

SOURCE: BARCHART

It has stepped up its AI product launches and moved beyond selling individual chips to offering AI systems that combine processors, networking gear and related hardware, giving customers an integrated AI infrastructure option and allowing it to better rival Nvidia’s rack-scale offerings.

AMD expects third-quarter revenue of about US$13-billion, plus or minus US$300-million, while analysts estimate US$12.52-billion, according to data compiled by LSEG.

Its expects adjusted gross margin to be about 56 per cent, largely in line with estimates.

The forecast suggests that AMD’s multi-billion dollar investments to challenge chip giant Nvidia’s dominance in the market for AI chips are beginning to pay off, with sales of its data-centre processors accelerating sharply.

While GPUs dominate heavy AI training, AMD is also benefiting from growing demand for central processing units, which are used alongside pricey graphics processors in servers. This has helped AMD capture market share from Intel.

AMD’s second-quarter revenue jumped 50 per cent to US$11.54-billion, beating the estimate of US$11.28-billion. Data-centre revenue more than doubled to US$6.72-billion, also exceeding expectations of US$6.48-billion.

More stories below advertisement

Adjusted profit of US$1.66 per share surpassed the estimated US$1.62.

At AMD’s AI event in July, CEO Lisa Su said the company’s second-generation Helios AI servers, featuring the MI455X AI accelerator and “Venice” processor made by TSMC, are in full production and would begin shipping in the coming months.

Supply, however, is constrained by AMD’s reliance on TSMC , the world’s largest contract chipmaker, where tight advanced packaging capacity continues to be a key hurdle.

AMD has also secured major customers and infrastructure agreements in recent months, as it races to expand its AI business.

About two weeks ago, it agreed to sell Anthropic tens of billions of dollars worth of AI servers powered by up to two gigawatts of MI450 chips from early 2027, and invest up to US$5-billion in the IPO-bound Claude maker, contingent on deployment milestones.

The company has also locked in up to 2.5 GW of data centre capacity through a deal with Core Scientific, while gaining warrants to purchase the company’s stock.

AMD’s client and gaming segment, which caters to consumer hardware, saw sales of US$3.84-billion in the second quarter, above estimates of US$3.78-billion.

Analysts have said weakness in the PC market, memory supply constraints and rising memory costs could weigh on demand and margins

Spotify SPOT-N -1.68%decrease forecast third-quarter profit below Wall Street estimates on Tuesday, after the streaming giant reported slowing user growth in major markets of Europe and North America, driving shares nearly 4 per cent lower in premarket trading.

The company has launched AI features such as “Personal Podcasts” and new offerings such as “Reserved” to attract more users and fend off competition from rivals including YouTube and Netflix NFLX-Q +0.33%increase, and AI music startups like Udio and Suno.

Separately on Tuesday, Spotify announced a new agreement with digital music licensing firm Merlin for the Swedish company’s upcoming paid tool for fan-made covers and remixing. It will allows artists on labels under Merlin’s Spotify agreement to participate.

The company said it expects operating income of €670-million (US$770.97-million) in the third quarter, below analysts’ average estimates of €677.8-million, according to data compiled by Visible Alpha.

In the second quarter, its operating income came in at €655-million, beating estimates of €639.2-million, driven by strong revenue growth and lower payroll taxes.

Such taxes, called social charges, are tied to the value of the company’s share price. The company’s shares have fallen about 16 per cent so far this year.

Spotify Technology S.A.

478.17-102.54 (-17.66%)

Year to date

Dec. 30, 2025

580.71

Aug. 4, 2026

478.17

SOURCE: BARCHART

The company’s quarterly revenue rose 14 per cent to €4.78-billion, slightly below LSEG-compiled estimates of €4.80-billion. The revenue forecast of €5-billion for the third quarter was slightly above estimates of €4.93-billion.

Its monthly active users forecast of 788 million was below Visible Alpha estimates of 793.6 million, while its outlook for a 5 million increase in premium subscribers to 305 million was largely in line with estimates.

While total MAUs and premium subscribers grew, North America and Europe’s percentage contribution to total MAUs declined. Europe’s share of premium subscribers has also continued to drop.

Nuclear reactor vendor Westinghouse Electric Co. has confidentially filed for a U.S. initial public offering, its owners revealed on Friday, as demand for new sources of nuclear power attracts renewed interest from investors.

