The S&P 500 ticked higher to a new record to began December trading as investors looked for stocks to add to big November gains.

The S&P 500 was higher by 0.2%, touching a new intraday record. The Nasdaq Composite added 1%, also reaching a new intraday high. The Dow Jones Industrial Average was down 0.3% after briefly trading above 45,000. The blue-chip index had previously touched the milestone briefly a few times last week.

Intel jumped 3% after CEO Pat Gelsinger retired after four years of underperformance at the chipmaker. Shares of Tesla also gained 3% following an upgrade to buy from neutral at Roth MKM, with the firm citing as a catalyst Musk’s close relationship with President-elect Donald Trump. AI server maker Super Micro Computersurged 19% after a special committee found “no evidence of misconduct” and that the firm’s financial statements were “materially accurate.”

November marked the best month of 2024 for both the Dow and S&P 500, with the two gaining 7.5% and 5.7% respectively for the period. Most of the gains came in a postelection rally after President-elect Donald Trump emerged as the winner. Both of the indexes notched closing highs in Friday’s shortened trading session.

Canadian manufacturing activity increased at the fastest pace in 21 months in November as the Bank of Canada’s interest-rate cutting campaign boosted domestic demand and despite port strikes that worsened delivery delays, data showed on Monday.

The S&P Global Canada Manufacturing Purchasing Managers’ Index (PMI) rose to 52.0 in November from 51.1 in October, its highest level since February 2023 and the third straight month above the 50.0 no-change mark.

A reading above 50 indicates expansion in the sector.

“Output and new orders both rose at stronger rates when compared to October, with firms noting an uplift in domestic market activity, linked in part to recent reductions in interest rates,” Paul Smith, economics director at S&P Global Market Intelligence, said in a statement.

“In contrast, subdued global demand continued to weigh on overall sales.”

The Canadian central bank has cut its benchmark interest rate by one and a quarter percentage points since June, lowering the rate to 3.75 per cent. Investors expect further easing in a policy decision on Dec. 11.

The output index rose to 53.1 from 52.2 in October, while the new orders measure was at 52.7, up from 50.5. New export orders declined for the 15th successive month.

Canada sends about 75 per cent of its exports to the United States, so its economy could be harmed if U.S. President-elect Donald Trump follows through on a pledge to impose a 25 per cent tariff on imports from Canada and Mexico.

Average lead times for the delivery of inputs lengthened for the fifth straight month and by the most since August, which firms put down to rail delays and port stoppages.

Earlier this month, Canada moved to end labor disputes at the country’s biggest ports, including Vancouver and Montreal, citing economic damage.

A stronger U.S. dollar – the greenback notched a 4-1/2-year high against its Canadian counterpart last Tuesday – helped raise the price of imported goods, firms said.

Input cost inflation accelerated to its highest level since April 2023. The output price index also rose but remained below its recent peak in August.

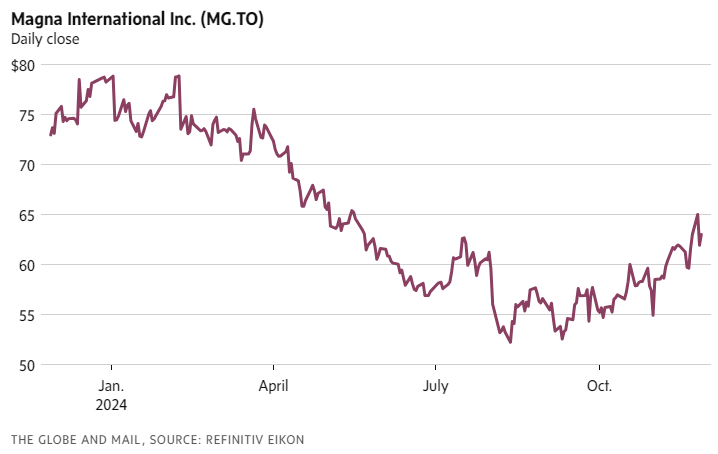

Add one more headwind facing Magna International Inc. MG-T +1.35%increase: When U.S. president-elect Donald Trump announced this week that he will impose a 25-per-cent tariff on all products imported from Canada and Mexico, the Canadian-based auto-parts manufacturer looked vulnerable to the tough talk.

