- OPEC+ ministers will meet to determine their next oil production policy steps on June 4 in Vienna.

- They face a market rattled by supply volatility, demand uncertainty and a prospective recession, which could throttle transport fuel consumption.

- Public signals have been conflicting following Saudi energy minister Prince Abdulaziz bin Salman’s late-May warning that oil speculators could face further pain ahead.

Author: Consultant

-

OPEC+ prepares for weekend meeting after Saudi warns speculators to ‘watch out’

-

Economic Calendar: June 5 – June 9

Monday June 5

China, Japan and Euro zone services and composite PMI

Germany trade surplus

(9:45 a.m. ET) U.S. S&P Global Services and Composite PMI for May.

(10 a.m. ET) U.S. factory orders for April. The Street expects an increase of 0.8 per cent from March.

(10 a.m. ET) U.S. ISM Services PMI for May.

—

Tuesday June 6

China trade surplus and foreign reserves

Japan household spending

Euro zone retail sales

Germany factory orders

(8:30 a.m. ET) Canadian building permits for April. Estimate is a month-over-month decline of 7.0 per cent.

(10 a.m. ET) Canada’s Ivey PMI for May.

Earnings include: JM Smucker Co.; Stingray Group Inc.

—

Wednesday June 7

Germany industrial production

(8:30 a.m. ET) Canada’s merchandise trade balance for April.

(8:30 a.m. ET) Canadian labour productivity for Q1.

(8:30 a.m. ET) U.S. goods and services trade deficit (and revisions) for April.

(10 a.m. ET) Bank of Canada policy announcement.

(3 p.m. ET) U.S. consumer credit for April.

Earnings include: Brown Forman; Campbell Soup Co.; Dollarama Inc.; Transcontinental Inc.

—

Thursday June 8

Japan and Euro zone GDP

(8:30 a.m. ET) U.S. initial jobless claims for week of June 3. Estimate is 238,000, up 6,000 from the previous week.

(10 a.m. ET) U.S. wholesale inventories for April.

(3:10 p.m. ET) Bank of Canada deputy governor Paul Beaudry presents the Economic Progress Report at the Greater Victoria Chamber of Commerce.

Earnings include: Enghouse Systems Ltd.; Major Drilling Group International; Saputo Inc.

—

Friday June 9

China CPI, PPI, aggregate yuan financing and money supply

(8:30 a.m. ET) Canadian employment for May. Estimate is a month-over-month increase of 30,000 jobs with the unemployment rate rising 0.1 of a percentage point to 5.1 per cent.

(8:30 a.m. ET) Canada’s capacity utilization for Q1.

(10 a.m. ET) U.S. quarterly services survey for Q1.

-

Payrolls rose 339,000 in May, much better than expected in resilient labor market

The U.S. economy continued to crank out jobs in May, with nonfarm payrolls surging more than expected despite multiple headwinds, the Labor Department reported Friday.

Payrolls in the public and private sector increased by 339,000 for the month, better than the 190,000 Dow Jones estimate and marking the 29th straight month of positive job growth.

-

Oil prices rise after U.S. debt deal; all eyes on OPEC meeting

Oil prices rose on Friday after a U.S. debt ceiling deal averted a default in the world’s biggest oil consumer, while attention turned to a meeting of OPEC ministers and their allies at the weekend.

Brent crude futures were up $1.21, or 1.6 per cent, to $75.49 a barrel by 1134 GMT, while U.S. West Texas Intermediate crude (WTI) was up $1.19, or 1.7 per cent, at $71.29. Both contracts were headed for their first weekly loss in three weeks.

Markets were reassured by a bipartisan deal to suspend the limit on the U.S. government’s $31.4-billion debt ceiling, which staved off a sovereign default that would have rocked global financial markets.

Earlier signals of a potential pause in rate hikes by the Federal Reserve also provided support to oil prices, not least by weighing on the U.S. dollar, making oil cheaper for holders of other currencies.