Westinghouse is jointly owned by Brookfield Asset Management Ltd. BEP-UN-T +0.72%increase, through its renewable energy arm, and Saskatoon-based uranium fuel provider Cameco Corp. CCO-T -2.09%decrease

The number of shares to be offered and the price range for the public listing have not yet been set, and the proposed IPO and its timing will depend on market conditions, Cameco said Friday. But the filing allows Westinghouse to prepare for a public listing and share information privately with regulators.

Nuclear energy is making a comeback as demand for electricity surges, especially to serve the rapid development of data centres that train and run artificial intelligence models.

Only eight years ago, Westinghouse was in bankruptcy when Brookfield’s private equity arm bought the company from Toshiba Corp. for US$4.6-billion.

Four years later, Brookfield’s private equity business sold Westinghouse to Cameco and Brookfield Renewable Partners LP, the company’s renewable energy arm, for US$4.5-billion plus US$3-billion in assumed debt. Brookfield kept a 51-per-cent stake, and Cameco owns 49 per cent.

Westinghouse has a decades-long track record in the nuclear sector and a head start on many of its rivals. More than half of the nuclear reactors operating around the world use its technology, according to the company.

If certain milestones are met – including Westinghouse reaching a valuation of US$30-billion – Westinghouse would be compelled to hold an IPO and the U.S. government would be allowed to take an 8-per-cent stake in the company.

The pursuit of such a lofty valuation for Westinghouse is a signal of the sharp reversal in fortunes for the nuclear sector, which is seeking large amounts of capital from investors for its expansion plans.

U.S. President Donald Trump has outlined a plan to jumpstart America’s nuclear industry. And Canada has a strategy to fast-track small modular reactor construction, while also adding more large-scale reactors in the country.

Brookfield Asset Management chief executive Connor Teskey said Friday that the U.S. Department of Energy has committed up to US$17.5-billion in loans to finance the early procurement of equipment for new reactors.

The government financing “is expected to accelerate deployment timelines by up to three years,” and to attract further investment in the nuclear supply chain, Mr. Teskey said.

“Our focus has now shifted from establishing the financing framework for long-lead orders to advancing individual projects,” he said.

Westinghouse’s main offering is its AP1000 reactor. There are two of these reactors operating in the U.S. and four in China, as well as more than a dozen others under construction. But the reactors also have a track record of construction delays and cost overruns, underscoring the inherent risk in such projects.

Enbridge Inc. ENB-T -1.80%decrease expects its gas transmission business to play a growing role amid booming demand across North America, even as some of its customers express unease over ongoing geopolitical uncertainty.

Speaking to analysts Friday as the company reported its second-quarter earnings, executives touted a number of projects underway to expand its capacity to deliver natural gas to customers in the months ahead.

“We’re hearing from customers in all regions of our footprint, including the U.S. Northeast, Midwest and Southeast. All are looking for additional capacity to support unprecedented power and LNG demand,” said president and CEO Greg Ebel.

Enbridge received “significantly more interest” than initially expected for its proposed expansion of the Algonquin Gas Transmission system, dubbed Project Beacon, he said.

The company recently completed an open season – a process used to formally gauge commercial interest – in the U.S. Northeast for the proposed expansion.

“This is really a great example of how we’re seeing … gas demand across all of our footprint in gas transmission right now for all kinds of requirements,” said Matthew Akman, who leads Enbridge’s gas transmission business.

“Some of that is obviously power and data centres and some of it is just catch up in terms of being behind in building infrastructure. Beacon in New England is probably the best example of that, where everyone knows we’ve needed more gas pipeline capacity into there for quite a while.”

Akman called it a “promising” project that could save more than $1 billion per year for utility customers in New England.

“There’s a real recognition we found in the response to the open season of the need for that capacity, for affordability and reliability to reduce emissions from oil burning power as well, and energy costs generally,” he said.

Enbridge also signed an exclusive option to acquire the TTC Connector Pipeline, which will connect Enbridge’s Tres Palacios Gas Storage facility to Freeport LNG and is expected to enter service by the end of the year.

Meanwhile, its Blackcomb pipeline has begun commissioning and the company sanctioned the Bay Runner Twin pipeline to provide Permian natural gas supply to the Rio Grande LNG facility.

