Consumer prices in Canada rose at a faster-than-expected pace of 2.4 per cent in December, largely due to the base-year effect from last year’s sales tax break, but closely-watched core measures of inflation cooled for the third consecutive month, data showed on Monday.

Analysts polled by Reuters had forecast inflation would hold at the 2.2-per-cent rate recorded in November.

On a monthly basis, the consumer price index declined by 0.2 per cent, Statistics Canada data showed. The monthly decline was less than market expectations of a 0.3-per-cent decrease.

The Canadian central bank’s preferred measures of core inflation, CPI-median and CPI-trim, continued to ease and were the lowest since December, 2024. CPI-median – or the value at the middle of the set of price changes in a month – cooled to 2.5 per cent from 2.8 per cent in November, while CPI-trim – which excludes the most extreme price changes – decreased to 2.7 per cent from 2.9 per cent.

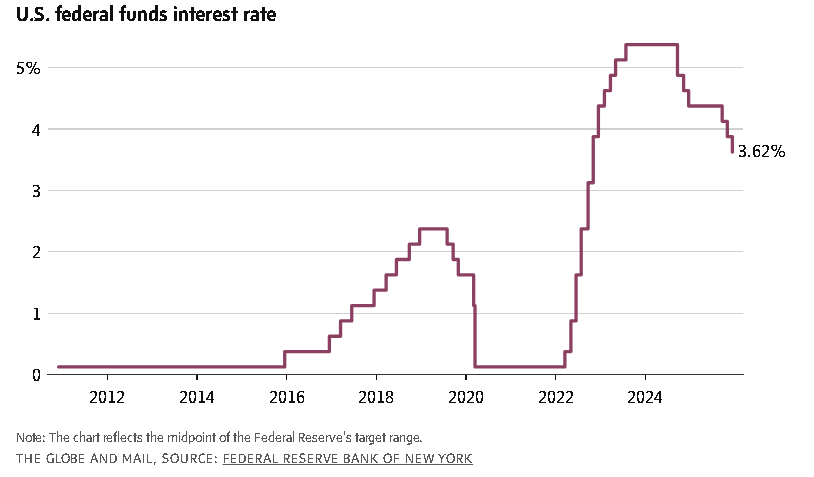

The deceleration in core prices should keep the Bank of Canada at ease after the Bank held its key policy rate steady at 2.25 per cent in December, and said this was about the right level to keep inflation close to its 2-per-cent target. Money markets expect rates to stay on hold in 2026.

The rise in headline inflation in December was driven by a temporary sales tax break on certain food and children’s items authorized by the previous Liberal government headed by Justin Trudeau in the comparative December, 2024, period.

Restaurant prices, one of the segments affected by the tax holiday, were the largest contributor to the acceleration in the annual inflation rate in December, 2025.

Opinion: What cost-of-living crisis? The data tell a different story

Moderating the acceleration in the annual rate was a year-over-year decline in prices for gasoline, which fell 13.8 per cent in December after a 7.8-per-cent decline in November.

Grocery prices, while unchanged month-over-month, rose 5 per cent annually.

Excluding volatile food and energy, inflation rose 2.5 per cent in the month.

Services price inflation rate in December accelerated to 3.3 per cent from 2.8 per cent in November, while goods prices rose by 1.2 per cent after 1.5 per cent in the previous month.

On an annual average basis, prices increased 2.1 per cent last year, following a 2.4 per cent rise in 2024.