Summary

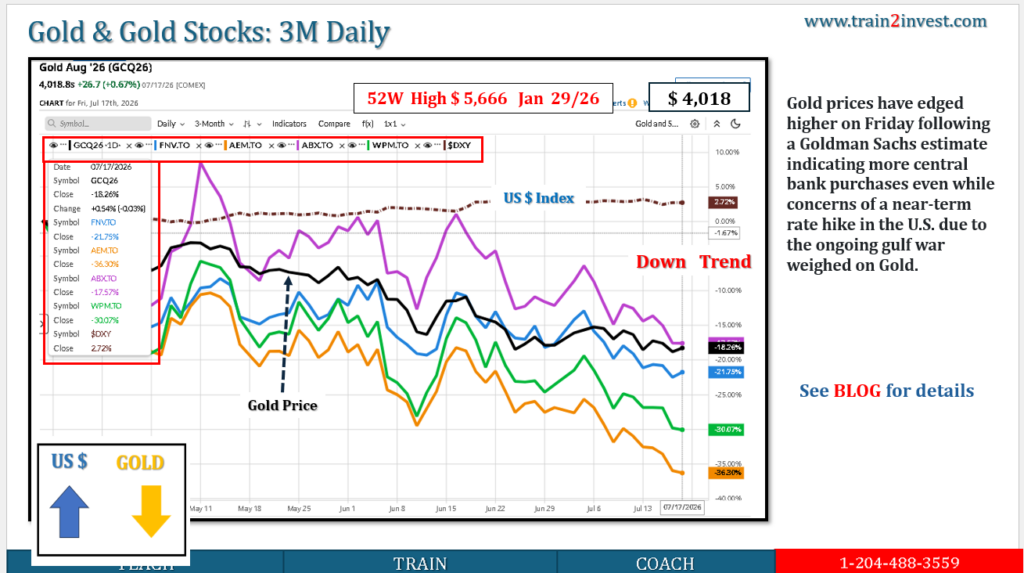

- Gold fell 2.23% over the five trading days ended July 17, 2026, closing at approximately US$4,012.70 per ounce.

- The U.S. Dollar Index was slightly lower, falling from roughly 100.95 to 100.76. Gold therefore declined despite a softer dollar.

- Gold equities fell more than bullion: approximately FNV –3.3%, ABX –5.7%, WPM –6.3% and AEM –7.7%.

- The main pressure came from higher-for-longer interest-rate expectations, rising oil-related inflation concerns, analyst target reductions and profit-taking.

- A stronger Canadian dollar also reduced the CAD value of U.S.-dollar gold revenue, creating an additional headwind for TSX-listed producers.

Five-Day Performance: July 13–17, 2026

| Asset | July 10 | July 17 | Approx. change |

|---|---|---|---|

| Gold futures | US$4,104/oz | US$4,012.70/oz | –2.23% |

| U.S. Dollar Index—DXY | 100.95 | 100.76 | –0.2% |

| Franco-Nevada—FNV.TO | C$290.92 | About C$281.30 | –3.3% |

| Barrick Mining—ABX.TO | C$51.90 | C$48.92 | –5.7% |

| Wheaton Precious Metals—WPM.TO | C$155.83 | C$145.96 | –6.3% |

| Agnico Eagle—AEM.TO | C$207.94 | C$191.93 | –7.7% |

Gold’s weekly result and Friday close are confirmed by commodity-market data. The individual equity figures are based on available historical closing-price records; FNV’s July 17 figure should be treated as approximate because public sources displayed inconsistent intraday and closing data.

1. Gold Price

Why gold declined

Gold started the week near US$4,100 per ounce, weakened materially Wednesday and Thursday, then recovered modestly Friday.

The key decline occurred Thursday, when gold fell about 2%. Escalating U.S.–Iran tensions pushed oil prices higher, which increased concern that energy inflation could keep U.S. interest rates elevated.