Earlier this month, Enbridge announced it had broken ground on a $4-billion natural gas pipeline expansion in British Columbia. The federal government approved the Sunrise Expansion Program in April.

The project aims to add another 300 million cubic feet per day of transportation capacity to the province’s natural gas transmission system.

“We do expect to punch above our weight in gas transmission,” said Akman.

“Some of that could be chunky, of course, because some of the projects … it’ll depend on the customer timing, but very active conversations going on and we’re optimistic that we’re going to be contributing more than our fair share over the next six to 12 months in gas transmission.”

Enbridge reported a second-quarter profit attributable to common shareholders of $1.4-billion, down from $2.18-billion a year earlier. The company said the profit amounted to 64 cents per share for the quarter ended June 30, down from $1 per share in the same quarter last year.

On an adjusted basis, Enbridge earned 63 cents per share in its latest quarter, down from an adjusted profit of 65 cents per share in the second quarter of 2025.

The company said its secured capital backlog stood at $41-billion. It has sanctioned $9-billion of new projects year-to-date and is on track to meet its targeted $10-billion to $20-billion of new project announcements over the 2026 to 2027 time frame.

Ebel said the company is advancing projects amid a backdrop of volatility in energy markets, supply chain disruptions and uncertainty from ongoing geopolitical developments around the world.

“There’s a fair bit of a challenging backdrop for producers, refiners, exporters, and pipelines to fully commit to large-scale projects, but let’s make no mistake, that is coming because the needs are there,” he said.

“Until we get through that volatility piece, people are going to be focused on, ‘Give me customized solutions that I can utilize and I’ll deal with the bigger solutions as we go forward.’”

Alimentation Couche-Tard Inc. ATD-T +1.37%increase is making an US$8.7-billion all-cash takeover play for Polish convenience retailer Zabka Group SA, widening its footprint in Europe with a major push in one of the continent’s fastest-growing economies.

It’s the Canadian company’s biggest acquisition to date, further cementing its position in a key part of the world against global rival 7-Eleven. It’s also one of its most unique acquisitions as it takes control of a dominant, technology-powered retailer already near the top of its game.

“This transaction, candidly, is like none I’ve ever done in the 14 years that I’ve been here,” Couche-Tard chief executive Alex Miller told analysts on a call, referring to his nearly two years as CEO and various senior leadership positions before that.

“Usually it’s us looking what we can bring” to get the most from the company we’re buying, he said. “In this example, we see a lot of things that we think can be brought to us.”

Laval, Que.-based Couche-Tard, which owns the Circle K convenience store chain, said Friday it will launch a voluntary tender offer for Zabka at a price of 32 Polish zloty or about US$8.48 a share. That’s a premium of about 9.4 per cent to its previous closing price.

Owners of about 57 per cent of Zabka stock are backing the deal and have signed agreements to tender their shares, Couche-Tard said. That includes two major shareholders: private equity firms CVC Capital Partners and Partners Group.

No matter how many shareholders tender their shares, Couche-Tard will achieve control of Zabka with an ownership majority. If it succeeds in buying shares representing at least 95 per cent of total voting rights, it plans to squeeze out the remaining stock and move to delist the company from the Warsaw Stock Exchange.

Zabka has been publicly listed in Warsaw for the last two years.Kacper Pempel/Reuters

Launched in 1998 and modelled on 7-Eleven’s corner shops in Japan, Zabka boasts a digital strategy that sees half its revenue flow through its AI-driven mobile shopping application. The company, whose name means “little frog,” runs nearly 13,000 stores across Poland and expanded into Romania in 2024.

Its network is built around compact, modular neighbourhood stores averaging about 700 square feet, and includes a chain of unmanned, autonomous outlets operating 24 hours a day. In addition to regular convenience staples, groceries and ready-to-eat meals, it also offers services like parcel pickup. Half of its customers are younger than 35.

“We are a predictable, growing business,” Zabka’s incoming CEO, Tomasz Blicharski, said, adding its sales have more than doubled over the past five years. The retailer has a commanding presence in Poland, with its biggest competition coming from individual mom and pop shops in various corners of the country, he said.