U.S. employment data, watched for pointers for upcoming Fed decisions, is due at 1230 GMT.

Investor attention is also fixed on the June 4 meeting of the Organization of the Petroleum Exporting Countries and allies including Russia, collectively called OPEC+.

OPEC+ in April announced a surprise cut of 1.16 million barrels per day, but the gains from that move have since been retraced and prices are below pre-cut levels.

Sources told Reuters fresh output cuts are unlikely.

On the demand side, the U.S. Institute for Supply Management (ISM) said its manufacturing PMI fell to 46.9 last month, the seventh-straight month that the PMI stayed below 50, indicating a contraction in activity.

Meanwhile, manufacturing data out of China, the world’s second biggest oil consumer, painted a mixed picture.

-

Suncor to cut 1,500 jobs by end of year, employees informed Thursday

Suncor Energy Inc. SU-T will cut 1,500 jobs by the end of the year, as new CEO Rich Kruger forges ahead with his mandate to reduce costs and improve the company’s lagging financial performance.

Employees were given the news Thursday afternoon, in a companywide email from Kruger, Suncor spokeswoman Sneh Seetal said.

She confirmed the job reductions are new, and not part of the company’s previously announced plan to reduce the size of its contractor workforce by 20 per cent in an effort to improve safety and performance at its oil sands sites.

“As a company we needed to make changes that will strengthen our company for the future, and that includes our overall cost structure,” Seetal said by phone, adding the 1,500 job losses will be spread across the organization and will affect both employees and contractors.

The reductions amount to about nine per cent of the 16,558 employees that Calgary-based Suncor had at the end of 2022, according to the company’s annual information form. However, that tally does not include contractors.

Suncor has been under pressure from shareholders — including activist investor Elliott Investment Management — to improve its financial and share price performance, which has lagged its peers.

The company has also been under fire for a recent spate of operational issues and workplace safety incidents, including a string of deaths.

Earlier this spring, Kruger, the former CEO of Imperial Oil Ltd., was enticed out of retirement to take the reins of Suncor and try to turn around the oil sands giant.

In an interview with The Canadian Press last month, Kruger declined to say whether that would involve layoffs or not. But he said he would “look hard and long at the work people do” to ensure that everything that is being done at the company adds value to the bottom line.

Seetal declined to say whether the bulk of the layoffs would take place at head office or in the field. Suncor employs people across the country, in the U.S. and internationally, with its corporate head office located in Calgary.

But she echoed Kruger’s theme of needing to ensure people are doing the work that provides the most value to the organization.

“Work that doesn’t necessarily support regular day-to-day maintenance and operations of assets would be considered (for layoffs), but it’s not necessarily solely office workers,” she said.

Seetal said Suncor is committed to treating its employees with dignity and respect throughout what will inevitably be a difficult process.

She also emphasized the company will not make any cuts that could affect worker safety.

In the first quarter of 2023, Suncor earned a $2.05-billion profit. On an adjusted basis, Suncor’s reported first-quarter profit was $1.81 billion, a 34 per cent decrease year-over-year.