So why has the share price remained roughly unchanged, holding onto an impressive gain of about 20 per cent over the past 11 weeks? Perhaps markets are telling pundits to relax.

The prospect of tariffs disrupting Magna’s complex global operations – which include 342 facilities in 28 countries, serving 58 vehicle manufacturers – is just one of several issues that have weighed on the company over the past few years.

It took a US$376-million charge in 2022 after shuttering its six production facilities in Russia.

Sales of electric vehicles, a segment in which Magna has a substantial investment with parts such as battery enclosures, have not been living up to expectations. More broadly, light-vehicle production – Magna’s bread and butter – is in a global slump, falling 4 per cent in the third quarter year-over-year.

Magna’s share price has been struggling with these challenges. From a high above $125 in mid-2021, the stock fell by as much as 58 per cent by August, 2024.

Since then, Mr. Trump has won the U.S. presidential election, and his harsh rhetoric on tariffs has edged toward actual policy, raising additional uncertainties for the interconnected North American automotive sector, which has virtually ignored borders for decades.

“It’s important to consider that, for close to 30 years, the sourcing of light vehicles and their downstream components – the whole value chain – has not viewed Canada and Mexico as separate countries,” said Mike Wall, the executive director of automotive analysis at S&P Global Mobility, in an interview.

Curiously, though, Magna’s share price has rebounded from its August lows, suggesting that investors aren’t too worried.

The stock’s cheap valuation, based on price-to-earnings and price-to-book ratios, implies that a lot of bad news has been priced in.

Interest rates may be working in Magna’s favour as well. As central banks cut their key rates in response to tamed inflation, lower borrowing costs should help stimulate vehicle sales.

A third factor: Magna has been adept at navigating the difficult environment for vehicle production. With its most recent quarterly results, released earlier this month, the company forecast relatively stable profit margins and announced it would buy back its own shares and pay down debt. The share price bounced 6.5 per cent on the day the quarterly results were released.

That was before Mr. Trump made his tariff announcement. Since then, Magna hasn’t commented publicly on the potential impact on its global operations and did not immediately respond to The Globe and Mail’s request for comment.

But at the Barclays Global Automotive and Mobility Tech Conference on Nov. 21, a top Magna executive did address the theoretical issue of tariffs – and didn’t sound particularly rattled.

Patrick McCann, Magna’s chief financial officer, wondered whether tariffs would hit vehicles or parts. In any case, if Mr. Trump wants tariffs to encourage production to move back to the U.S., he mused, it would be nearly impossible to achieve such a complex shift over a four-year period.

“Those are all the things that are up in the air, and I don’t have a crystal ball,” Mr. McCann said.

For now, investors appear to be okay with that. Magna’s share price, though down sharply over the past few years, is hovering just below a six-month high. And major equity indexes, including the S&P 500 and the S&P/TSX Composite Index, rallied to fresh records this week.

The leading theory is that optimism over Mr. Trump’s tariff threat isn’t misplaced: The incoming president would prefer to win concessions on illegal immigration and drug smuggling. What’s more, the optimistic case rests on 2016, when Mr. Trump made similar tariff threats prior to the start of his first presidential term. Back then, negotiations prevailed and stocks gained.

Indeed, Magna’s share price rallied 31.4 per cent from election day 2016 through election day 2020, not including dividends. That was well ahead of the 8.8-per-cent gain for the S&P/TSX Composite Index over the same period.

At the very least, this outperformance suggests that investors can do well by tuning out the bluster from the White House over the next four years and focus instead on how Magna is responding to challenging operating conditions. The headwinds are still there, according to the bullish case, but so is a cheap stock.

(9:30 a.m. ET) Canada’s S&P Global Manufacturing PMI for November.

(9:45 a.m. ET) U.S. S&P Global Manufacturing PMI for November.

(10 a.m. ET) U.S. ISM Manufacturing PMI for November.

(10 a.m. ET) U.S. construction spending for October. The Street is forecasting a rise of 0.2 per cent from September.

Also: Canadian and U.S. auto sales for November.

—

Tuesday December 3

(10 a.m. ET) U.S. Job Openings & Labor Turnover Survey for October.

Earnings include: Bank of Nova Scotia; Descartes Systems Group Inc.; Marvell Technology Inc.; Salesforce Inc.