After a solid trajectory of profit growth over the past two decades, Couche-Tard’s business has come under pressure more recently as consumers cut spending to deal with higher levels of debt as well as inflation. Mr. Miller has proven the company can drive sales from existing stores without takeovers but this deal will put investor focus back on deal-making.

Couche-Tard nabbed a toehold in Europe with the purchase of Norway’s Statoil Fuel & Retail in 2012. It was the company’s first major expansion outside North America, giving it a small presence in Poland in addition to more substantial operations in Scandinavia.

That was followed by the takeover of Ireland’s Topaz Energy Group in 2016 and another deal in Germany and the Benelux countries in 2023, when it bought some 2,200 service stations from French oil company TotalEnergies SE. Along the way, it dropped a US$20-billion bid for European retailer Carrefour in 2021 after it wasn’t able to overcome French government opposition.

Japan’s Seven & i Holdings Co., the parent of 7-Eleven and Couche-Tard’s main rival on the international stage, was also in the hunt for Zabka but said earlier this month it couldn’t strike an agreement that would be in its best interests. The Japanese company wants to build its European presence, which is currently limited to three Nordic countries.

Couche-Tard abandoned its own effort to acquire Seven & i last year in what would have been a blockbuster deal. The Canadian company blasted its Japanese rival for failing to engage in meaningful talks when it announced it was ending its campaign – criticism that has given more weight to the rivalry between the two retailers ever since as they battle for convenience store supremacy.

The Circle K owner likes Zabka for a number of reasons, including the Polish company’s skills at food retailing, extensive distribution network and advanced data and analytics expertise. In short, Mr. Miller said: “Many of the capabilities we believe will define the future of convenience already exist at scale within Zabka.”

Poland’s economic strength doesn’t hurt either. An economy that was once wilting behind the Iron Curtain has transformed over three decades to become one of Europe’s most dynamic, with GDP growth of 3.6 per cent last year.

The transaction is expected to be accretive to the margin on adjusted earnings before interest, taxes, depreciation and amortization right away, and accretive to earnings per share by the second year following deal finalization, Couche-Tard said. According to the company, it can achieve about US$250-million worth of cost-saving opportunities within three years.

Couche-Tard said it intends to fund the transaction through fully committed debt facilities, with J.P. Morgan as lead arranger, and National Bank of Canada Capital Markets and Bank of Nova Scotia acting as joint bookrunners.

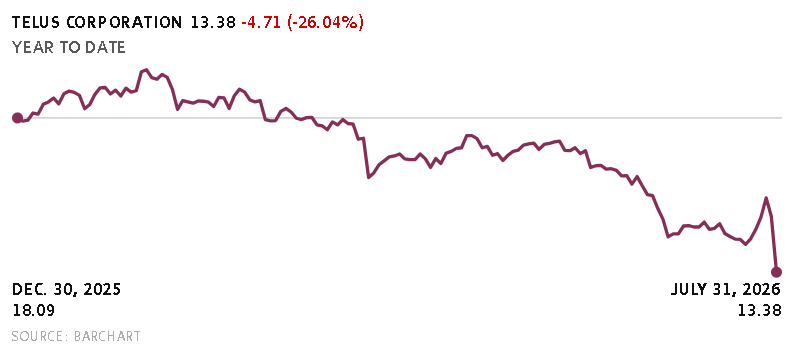

Telus Corp. T-T -11.27%decrease surprised investors Friday with a higher-than-expected 55-per-cent dividend cut while lowering its financial guidance for the year as new chief executive officer Victor Dodig reorients the telecom and technology company in a bid to improve its finances.

The company was widely expected to cut its quarterly dividend, but analysts did not expect it to fall to 18.75 cents per share from 41.84 cents previously.

In a Friday morning note to investors, TD Cowen analyst Vince Valentini said the dividend cut and changes to the financial guidance for the rest of the year “were much worse than expected.”

Telus shares closed down more than 11 per cent to $13.38 on the Toronto Stock Exchange as investors digested the news. Including the latest drop, the shares have fallen almost 52 per cent over the last five years, and almost 26 per cent since the beginning of the year.

“We’re resetting the company for the long term,” Mr. Dodig said in an interview with The Globe on Friday morning.

He acknowledged that the dividend reset was widely anticipated by investors. “We believe that it’s something that was necessary,” he said. “We now have the ability to invest as we grow our company.”