-

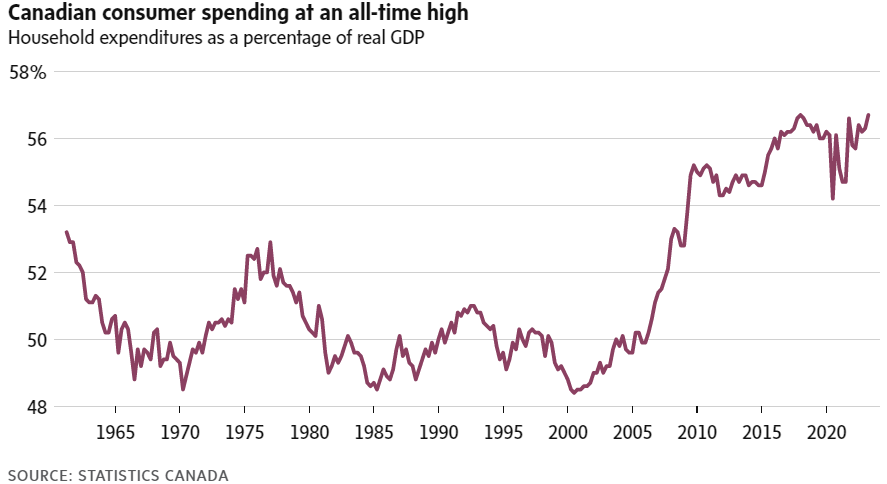

Consumers defy recession forecasts and spend, spend, spend

Can we shop our way out of a recession? Consumers in Canada are giving it their best shot.

The strong first-quarter growth in GDP that caught economists off guard was powered by two sectors, exports and consumer spending, with the latter rising 5.7 per cent on an annualized basis.

That growth was twice as fast as economists expected, and it pushed consumer spending to its highest share of GDP since records began in 1961.

South of the border, resilient consumers have been credited for helping stave off recession. But Canadian shoppers are outspending even their counterparts in the United States, where consumer spending rose 3.8 per cent.

None of this is good news for the Bank of Canada as it tries to cool inflation by discouraging people from buying stuff. Instead Canadians defied rate hikes and recession warnings to fork out for goods such as vehicles and services, including restaurants and hotels, at a frenzied pace.

The boom in services spending will have been particularly troubling to the bank. Governor Tiff Macklem warned in early May “the biggest upside risk to our inflation forecast is that services price inflation could be more persistent than we expect.”

Which is why some economists believe the bank isn’t done tightening. “This is just the latest data point reinforcing the strength of the Canadian economy, particularly the consumer,” wrote Randall Bartlett, an economist with Desjardins. The shopping spree “substantially increases the odds of another rate hike.”

-

With just days to spare, Senate gives final approval to U.S. debt ceiling deal, sending it to Biden

Fending off a U.S. default, the Senate gave final approval late Thursday to a debt ceiling and budget cuts package, grinding into the night to wrap up work on the bipartisan deal and send it to President Joe Biden’s desk to become law before the fast-approaching deadline.

The compromise package negotiated between Biden and House Speaker Kevin McCarthy leaves neither Republicans nor Democrats fully pleased with the outcome. But the result, after weeks of hard-fought budget negotiations, shelves the volatile debt ceiling issue that risked upending the U.S. and global economy until 2025 after the next presidential election.

Approval in the Senate on a bipartisan vote, 63-36, somewhat reflected the overwhelming House tally the day before, relying on centrists in both parties to pull the Biden-McCarthy package to passage – though Democrats led the tally in both chambers.

Senate Majority Leader Chuck Schumer said ahead of voting that the bill’s passage means “America can breathe a sigh of relief.”

Afterward he said, “We’ve saved the country from the scourge that is default.”

Biden said in a statement following passage that senators from both parties “demonstrated once more that America is a nation that pays its bills and meets its obligations – and always will be.”

He said he would sign the bill into law as soon as possible. “No one gets everything they want in a negotiation, but make no mistake: this bipartisan agreement is a big win for our economy and the American people,” the president said. The White House said he would address the nation about the matter at 7 p.m. EDT Friday.

Fast action was vital if Washington hoped to meet next Monday’s deadline, when Treasury has said the U.S. will start running short of cash to pay its bills, risking a devastating default. Raising the nation’s debt limit, now $31.4-trillion, would ensure Treasury could borrow to pay already incurred U.S. debts.

In the end, the debt ceiling showdown was a familiar high-stakes battle in Congress, a fight taken on by McCarthy and powered by a hard-right House Republican majority confronting the Democratic president with a new era of divided government in Washington.

Refusing a once routine vote to allow a the nation’s debt limit to be lifted without concessions, McCarthy brought Biden’s White House to the negotiating table to strike an agreement that forces spending cutbacks aimed at curbing the nation’s deficits.