Ordinarily, geopolitical conflict supports gold through safe-haven demand. During this week, however, the market focused more heavily on the inflation and interest-rate consequences:Higher oil→higher inflation risk→higher expected interest rates→pressure on gold

Gold pays no interest. When government-bond yields remain high, the opportunity cost of holding gold increases.

U.S. gold futures settled at US$4,051.80 on Wednesday, before falling further Thursday. Gold then gained approximately 0.7% Friday, but the rebound was insufficient to reverse the weekly loss.

Why geopolitical tension did not lift gold

The geopolitical effect was contradictory:

| Effect | Gold implication |

|---|---|

| Safe-haven demand | Positive |

| Higher oil and inflation expectations | Negative |

| Higher expected interest rates | Negative |

| Market risk reduction | Potentially positive |

| Profit-taking after the previous gold rally | Negative |

During this five-day period, the negative interest-rate and positioning effects outweighed safe-haven buying.

2. U.S. Dollar Index—DXY

DXY was broadly stable to slightly lower. It began the period near 100.95, rose to approximately 101.24 Monday, and ended close to 100.76 Friday.

Why the dollar weakened

Softer-than-expected U.S. inflation data reduced expectations for another Federal Reserve rate increase. This lowered the relative interest-rate support available to the dollar.

At the same time, geopolitical tensions created some safe-haven demand for U.S. dollars. The two forces largely offset each other:Lower Fed expectations→weaker dollar

butGeopolitical risk→safe-haven dollar demand

The result was a relatively small weekly DXY movement.

Why gold fell even though DXY weakened

Gold and the U.S. dollar frequently move inversely, but this is not a fixed mathematical relationship.

This week:

- DXY declined only modestly.

- Real and nominal interest-rate concerns remained elevated.

- Oil-related inflation fears increased.

- Investors continued reducing precious-metals exposure.

Therefore, the interest-rate and positioning effects were stronger than the small positive effect of a softer dollar.

3. Franco-Nevada—FNV.TO

FNV declined approximately 3%–4%, less than the major gold producers.

Why FNV held up better

Franco-Nevada is a royalty and streaming company, not a conventional mine operator. It provides capital to mining companies in exchange for a percentage of future production or revenue.

It has limited direct exposure to:

- Mine operating costs

- Labour inflation

- Fuel costs

- Equipment costs

- Mine construction overruns

- Daily mine-management problems

That generally gives FNV lower operating leverage than Barrick or Agnico Eagle.

The stock still fell because lower gold prices reduce the expected value of future royalty revenue. But the royalty model helped limit the decline relative to the producers.

FNV closed around C$290.92 on July 10 and traded near the low-C$280s by the end of the week.

4. Barrick Mining—ABX.TO

ABX declined from C$51.90 to C$48.92, a loss of approximately:51.9048.92−51.90×100=−5.74%

Why Barrick underperformed gold

Barrick has operating leverage to gold:Operating profit per ounce=gold price−production cost

Illustrative example:

| Assumption | Before decline | After decline |

|---|---|---|

| Gold price | US$4,100 | US$4,010 |

| Production cost | US$1,700 | US$1,700 |

| Margin per ounce | US$2,400 | US$2,310 |

| Margin change | — | –3.8% |

A roughly 2.2% gold decline can therefore produce a larger percentage reduction in expected operating profit.

Barrick is also exposed to:

- Political and permitting risk

- Mine-development risk

- Copper-price exposure

- Capital expenditures

- Production guidance

- Cost inflation

Those factors explain why ABX fell substantially more than bullion.

5. Wheaton Precious Metals—WPM.TO

WPM fell from C$155.83 to C$145.96, a decline of approximately:155.83145.96−155.83×100=−6.33%

Why WPM fell more than FNV

Wheaton is also a streaming company, but its revenue has meaningful exposure to silver as well as gold.

Silver declined approximately 6.3% during the week, substantially more than gold.

Therefore, WPM faced two commodity pressures:

- Lower gold prices

- A much sharper silver-price decline

WPM’s higher sensitivity to silver helps explain why it underperformed Franco-Nevada despite both having royalty-and-streaming models.

