Summary

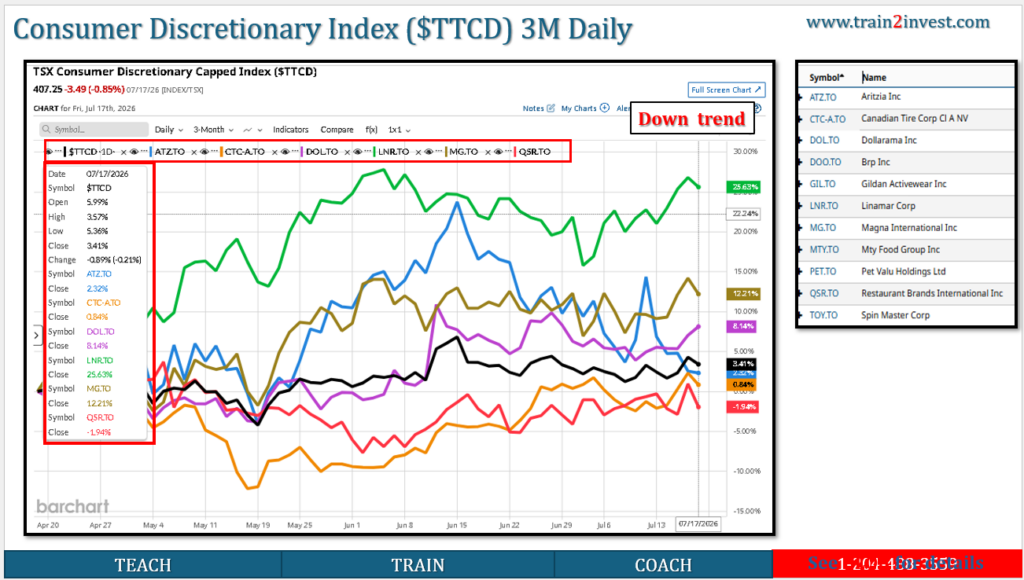

- TTCD—the S&P/TSX Capped Consumer Discretionary Index—was volatile and generally weakened during July 13–17, 2026, after closing at 406.75 on July 10.

- The largest identifiable factor was profit-taking after Aritzia’s 7.4% post-earnings jump on July 10.

- Higher oil prices and bond yields increased inflation and interest-rate concerns, which are usually negative for discretionary spending and sector valuations.

- Broader risk sentiment improved temporarily midweek but deteriorated again Friday as global equity markets sold off.

- I could not verify a complete official set of TTCD closing values for all five sessions; therefore, the causal attribution below is based on confirmed market and constituent evidence rather than a precise daily decomposition.

Five-Day Movement

| Period | TTCD direction | Main explanation |

|---|---|---|

| Monday, July 13 | Downward pressure | Profit-taking after the previous Friday’s strong rally; renewed U.S.–Iran tensions lifted oil prices and bond yields |

| Tuesday, July 14 | Mixed/soft | Inflation uncertainty and a U.S. 10-year Treasury yield around 4.6% pressured rate-sensitive consumer shares |

| Wednesday, July 15 | Rebound | Improved global equity sentiment helped TTCD rise 0.64% to 403.01 |

| Thursday, July 16 | Mixed | Investors balanced strong corporate earnings against persistent oil and interest-rate risks |

| Friday, July 17 | Renewed pressure | Global technology weakness and broader risk reduction spilled into Canadian equities |

The verified TTCD reading for July 15 was 403.01, up 0.64% for that session, but still below its 406.75 July 10 close.

Key Drivers

1. Aritzia’s post-earnings reversal

Aritzia was the most important company-specific influence.

On July 10, Aritzia gained 7.4% after reporting:

- Revenue growth of 43%

- Comparable-sales growth of 35%

- Adjusted EPS of C$0.96, above the approximately C$0.88 consensus

- U.S. revenue growth of 55%

- Increased full-year revenue guidance

These results initially lifted both Aritzia and the consumer-discretionary sector.

However, ATZ subsequently fell from approximately C$158.56 at the July 13 opening to C$143.17 by July 17, a decline of roughly 9.7%. That indicates that much of the initial earnings rally was reversed during the five-day period.

Economic interpretation: the results were strong, but the stock had already risen substantially. Investors likely shifted from evaluating earnings growth to questioning whether the valuation already reflected that growth.

2. Higher oil prices hurt consumer expectations

Renewed U.S.–Iran tensions pushed WTI oil toward or above US$80 per barrel early in the week.

Higher oil prices can weaken TTCD through:

- Higher gasoline and transportation costs

- Reduced disposable household income

- Higher retailer freight and distribution expenses

- Increased inflation expectations

- Reduced probability of interest-rate cuts

This is generally more negative for apparel, automotive, recreational and durable-goods companies than for essential retailers.

3. Higher bond yields pressured valuations

The U.S. 10-year Treasury yield traded around 4.58%–4.62% early in the week.

Higher yields affect consumer-discretionary shares through two channels:

- Economic channel: mortgages, auto loans and credit-card financing remain expensive.

- Valuation channel: future corporate earnings are discounted at a higher rate, reducing justified price-to-earnings multiples.

Higher-valued stocks such as Aritzia and Dollarama can be particularly sensitive to this valuation effect, even when operating results remain strong.

4. Mixed performance among TTCD constituents

The sector did not move uniformly.

| Constituent type | Likely effect |

|---|---|

| Aritzia | Major drag after reversing its post-earnings jump |

| Magna and auto-related companies | Sensitive to borrowing costs, tariffs, vehicle production and economic growth expectations |

| Canadian Tire | Sensitive to discretionary household spending and housing-related purchases |

| Dollarama | More defensive; value-oriented demand likely limited the sector’s decline |

Dollarama continued to benefit from strong demand for lower-priced products. Its latest reported quarterly sales rose to C$1.85 billion, while adjusted earnings exceeded expectations.

Interpretation

TTCD’s five-day movement was not evidence that the Canadian consumer suddenly deteriorated. It was primarily a combination of:

- A reversal in Aritzia after a sharp earnings-related gain

- Higher oil and bond yields

- Profit-taking in richly valued consumer stocks

- Broader global risk-off sentiment

Short term

The sector remains vulnerable to oil prices, bond yields, inflation data and profit-taking in high-multiple stocks.

Longer term

The fundamental picture is mixed:

- Strong companies continue to report healthy revenue growth.

- Value retailers remain supported by cost-conscious consumers.

- Automotive and durable-goods companies remain exposed to financing costs and economic cyclicality.

Actionable Takeaways

- TTCD’s weakness was largely constituent- and valuation-driven, not a uniform collapse in consumer spending.

- Aritzia was likely the most significant marginal driver because its July 10 rally reversed sharply.

- Falling oil prices and bond yields would support a TTCD recovery.

- Continued weakness despite lower yields and stable consumer data would disprove the thesis that the decline was mainly macro- and valuation-related.

Leave a Reply

You must be logged in to post a comment.