—

Wednesday December 4

Japan and Euro zone services and composite PMI

(8:15 a.m. ET) U.S. ADP National Employment Report for November.

(8:30 a.m. ET) Canadian labour productivity for Q3. Estimate is a decline of 0.3 per cent from Q2.

(9:30 a.m. ET) Canada’s S&P Global Services PMI for November.

(9:45 a.m. ET) U.S. S&P Global Services/Composite PMI for November.

(10 a.m. ET) U.S. ISM Services PMI for November.

(10 a.m. ET) U.S. factory orders for October. Consensus is a gain of 0.3 per cent from September.

(1:45 p.m. ET) U.S. Fed chair Jerome Powell participates in a moderated discussion at the New York Times DealBook Summit.

(2 p.m. ET) U.S. Beige Book is released.

Earnings include: Dollarama Inc.; Dollar Tree Inc.; EQB Inc.; GameStop Corp.; National Bank of Canada; North West Co. Inc.; Royal Bank of Canada

—

Thursday December 5

Euro zone retail sales

Germany factory orders

(8:30 a.m. ET) Canada’s merchandise trade balance for October.

(8:30 a.m. ET) U.S. initial jobless claims for week of Nov. 30. Estimate is 215,000, up 2,000 from the previous week.

(8:30 a.m. ET) U.S. goods and services trade deficit for October.

(10 a.m. ET) U.S. Global Supply Chain Pressure Index for November.

(10 a.m. ET) Canada’s Ivey PMI for November.

Also: OPEC+ meeting

Earnings include: Bank of Montreal; Canadian Imperial Bank of Commerce; Dollar General Corp.; Hewlett Packard Enterprise Co.; Kroger Co.; Lululemon Athletica Inc.; Toronto-Dominion Bank

—

Friday December 6

China foreign reserves

Japan household spending

Euro zone real GDP

Germany industrial production and trade surplus

(8:30 a.m. ET) Canadian employment for November. The Street is expecting a gain of 0.1 per cent, or 27,500 jobs, from November with the unemployment rate rising 0.1 per cent to 6.6 per cent and average hourly wages rising 4.5 per cent year-over-year.

(8:30 a.m. ET) U.S. nonfarm payrolls for November. Consensus is a gain of 200,000 jobs from October with the unemployment rate rising 0.1 per cent to 4.2 per cent and average hourly wages up 0.3 per cent month-over-month and 3.9 per cent year-over-year.

(10 a.m. ET) U.S. University of Michigan Consumer Sentiment Index for December (preliminary reading).

(3 p.m. ET) U.S. consumer credit for October.

Earnings include: BRP Inc.; Canadian Western Bank; Laurentian Bank of Canada

Five major Canadian news media companies on Friday filed a legal action against ChatGPT owner OpenAI, accusing it of regularly breaching copyright and online terms of use.

The move is the latest in a series of challenges for OpenAi, which has Microsoft as its major backer.

In a statement, Torstar, Postmedia, The Globe and Mail, The Canadian Press, and CBC/Radio-Canada said OpenAI was scraping large swaths of content from media to help develop its products without getting permission or compensating content owners.

“Journalism is in the public interest. OpenAI using other companies’ journalism for their own commercial gain is not. It’s illegal,” it said.

Earlier this month billionaire entrepreneur Elon Musk expanded a lawsuit against OpenAI. He said Microsoft and OpenAI illegally sought to monopolize the market for generative artificial intelligence and sideline competitors.

After slumping throughout much of 2022 and 2023, the share prices of Canada’s Big Six have been on a tear for more than a year as fears subside over high interest rates, a weak housing market and stretched household finances.

The group has rallied 44 per cent from its recent lows in October, 2023, easily outperforming the S&P/TSX Composite Index by about 11 percentage points – all while paying attractive dividends.

But this impressive group performance masks an unusually stark divergence between leading bank stocks and laggards.

Though less than 20 percentage points often separates them, the difference has grown as wide as 85 percentage points over the past 13 months. That is a gargantuan spread for entities that are essentially in the same business of underwriting loans, managing wealth and advising on deals.

“You’re starting to see clear winners out there,” Tony Ciero, senior portfolio manager at Caldwell Securities, said in an interview.

