Summary

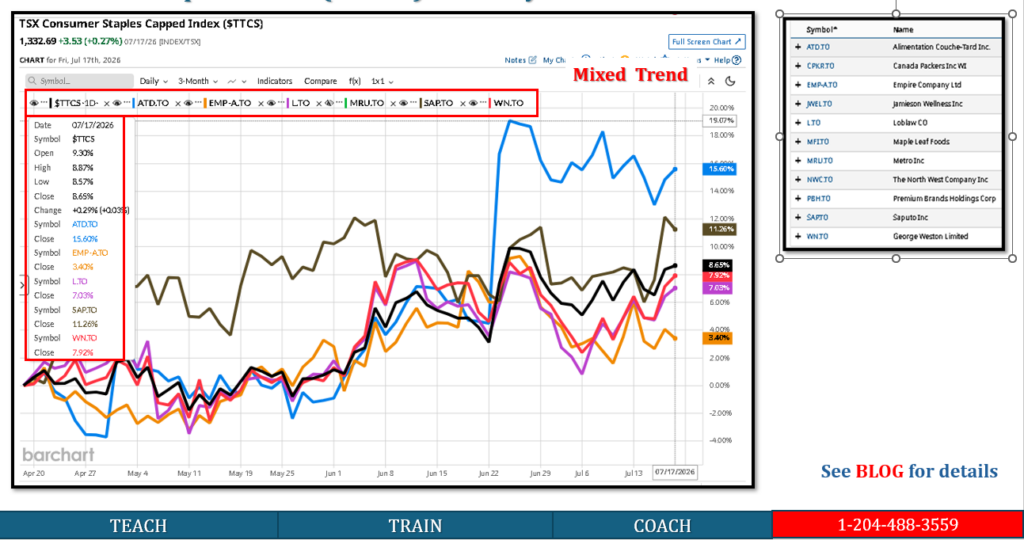

- George Weston (WN.TO) gained 2.86% over July 13–17, 2026, rising from C$100.98 to C$103.87.

- The stock advanced Monday, declined Tuesday and was nearly flat Wednesday, before rebounding strongly Thursday and Friday.

- No major George Weston-specific announcement was identified during the five sessions.

- The strongest driver was positive movement in Loblaw, George Weston’s largest operating investment, combined with defensive consumer-staples demand.

- Share repurchases and solid underlying results provided background support, but did not create a specific daily catalyst.

Five-Day Price Movement

| Date | Close | Daily change | Main interpretation |

|---|---|---|---|

| July 10 | C$100.98 | — | Starting reference |

| July 13 | C$102.44 | +1.45% | Defensive-sector buying |

| July 14 | C$100.95 | –1.45% | Profit-taking |

| July 15 | C$100.88 | –0.07% | Consolidation |

| July 16 | C$103.12 | +2.22% | Strong Loblaw/staples rebound |

| July 17 | C$103.87 | +0.73% | Positive momentum continued |

Overall return

100.98103.87−100.98×100=2.86%

WN.TO therefore gained C$2.89 per share, or approximately 2.9%, over the period.

Key Drivers

1. Loblaw was the principal operating driver

George Weston is primarily a holding company whose value is heavily influenced by its ownership of:

- Loblaw Companies

- Choice Properties REIT

- Corporate cash, debt and other investments

Loblaw gained approximately 2.0% over the same five-day period, supported by defensive demand for grocery, pharmacy and discount-retail exposure.

Because Loblaw is George Weston’s largest underlying asset, strength in L.TO generally increases the market value attributed to WN.TO.

This relationship is not necessarily one-for-one because George Weston also has:

- Holding-company debt

- Corporate expenses

- Choice Properties exposure

- Tax considerations

- A holding-company discount

2. Defensive consumer-staples rotation

The broader consumer-staples sector strengthened during the latter part of the week.

Investors generally view George Weston’s underlying businesses as defensive because they are concentrated in:

- Food retail

- Pharmacy and healthcare products

- Discount grocery

- Essential consumer goods

- Grocery-anchored real estate

These businesses are less dependent on discretionary household spending than automotive, apparel or durable-goods companies.

This likely contributed to Monday’s increase and the strong Thursday–Friday recovery.

3. Tuesday–Wednesday decline was likely consolidation

WN.TO fell from C$102.44 Monday to C$100.88 Wednesday, a decline of approximately:102.44100.88−102.44×100=−1.52%

No material negative George Weston announcement was identified during those sessions.

The pullback was most consistent with:

- Profit-taking after recent gains

- Movement in Loblaw and other staples shares

- Normal short-term consolidation

- Valuation caution as WN approached recent highs

This is an inference, not a directly confirmed cause.

4. Strong Thursday rebound followed Loblaw’s pattern

WN.TO gained 2.22% Thursday, its strongest session of the week.

Loblaw also rose strongly that day. This supports the conclusion that the movement was linked mainly to the value of George Weston’s underlying holdings rather than a separate Weston-specific event.

The share-price pattern was therefore:Loblaw/staples movement→change in WN holding value→WN share-price response

5. Share repurchases supported per-share value

George Weston purchased and cancelled 2.9 million shares for C$275 million during the first quarter of 2026. The lower share count contributed approximately C$0.03 per share to adjusted EPS growth.

Buybacks can support the stock by:

- Reducing shares outstanding

- Increasing earnings per share

- Increasing each remaining shareholder’s proportional interest

- Narrowing the holding-company valuation discount

However, there was no new repurchase announcement during the five-day period itself.

Fundamental Background

George Weston’s first-quarter results showed:

| Metric | Q1 2026 |

|---|---|

| Adjusted net earnings available to common shareholders | C$333 million |

| Year-over-year growth | +1.8% |

| Adjusted diluted EPS | C$0.87 |

| Adjusted EPS growth | +4.8% |

| Shares repurchased and cancelled | 2.9 million |

| Repurchase value | C$275 million |

Loblaw generated positive sales momentum, while Choice Properties reported stable occupancy and strong leasing spreads.

Facts Versus Inference

| Finding | Assessment |

|---|---|

| WN.TO gained 2.86% | Verified |

| Thursday was the strongest session | Verified |

| Loblaw rose over the same period | Verified |

| George Weston released major news during the week | No major release identified |

| Loblaw strength drove much of WN’s gain | Strong evidence-based inference |

| Tuesday–Wednesday weakness was profit-taking | Reasonable inference |

| George Weston’s intrinsic value rose exactly 2.86% | Not established |

Scenarios

| Scenario | Near-term implication |

|---|---|

| Bull | Continued Loblaw strength, stable Choice Properties performance and buybacks could move WN toward its 52-week high near C$106 |

| Base | WN consolidates between approximately C$100 and C$106 while awaiting earnings |

| Bear | Weak Loblaw results, REIT pressure or a wider holding-company discount could push WN below C$100 |

What Would Disprove This Explanation?

The Loblaw-driven interpretation would weaken if:

- WN declines while Loblaw continues rising

- Choice Properties weakens materially

- George Weston increases corporate debt substantially

- The holding-company discount widens

- George Weston reports weaker standalone cash flow or higher corporate expenses

Actionable Takeaways

WN.TO’s five-day pattern was:early gain→two-day pullback→strong Thursday–Friday rebound

The stock finished approximately 2.9% higher. The most credible explanation is strength in Loblaw and defensive consumer-staples positioning, rather than a new George Weston-specific event.