Overall, the 99-page bill restricts spending for the next two years, suspends the debt ceiling into January 2025 and changes some policies, including imposing new work requirements for older Americans receiving food aid and green-lighting an Appalachian natural gas line that many Democrats oppose.

It bolsters funds for defence and veterans, cuts back new money for Internal Revenue Service agents and rejects Biden’s call to roll back Trump-era tax breaks on corporations and the wealthy to help cover the nation’s deficits. It imposes automatic 1% cuts if Congress fails approve its annual spending bills.

After the House overwhelmingly approved the package late Wednesday, Senate Republican leader Mitch McConnell signalled he too wanted to waste no time ensuring it became law.

Touting its budget cuts, McConnell said Thursday, “The Senate has a chance to make that important progress a reality.”

Having remained largely on the sidelines during much of the Biden-McCarthy negotiations, several senators insisted on debate over their ideas to reshape the package. But making any changes at this stage would almost certainly derail the compromise and none were approved.

Instead, senators dragged through rounds of voting late into the night rejecting the various amendments, but making their preferences clear. Conservative Republican senators wanted to include further cut spending, while Democratic Sen. Tim Kaine of Virginia sought to remove the Mountain Valley Pipeline approval.

The energy pipeline is important to Sen. Joe Manchin, D-W.Va., and he defended the development running through his state, saying the country cannot run without the power of gas, coal, wind and all available energy sources.

But, offering an amendment to strip the pipeline from the package, Kaine argued it would not be fair for Congress to step into a controversial project that he said would also course through his state and scoop up lands in Appalachia that have been in families for generations.

Defense hawks led by Sen. Lindsey Graham of South Carolina complained strongly that military spending, though boosted in the deal, was not enough to keep pace with inflation – particularly as they eye supplemental spending that will be needed this summer to support Ukraine against the war waged by Russian President Vladimir Putin.

“Putin’s invasion is a defining moment of the 21st century,” Graham argued from the Senate floor. “What the House did is wrong.”

They secured an agreement from Schumer, which he read on the floor, stating that the debt ceiling deal “does nothing” to limit the Senate’s ability to approve other emergency supplemental funds for national security, including for Ukraine, or for disaster relief and other issues of national importance.

All told, 46 Democratic senators and 17 Republicans voted for the package; 31 Republicans, four Democrats and one independent who caucuses with the Democrats opposed it.

For weeks negotiators laboured late into the night to strike the deal with the White House, and for days McCarthy had worked to build support among skeptics.

Tensions had run high in the House the night before as hard-right Republicans refused the deal. Ominously, the conservatives warned of possibly trying to oust McCarthy over the issue.

But Biden and McCarthy assembled a bipartisan coalition, with Democrats ensuring passage on a robust 314-117 vote. All told, 71 House Republicans broke with McCarthy to reject the deal.

“We did pretty dang good,” McCarthy, R-Calif., said afterward.

As for discontent from Republicans who said the spending restrictions did not go far enough, McCarthy said it was only a “first step.”

The White House immediately turned its attention to the Senate, its top staff phoning individual senators.

Democrats also had complaints, decrying the new work requirements for older Americans, those 50-54, in the food aid program, the changes to the landmark National Environmental Policy Act and approval of the controversial Mountain Valley Pipeline natural gas project they argue is unhelpful in fighting climate change.

The non-partisan Congressional Budget Office said the spending restrictions in the package would reduce deficits by $1.5-trillion over the decade, a top goal for the Republicans trying to curb the debt load.

In a surprise that complicated Republicans’ support, however, the CBO said their drive to impose work requirements on older Americans receiving food stamps would end up boosting spending by $2.1-billion over the time period. That’s because the final deal exempts veterans and homeless people, expanding the food stamp rolls by 78,000 people monthly, the CBO said.

-

Ottawa backs $3-billion of debt for Trans Mountain pipeline

Ottawa has backstopped $3-billion more in debt for Crown-owned Trans Mountain Corp.’s delayed and overbudget oil pipeline expansion, but the government maintains its guarantees do not amount to public funding.