The way he sees it, interest rates are a key source of the divergence. Some banks suffered more than others as interest rates rose through 2022 and 2023, stoking concerns about loan losses as borrowing costs soared. Now, falling rates are also rewarding banks disproportionately as some stand to benefit more than others as concerns about loan losses subside.

Canadian Imperial Bank of Commerce CM-T -0.07%decrease sits comfortably at one end of the performance spectrum, with a gain of nearly 87 per cent (not including dividends) since October, 2023. At the other end, Toronto-Dominion Bank TD-T -0.89%decrease has gained just 2 per cent over this period, to Nov. 20.

Perhaps TD can be dismissed as an outlier, after the bank’s anti-money laundering lapses culminated in a US$3-billion fine in October and a cap on the bank’s U.S. asset growth.

Even so, CIBC is nearly 60 percentage points ahead of Bank of Montreal BMO-T +0.72%increase and 45 percentage points ahead of Bank of Nova Scotia BNS-T +0.10%increase.

“Our strategy is working, and it’s working well,” Victor Dodig, CIBC’s chief executive officer, said during a conference call with analysts in late August, after the bank reported its third-quarter financial results.

But CIBC isn’t the only cylinder firing within the banking sector. Both Royal Bank of Canada RY-T -0.54%decrease and National Bank of Canada NA-T -0.30%decrease have outperformed their peers, with gains of 57 per cent and 60 per cent, respectively, further underscoring the chasm between the haves and have-nots.

So how does an investor find the next haves?

Analyst reports, which offer sophisticated approaches to stock valuations, credit health and financial forecasts, can certainly help.

But you may discover that different analysts come to different conclusions, with conflicting views about the best bet. And when analysts do agree on a favourite, overwhelming consensus can suggest that a stock has too much optimism priced in and may disappoint lofty expectations.

Consider, then, adding the following four strategies to the mix.

We’ll be the first to admit that these approaches can look a little quirky at first glance. That’s because they virtually ignore fundamental issues such as strategy, leadership, acquisitions and the economic landscapein which banks function.

But they may shed some light on what has been driving Canadian bank stocks over the past year and could serve as useful add-ons to your current approach to picking bank stocks. Think of them as extra tools in the toolbox.

Embrace the laggard

This approach is for steely-nerved number crunchers who can ignore bad news: Rank bank stocks by their performance over the past 12 months, then pick the worst performer – that’s right, the dud, the dog or whatever you want to call it – and hang on for dear life in the hope that a rebound kicks in.

It often does. Big banks are well-run, highly regulated and stable financial giants that track the Canadian economy over time. More importantly, they tend to recover from short-term setbacks relatively fast, which can turn dips into buying opportunities.

“Canada is a special market when it comes to banking because it’s an oligopoly. You just don’t have the cut-throat competition that you see in the United States,” Alexander MacDonald, a portfolio manager at GlobeInvest Capital Management, said in an interview.

According to this approach, CIBC would have stood out as a buying opportunity before the current upswing began. From October, 2022, to October, 2023, while the entire banking sector struggled with rising interest rates and a shaky economy, the lender’s share price trailed its peers with a decline of 18 per cent.

The bank’s relatively high exposure to the Canadian housing market, through its large mortgage book, looked like a risk and was likely a reason for the stock’s lacklustre performance.

One year later, though, rates have begun to decline and exposure to the Canadian housing market is no longer a dead weight. Bingo! – CIBC has emerged as the top-performing big bank stock.

Though the long-term track record for the pick-the-laggard strategy is impressive – and a safer approach involves overweighting the three underperformers and underweighting the three overperformers – keep in mind that it has endured its share of misfires when losers kept losing.

Yeah, we’re referring to Scotiabank here. The bank was the laggard in 2020 and then underperformed all but one of its peers in 2021. In 2022, the bank emerged again as the laggard and underperformed all of its peers in 2023.

Move over, Scotiabank. Today’s top laggard is TD.

Gains in its share price have trailed its peers by 53 percentage points over the past 13 months. TD is also a distant 26 percentage points behind the second-worst laggard, Bank of Montreal.

Some analysts aren’t upbeat: “We believe it will be difficult for TD to outperform its peers over the medium term, as it has limited strategic flexibility, lower earnings/dividend growth and significant cultural change coming,” Darko Mihelic, an analyst at RBC Dominion Securities, said in a mid-October note.