Mr. Dodig said the company’s decision to push back its debt-reduction target by a year to the end of 2028, and lower its financial guidance for 2026, reflect “what we see as the reality,” as the company pursues sales of some of its assets and undertakes a shift in strategy. He said the company has plans to grow revenue faster, simplify its business and redirect spending to the highest areas of growth.

The shifts announced Friday represent an “abbreviated detour as we reset,” Mr. Dodig said. “I’m confident in the way forward.”

Analysts have been raising concerns about Telus’s dividend growth plans since last year, when some called its previous plans to continue increasing its dividend unsustainable. Telus paused dividend growth last November, but has faced ongoing pressure from Bay Street to cut the payout.

The company said Friday the dividend cut is expected to generate about $2.7-billion in cash savings through 2028, which will be used to reduce its long-term debt.

In another early note Friday, Bank of Nova Scotia analyst Maher Yaghi said the dividend cut was needed to restore the company’s financial flexibility.

“The action is the right one, but the size of the guidance reduction shows it was not discretionary,” he said.

The company also reported a net loss of $1.8-billion in the second quarter after recording a $2.1-billion writedown for its Telus Digital unit.

“Some of the growth and spending that we’re seeing from clients going forward has abated somewhat. The goodwill writedown reflects all of that,” Mr. Dodig said.

Telus said it expects revenue for the year to be flat or fall up to 2 per cent, compared to prior guidance in May of a revenue increase of 2 to 4 per cent. The company said its adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) is now expected to fall by 2 to 4 per cent for the year, compared to prior guidance of growth of 2 to 4 per cent. Full-year cash flow is expected to be $1.8-billion this year, down from the prior estimate of $2.45-billion or by about 27 per cent.

Telus also said it plans to reduce its net debt to EBITDA ratio to about three times by the end of 2028 – a debt-reduction target it had previously expected to reach by the end of 2027.

Telus also said Friday it will eliminate the discount it offers investors who use the company’s dividend reinvestment plan (DRIP). The plan allowed shareholders to receive their dividend payments in shares priced below current market value. The change will be effective Oct. 1.

Friday’s announcements mark a turning point for the company’s financial strategy under the new leadership. Darren Entwistle, who retired at the end of July after 25 years at the helm, told The Globe last month that he would have “stayed the course” on the dividend, but acknowledged at the time that his successor, Mr. Dodig, may do otherwise.

On Bay Street, Mr. Dodig became known for turning around the financial performance and share price of The Canadian Imperial Bank of Commerce, which was underperforming its peers when he began as CEO.

Now, he is taking on Telus in the middle of major transformation amid a challenging time for the industry as a whole, as population growth has slowed and wireless prices have been forced down by greater competition.

In addition to a dividend cut, analysts have suggested Telus could divest of a range of non-core assets – from its venture portfolio and surplus real estate to a greater proportion of its health business, which it is currently attempting to monetize.

The company did not share significant details on the progress of those attempts. Mr. Dodig said the company is waiting for the right investor who recognizes an asset’s full value. “We are not out there to sell anything at any price,” he said.

Mr. Dodig told analysts on a call Friday that he will focus on retaining the company’s “crown jewels” and will announce asset sales going forward. “I think you’ll see a much more simplified Telus over time.”

He said Telus Health, Telus Digital and Telus Agriculture are all good businesses, but he will focus “on those we believe should be monetized because they’re better off in the hands of another owner, and do that in a thoughtful manner.”

In a July note to investors, Mr. Valentinicalculated that the company could hypothetically make upward of $8-billion and significantly lower its debt leverage if it were to divest of all its non-core assets, although he said this was an “extreme scenario.” He estimated the company would cut its dividend by 30 per cent.

Mr. Yaghi said in a note earlier in the month that a roughly 50-per-cent dividend cut “would create the financial flexibility needed to begin repairing the balance sheet and reset the equity story on a more sustainable footing.”

It’s not the only dividend cut that Canadian investors have witnessed recently. Last year, rival telecom BCE Inc. BCE-T unchno change slashed its own dividend by more than 50 per cent in order to allocate that cash elsewhere.

Editor’s note: A previous version of the story included incorrect information about the current dividend yield based on today’s share price, which has been removed. The article was further corrected to state that last year BCE cut its dividend by more than 50 per cent, and to correct the spelling of TD Cowen.