According to Export Development Canada’s website, Ottawa is guaranteeing $1.75-billion to $2-billion of financing provided by commercial lenders in a transaction finalized at the beginning of May. That followed a guarantee for $750-million to $1-billion of debt in late March. The guarantees are listed within the Canada Account, which includes transactions that are too risky for EDC under its usual course of business because of risks related to deal size, markets, borrowers and financing conditions.

The government approved the loan guarantees after backstopping another $10-billion in financing last year.

In March, Trans Mountain Corp. reported the estimated costs for its expansion had ballooned to $30.9-billion, an increase of more than 300 per cent from the initial $7.4-billion that former owner Kinder Morgan Canada forecast in 2017.

Even before the latest overrun was disclosed, independent analyses, including one a year ago from the Parliamentary Budget Officer, had shown Ottawa would lose money on the project, which it purchased from Kinder Morgan Canada in 2018 for $4.5-billion.

Finance Minister Chrystia Freeland said in 2022 that Ottawa would not plow any more public money into Trans Mountain, which the government has pledged to sell eventually. She said the corporation would secure the funding necessary to complete the project through third-party financing, either in public debt markets or from financial institutions.

The additional government guarantees mean taxpayers are taking on the risk of default. But they are not footing more of the bill to complete the project, Marie-France Faucher, a spokesperson for Ms. Freeland, said in a statement.

“As confirmed in TMC’s first quarter financial statements, TMC continues to secure the necessary third-party financing to complete the project. As part of this process, the Government of Canada has provided a loan guarantee on behalf of the corporation,” Ms. Faucher said. “This is common practice and does not reflect any new public spending. The company is paying a fee to the government for this loan guarantee.”

Trans Mountain is Canada’s only pipeline system for transporting oil to the West Coast. The first phase was completed in 1953, and the line can currently ship 300,000 barrels of oil a day to Burnaby, B.C., from the Edmonton area. Prime Minister Justin Trudeau’s government bought the pipeline after Kinder Morgan Canada shelved plans for the expansion in the face of stiff opposition and court challenges from environmentalists and some Indigenous groups.

The expansion project, which is due to be completed early next year, will nearly triple the pipeline’s throughput to 890,000 barrels a day. Eighty per cent of the capacity of the expanded pipeline has been allocated to 11 Canadian and international producers and refiners, under 15- and 20-year transport contracts.

Energy companies have said for years they are looking to the expansion of the pipeline to boost the value of their oil production, which has at times suffered deep price discounts compared with other international crude types because of tight export capacity and reliance on the United States as the Canadian oil patch’s only sizable customer.

Years of delays and cost increases have raised concerns about the project’s long-term financial viability. Ms. Faucher said the government plans to start the process of divesting itself from the pipeline “in due course.”

“As assessed by BMO Capital Markets and TD Securities, the project remains commercially viable, and there is strong interest from investors in high quality, operational infrastructure assets like the Trans Mountain Expansion Project,” she said.

Several Indigenous groups have expressed interest in buying the pipeline, including Calgary-based Project Reconciliation; Nesika Services, a group that describes itself as an Indigenous-led not-for-profit; and Chinook Pathways, a partnership between Western Indigenous Pipeline Group and Pembina Pipeline Corp. But some would-be bidders have expressed fatigue after waiting years for a formal process to begin.

-

Private payrolls rose by 278,000 in May, well ahead of expectations, ADP says

- Private sector employment increased by a seasonally adjusted 278,000 for the month, ahead of the Dow Jones estimate for 180,000, ADP reported.

- The ADP report noted that the distribution of job grains was “fragmented” as increases were concentrated in just a few industries.

- Salary growth is still strong showing signs of decelerating, the payroll processing firm said.

Private payrolls rose by 278,000 in May, well ahead of expectations, ADP says (cnbc.com)