Clearly, the case for TD’s recovery is anything but rock-solid. But this strategy doesn’t sweat the details.

Grab the biggest dividend

If you’re looking for a simpler approach to picking bank stocks, this one is straightforward. Rank Canadian bank stocks based on dividend yield or annualized payout divided by share price. Pick the highest yield and let the quarterly distributions flow.

The simplicity rests on a solid premise: Big banks offer reliable dividends, so why not grab the biggest?

Given their modest payout ratios – they generally distribute 40 per cent to 50 per cent of their profits in dividends – and large capital buffers, “banks have a lot more capacity to absorb ups and downs in their business if there is a near-term bump in profitability,” Monica Yeung, a portfolio manager at TD Asset Management, said in an interview.

A year ago, CIBC and Bank of Nova Scotia stood out for their extra-large dividend yields of more than 7 per cent, which made both stocks look like strong buying opportunities using this approach.

However, the strategy is hit-and-miss. Yes, both stocks have soared over the past year, but Scotiabank still sits among the bottom three performers.

More problematic: bank stocks with lower dividend yields have also performed well. RBC and National Bank trail only CIBC since October, 2023, even though the two banks had the lowest dividend yields among the Big Six banks at the start of the period.

Still, with bond yields declining and guaranteed investment certificates no longer the cash geysers they once were, there’s something to be said about turning to bank stocks for a source of income. Today’s top candidates: Scotiabank – again – offers the highest dividend yield of 5.4 per cent. TD has the second-highest yield, at 5.2 per cent.

Chase dividend growth

Rather than focusing on stocks with the highest dividend yields, this strategy looks at the banks that are delivering the biggest dividend increases.

A stock with a fast-rising dividend can offer a better income stream over the longer term than a stock whose quarterly payout is stuck in neutral. As well, generous dividend increases can reflect robust financial health and strong profit growth.

National Bank has been generating the best dividend growth among the Big Six banks.

It raised its quarterly payout by 7.8 per cent over the past year. That is considerably better than the 4.1-per-cent hikes by its peers, on average. And it is a lot better than miserly Scotiabank, which did not increase its quarterly payout at all over the same period.

National Bank also leads the way over the past five years, with average dividend growth of 10.2 per cent, according to data from Bloomberg.

Beyond receiving more income, investors have also benefited from a rising share price. National Bank is up 54 per cent over the past year and has led its peers by 64 percentage points over a five-year period.

Today’s best bet using this strategy: Stick with National Bank.

Though dividend growth can’t be predicted with any certainty, investors can make an educated guess using payout ratios, which tell you how much of a bank’s profits are being distributed in the form of dividends. National Bank’s ratio is the lowest among the Big Six, at 41.2 per cent, according to bank filings.

That’s also at the low end of the bank’s objective of distributing 40 to 50 per cent its income as dividends, which suggests there’s still plenty of room for increases.

“When we think about the next cycle of dividend hikes, which should come this quarter, National Bank probably has the most capacity to increase its dividend,” Ms. Yeung said.

Pursue profit growth

Banks tend to deliver steady but unspectacular profit growth over time unless they are rebounding from a horrendous period of loan losses and economic mayhem.

But do some banks deliver more than others? You bet, and in recent years profit growth has lined up nicely with stock performance.

National Bank, the best big-bank stock over the past five years in terms of cumulative gains, also has the best annualized five-year profit growth, at 10.5 per cent. That’s about twice the pace of its nearest competition, CIBC, over the same period. These results don’t include Canadian Western Bank, which National Bank is in the process of acquiring.

But Scotiabank may be the bank to watch now. Yes, Scotiabank.

Scott Thomson, who was recruited from outside the sector to lead the bank in 2023, has a clear mandate to turn things around and make shareholders happy. To achieve that, he has set bold efficiency targets and narrowed the bank’s focus to North America, which some investors are applauding.

“The biggest attraction is the pivot in strategy,” Mr. MacDonald said.

“For years, they’ve been pouring money into Latin America, which hasn’t been working out for them. So to see them getting away from that, there’s potentially some light at the end of the tunnel,” he said.

It is making moves already. In August, Scotiabank announced a deal to buy a minority stake in KeyCorp, injecting much-needed capital that should drive the U.S. regional bank’s net interest income, which will feed into Scotiabank’s profits.

