- The Federal Reserve is expected to increase interest rates by a quarter point Wednesday, even with concerns about stress in the banking system.

- The central bank is also expected to release projections about the economy and the path of rate hikes, though some economists say it may have a difficult time making those forecasts due to uncertainty.

- Investors are also looking for assurances from the Fed that the issues with regional banks will be contained.

Author: Consultant

-

The Fed is likely to hike rates by a quarter point but it must also reassure it can contain a banking crisis

-

Nothing comes for free: What China hopes to gain in return for helping Russia

The visit by China’s president, Xi Jinping, to Moscow this week comes at a time when Russia, and President Vladimir Putin, look vulnerable. Analysts are questioning what price China could extract from Russia in return for supporting it.China has a strategic interest in Putin’s war on Ukraine being victorious but it doesn’t want to risk Western sanctions on its own economy.

One of the big questions to emerge from the visit by China’s president, Xi Jinping, to Moscow this week is the degree to which it could help a geopolitically isolated Russia both on the battlefield, and off it — and what price it could extract for doing so.

It’s no secret that Russia would like China to help it out while it flounders in an economic and military quagmire brought about by its invasion of Ukraine a year ago. International sanctions have restricted or cut off Moscow’s access to numerous Western markets, while the ongoing war in Ukraine shows all the signs of turning into a bloody stalemate that could, if it loses, cause seismic political change in Moscow.

Against that backdrop, the current meeting between Xi and President Vladimir Putin in Moscow, into its second day on Tuesday, will see the leaders discuss the war in Ukraine and China’s peace plan, the Russian leader said as he welcomed his Chinese counterpart Monday.

Unofficially, however, analysts say the presidents are also likely to discuss ways for China to assist Russia without it risking being hit with Western sanctions itself.

Russia reportedly asked Beijing for military and economic assistance early on in its invasion to help it wage its war against Ukraine, although both governments publicly denied it. The eye of suspicion is still being cast on Beijing, despite its continuing denials that it could help Moscow with lethal weapons.

For many close watchers of Russia and China’s deepening relationship over the past decade, the big question then is this: What could China want in return for helping Moscow?

What does China want?

When geopolitical analysts discuss China, one aspect of Beijing’s foreign policy is agreed on fully: China never acts purely out of altruism and there is always a price (or perceived prize for Beijing) for its support or intervention.

https://www.cnbc.com/2023/03/21/what-does-china-want-from-russia-if-it-helps-it-with-ukraine.html

-

March 21: Crude Oil Futures Rise For 2nd Straight Day, Settle Sharply Higher

Crude oil prices climbed higher on Tuesday, gaining for a second straight session, amid improving risk sentiment thanks to the coordinated efforts by major central banks to rescue troubled U.S. and European banks.

The dollar was quite subdued today with investors looking ahead to the Federal Reserve’s monetary policy announcement on Wednesday.

West Texas Intermediate Crude oil futures for April ended higher by $1.69 or about 2.5% at $69.33 a barrel.

Brent crude futures were up $1.37 or 1.86% at $75.16 a barrel a little while ago.

Traders look ahead to weekly oil reports from the American Petroleum Institute (API) and U.S. Energy Information Administration (EIA). API’s report is due later today, while EIA is scheduled to release its inventory data at 10:30 AM ET on Wednesday.

A meeting of key ministers from OPEC+, which includes OPEC members plus Russia and other allies, is scheduled for April 3.

-

March 21: TSX Ends On Strong Note

The Canadian market ended on a strong note on Tuesday, led by gains in healthcare, energy, technology and financials shares.

The undertone was quite positive right through the day’s session amid easing concerns about banking turmoil thanks to the coordinated steps taken by governments and the central banks to rescue troubled U.S. and European banks.

Investors looked ahead to the Federal Reserve’s monetary policy. The Fed is widely expected to raise interest rate by 25 basis points.

The benchmark S&P/TSX Composite Index ended with a gain of 135.49 points or 0.69% at 19,654.92 after scaling a high of 19,734.68.

The annual inflation rate in Canada fell to 5.2% in February of 2023, the least since January 2022, slowing from the 5.9% in the previous month amid significant base-year effects.

Core consumer prices in Canada increased 0.5% from a month earlier in February of 2023, following a 0.3% rise in January.

Hut 8 Mining Corp (HUT.TO) soared more than 9% on huge volumes.

Crescent Point Energy (CPG.TO) surged nearly 7.5%. Baytex Energy (BTE.TO), Shopify Inc (SHOP.TO), Cenovus Energy (CVE.TO), Athabasca Oil Corporation (ATH.TO) and Canadian Natural Resources (CNQ.TO) gained 3 to 5%.

Suncor Energy (SU.TO), Canadian Imperial Bank of Commerce (CM.TO), Lundin Mining Corporation (LUN.TO), Bank of Nova Scotia (BNS.TO), Algonquin Power & Utilities Corp (AQN.TO), TC Energy Corporation (TRP.TO), Manulife Financial Corporation (MFC.TO) and National Bank of Canada (NA.TO) gained 1 to 2.8%.