6. Agnico Eagle—AEM.TO

AEM declined from roughly C$207.94 to C$191.93, a loss of approximately:207.94191.93−207.94×100=−7.70%

Why AEM experienced the largest decline

AEM faced both sector-wide and company-specific pressure.

Gold-price leverage

As a major operating producer, AEM’s earnings and cash-flow expectations are sensitive to changes in gold prices.

Barnat mine concern

Agnico previously reported a rock-mass movement at the Barnat open pit. Although this was not necessarily a new development during the five-day period, it remained an operational uncertainty affecting market sentiment.

Analyst target reductions

Several analysts reduced their AEM price targets during the period or immediately around it, largely reflecting lower commodity-price forecasts and mine-specific assumptions. The ratings were often maintained, but lower targets reinforced short-term selling pressure.

A target reduction does not directly reduce the company’s cash flow. It can, however, influence investor positioning when it confirms that analysts are using lower gold-price assumptions.

Canadian-Dollar Effect

The Canadian dollar gained approximately 1% against the U.S. dollar during the week, reaching about US$0.7135, or C$1.4015 per U.S. dollar.

Gold is priced internationally in U.S. dollars. For a TSX-listed gold company:CAD gold price=USD gold price×USD/CAD exchange rate

If gold falls in U.S. dollars and the Canadian dollar strengthens, the decline in Canadian-dollar gold revenue is amplified.

Illustrative example:

| Variable | Start | End |

|---|---|---|

| Gold | US$4,104 | US$4,013 |

| USD/CAD | 1.4125 | 1.4015 |

| Implied CAD gold | C$5,798 | C$5,624 |

| Approximate decline | –3.0% |

Thus, although U.S.-dollar gold fell about 2.2%, its implied Canadian-dollar value declined closer to 3%.

That created an additional headwind for FNV, ABX, WPM and AEM on the TSX.

Comparative Interpretation

| Asset | Business sensitivity | Five-day result |

|---|---|---|

| Gold bullion | Metal price only | –2.23% |

| FNV | Diversified royalty portfolio; low operating-cost exposure | About –3.3% |

| ABX | Producing mines; cost and geopolitical exposure | –5.7% |

| WPM | Gold and silver streaming exposure | –6.3% |

| AEM | Gold producer plus operational and analyst concerns | –7.7% |

The ordering is economically consistent:bullion→royalty company→operating miners

Operating mining shares normally move more than the underlying commodity because their earnings contain operational and financial leverage.

Scenarios

| Scenario | Gold and equities implication |

|---|---|

| Bull | Lower bond yields, weaker DXY and easing oil inflation allow gold to recover above US$4,100; miners likely outperform bullion |

| Base | Gold consolidates around US$3,950–US$4,100; royalty companies remain more stable than producers |

| Bear | Higher oil, persistent inflation and renewed rate-hike expectations push gold below US$3,950; producers remain the most vulnerable |

What Would Disprove This Interpretation?

The interest-rate thesis would weaken if:

- Bond yields decline materially but gold continues falling.

- DXY weakens significantly without a gold recovery.

- Gold stabilizes while AEM, ABX and WPM continue declining sharply.

- Mining companies report new production, cost or balance-sheet problems.

In those circumstances, company-specific operational and valuation concerns would be more important than the gold price itself.

Actionable Takeaways

- Gold declined despite a modestly weaker DXY because interest-rate and inflation concerns dominated the currency effect.

- Gold equities amplified bullion’s decline because of operating leverage and the stronger Canadian dollar.

- FNV was relatively defensive because it does not operate mines.

- WPM was additionally affected by silver’s sharp decline.

- AEM experienced the greatest pressure, reflecting gold weakness, analyst target cuts and continuing mine-specific uncertainty.

- A sustainable recovery would likely require some combination of lower bond yields, softer oil-driven inflation, a weaker dollar and stabilization above US$4,000 gold.

Leave a Reply

You must be logged in to post a comment.