Precision Drilling Corporation (PD.TO) rallied 8.7%. Canadian Utilities (CU.X.TO) and Canadian Tire Corporation (CTC.TO) surged 6.6% and 6.2%, respectively.

Fairfax Financial Holdings (FFH.TO), Nuvei Corp (NVEI.TO), Bombardier Inc (BBD.A.TO), goeasy (GSY.TO), Kinaxis Inc (KXS.TO), Cargojet (CJT.TO), Nutrien (NTR.TO) and BRP Inc (DOO.TO) also posted strong gains.

Fortis Inc (FTS.TO), Franco-Nevada Corporation (FNV.TO), Agnico Eagle Mines (AEM.TO), Teck Resources (TECK.A.TO), Loblaw Companies (L.TO) and Stantec (STN.TO) ended sharply lower.

-

Oil prices fall to lowest since 2021 on banking fears

Oil prices dropped to their lowest in 15 months on Monday, driven down by concern that risks in the global banking sector and a potential increase to U.S. interest rates could spark a recession that would sap fuel demand.

In volatile trading, Brent crude futures for May fell 87 cents, or 1.2 per cent, to $72.10 a barrel by 1211 GMT. The U.S. West Texas Intermediate crude contract for April was down 85 cents, or 1.3 per cent, at $65.89 before its expiry on Tuesday.

The more actively traded May futures were down 1.2 per cent at $66.11 a barrel.

Brent and WTI earlier fell by about $3, hitting lows last registered in December 2021, with WTI sinking below $65 a barrel. Both benchmarks shed more than 10 per cent of their value last week as the banking crisis deepened.

The slide in oil comes despite the historic deal for UBS, Switzerland’s largest bank, to buy Credit Suisse in an attempt to rescue the country’s second-biggest bank.

However, banking stocks and bonds continued to plunge on Monday in a sign that investor confidence remains fragile.

After the deal was announced, The U.S. Federal Reserve, European Central Bank and other major central banks pledged to enhance market liquidity and support other banks.

“The market focus is on current banking sector volatility and the potential for further rate hikes by the Fed,” said Baden Moore, National Australia Bank’s head of commodity research.

The U.S. Federal Reserve is expected to raise interest rates by 25 basis points on March 22 despite the recent banking sector turmoil, according to most of the economists polled by Reuters.

However, some executives are calling on the central bank to pause its monetary policy tightening for now but be ready to resume raising rates later.

“Volatility is likely to linger this week, with broader financial market concerns likely to remain at the forefront,” ING Bank analysts said in a note, adding that the looming Fed decision increases week’s Fed meeting adds to uncertainty in markets.

Further out, a ministerial committee of OPEC and producer allies including Russia, together known as OPEC+, is set for April 3. The group agreed in October to cut oil production targets by 2 million barrels per day until the end of 2023.

-

North Korea’s Kim Jong Un calls for nuclear attack preparedness on US, South Korea

North Korean leader Kim Jong Un has called on his country to be ready to launch a nuclear attack to deter war as he accused the U.S. and South Korea of carrying out military drills with American nuclear assets, according to state media.

Kim’s remarks, carried on state media KCNA, came after the Hermit Kingdom launched a short-range ballistic missile toward the sea on Sunday. The missile flew across the country and landed in the sea off its east coast, according to South Korean and Japanese assessments – which reported that the missile traveled a distance of about 500 miles.

FILE: North Korean leader Kim Jong Un attends the 7th enlarged plenary meeting of the 8th Central Committee of the Workers’ Party of Korea (WPK) in Pyongyang, North Korea, March 1, 2023 in this photo released by North Korea’s Korean Central News Agency (KCNA). (KCNA via REUTERS)

Kim, who oversaw the test, said the exercises improved the military’s actual war capability and highlighted the need to ensure its readiness posture for any “immediate and overwhelming nuclear counterattack” through such drills.

KCNA quoted Kim as saying the North “urgently” needed to bolster up its nuclear war deterrence exponentially as the enemies “are getting ever more pronounced in their moves for aggression against” his country.

“The nuclear force of the DPRK will strongly deter, control and manage the enemy’s reckless moves and provocations with its high war readiness, and carry out its important mission without hesitation in case of any unwanted situation,” Kim was quoted as saying.

KCNA photos showed Kim attending the test with his young daughter as flames roared from the soaring missile before it hit the target.

-

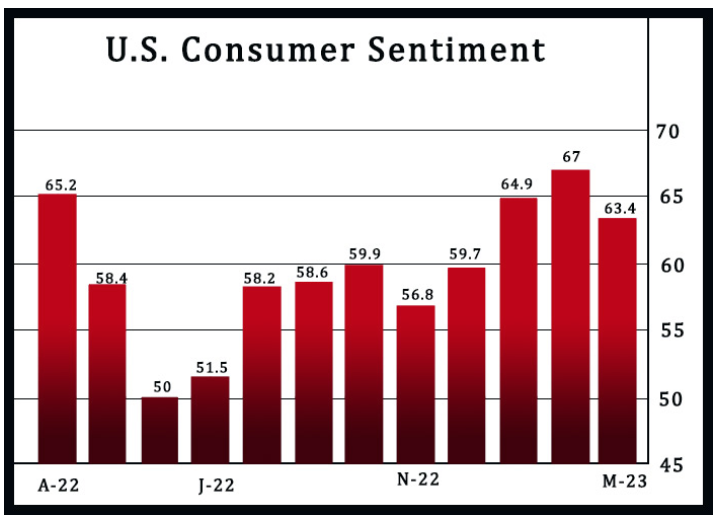

U.S. Consumer Sentiment Unexpectedly Drops In March, Inflation Expectations Dip

Consumer sentiment in the U.S. fell for the first time in four months in March, according to a preliminary report released by the University of Michigan on Friday.

The report said the consumer sentiment index slid to 63.4 in March from 67.0 in February. Economists had expected the index to be unchanged.

Surveys of Consumers Director Joanne Hsu noted the decrease was already fully realized prior to the failure of Silicon Valley Bank.

“Sentiment declines were concentrated among lower-income, less-educated, and younger consumers, as well as consumers with the top tercile of stock holdings,” Hsu said.

She added, “Overall, all components of the index worsened relatively evenly, primarily on the basis of persistently high prices, creating downward momentum for sentiment leading into the financial turmoil that began last week.”

The current economic conditions index fell to 66.4 in March from 70.7 in February, while the index of consumer expectations dropped to 61.5 from 64.7.

Meanwhile, the report showed decreases in both near-term and long-term inflation expectations, with year-ahead inflation expectations falling to the lowest level since April 2021.

One-year inflation expectations slipped to 3.8 percent in March from 4.1 percent in February, while five-year inflation expectations edged down to 2.8 percent from 2.9 percent.

-

Jammu and Kashmir: India’s first big lithium find boosts electric car hopes

India has announced its first significant discovery of reserves of lithium, a rare element crucial for manufacturing electric vehicles.

The government said on Thursday that 5.9m tonnes of the element had been discovered in Jammu and Kashmir.

So far, India has depended on Australia and Argentina for lithium imports.

Lithium is a key component in rechargeable batteries that power numerous gadgets like smartphones and laptops, as well as electric cars.

Experts say that the discovery could aid India’s push to increase the number of private electric cars by 30% by 2030, as part of efforts to cut carbon emissions to tackle global warming.

The Geological Survey of India found the lithium reserves in the Salal-Haimana area of Reasi district in Jammu and Kashmir, India’s Ministry of Mines said.

In 2021, much smaller deposits of lithium were found in the southern state of Karnataka.

Earlier, the government had said that it was looking to improve its supply of rare metals needed to boost new technologies and was looking for sources in India and abroad.

Vivek Bharadwaj, Ministry of Mines secretary, told Mint newspaper that India had been “re-orienting its exploration measures” to meet this goal.

Around the world the demand for rare metals, including lithium, has increased as countries look to adopt greener solutions to slow down climate change.

In 2023, China signed a $1bn (£807m) deal to develop Bolivia’s vast lithium reserves, which are estimated at 21m tonnes and the largest in the world.

According to the World Bank, mining of crucial minerals will need to increase by 500% to meet global climate targets by 2050.

However, experts say that the process of mining lithium is not environment-friendly.

Lithium is extracted from hard rocks and underground brine reservoirs largely found in Australia, Chile and Argentina.

After it is mined, it is roasted using fossil fuels, searing the landscape and leaving behind scars. The extraction process also requires a lot of water and releases large amounts of carbon dioxide into the atmosphere.

To extract it from underground reservoirs, many of which are found in water-scarce Argentina – a large amount of water is used, leading to protests from indigenous communities, who say that such activity is exhausting natural resources and leading to acute water shortages.

-

UBS reaches agreement to buy Credit Suisse after upping offer: report

The Swiss government is reportedly set to announce a deal Sunday that will allow UBS, the largest bank in Switzerland, to buy its beleaguered rival, Credit Suisse, for $2 billion, according to the Financial Times.

https://www.foxbusiness.com/economy/ubs-reaches-agreement-to-buy-credit-suisse-after-upping-offer-report

The announcement comes amid mounting concerns over the potential collapse of Credit Suisse creating a contagion in the banking sector. Credit Suisse saw its stock price plunge and deposit outflows continue last week despite receiving a $54 billion financial lifeline from the Swiss National Bank to bolster its liquidity. The deal was first reported by the Financial Times.

Regulators faced a sense of urgency to push the deal through on Sunday before markets opened Monday as the specter of Credit Suisse potentially failing next week loomed over the negotiations. Credit Suisse, which has been in business for 167 years, is one of 30 globally systemically important banks, which heightened worries about how global financial markets would react to its implosion.