As well, Scotiabank reported that its efficiency ratio – which compares expenses to revenue (lower is better) – declined to 56 per cent in the bank’s fiscal third quarter, down from 56.5 per cent a year ago. Its goal is to bring the ratio down 50 per cent over the next several years.

And the bank leads its peers with estimated profit growth of 8.3 per cent in fiscal 2025, according to FactSet. Scoff if you want. But as the past year demonstrates, winning bank stocks can emerge from humble beginnings.

(8:30 a.m. ET) Canadian manufacturing sales for October.

(8:30 a.m. ET) U.S. Chicago Fed National Activity Index for October.

(10:30 a.m. ET) U.S. Dallas Fed Manufacturing Activity for November.

Earnings include: Alimentation Couche-Tard Inc.; Zoom Video Communications Inc.

—

Tuesday November 26

(8:05 a.m. ET) Bank of Canada deputy governor Rhys Mendes speaks in Charlottetown.

(8:30 a.m. ET) Canadian wholesale trade for October.

(9 a.m. ET) U.S. S&P CoreLogic Case-Shiller Home Price Index (20 city) for September. Estimates are gains of 0.3 per cent month-over-month and 4.7 per cent year-over-year.

(9 a.m. ET) U.S. FHFA House Price Index for September. Estimates are a rise of 0.2 per cent from August and 4.7 per cent year-over-year.

(10 a.m. ET) U.S. new home sales for October. Estimate is an annualized rate drop of 2.7 per cent.

(10 a.m. ET) U.S. Conference Board Consumer Confidence Index for November.

(2 p.m. ET) U.S. Fed minutes from Nov. 6-7 meeting

Also: Nova Scotia election.

Earnings include: Analog Devices Inc.; Best Buy Co. Inc.; CrowdStrike Holdings Inc.; Dell Technologies Inc.; HP Inc.; Nordstrom Inc.

—

Wednesday November 27

China industrial profits

Germany consumer confidence

(8:30 a.m. ET) U.S. initial jobless claims for week of Nov. 23. Estimate is 217,000, up 4,000 from the previous week.

(8:30 a.m. ET) U.S. real GDP and price indexes for Q3. Estimates are annualized rate rises of 2.8 per cent and 1.8 per cent, respectively.

(8:30 a.m. ET) U.S. goods trade deficit for October.

(8:30 a.m. ET) U.S. wholesale and retail inventories for October.

(8:30 a.m. ET) U.S. durable and core orders for October. The Street expects month-over-month increases of 0.3 per cent and 0.2 per cent, respectively.

(9:45 a.m. ET) U.S. Chicago PMI for November.

(10 a.m. ET) U.S. personal spending and income for October. Consensus estimates are rises of 0.3 per cent from September for both.

(10 a.m. ET) U.S. core PCE price index for October. Consensus is a rise of 0.3 per cent from September and up 2.8 per cent year-over-year.

(10 a.m. ET) U.S. pending home sales for October.

Earnings include: Kroger Co.; VersaBank

—

Thursday November 28

Euro zone private sector credit and economic and consumer confidence

Germany CPI

U.S. markets closed (Thanksgiving)

(8:30 a.m. ET) Canada’s current account balance for Q3.

President-elect Donald Trump is vowing to impose tariffs of 25 per cent on all goods coming from Canada and Mexico on his first day back in the White House, until the U.S.’s two neighbouring countries stop all migrants and fentanyl from entering the nation.

Mr. Trump made the announcement at 6.35 p.m. Monday on his Truth Social platform, firing an opening salvo in the global trade war that he has long promised in his second term as U.S. president.

“As everyone is aware, thousands of people are pouring through Mexico and Canada, bringing Crime and Drugs at levels never seen before,” the president-elect wrote. “On January 20th, as one of my many first Executive Orders, I will sign all necessary documents to charge Mexico and Canada a 25% Tariff on ALL products coming into the United States, and its ridiculous Open Borders. This Tariff will remain in effect until such time as Drugs, in particular Fentanyl, and all Illegal Aliens stop this Invasion of our Country!”

For Canada, which sends more than 77 per cent of its exports to the U.S., the tariffs would represent an economic blow and threaten a recession, with the oil and auto industries particularly affected. For U.S. consumers, who would pay the cost of the tariffs, they would mean punishing inflation.

For Mr. Trump, the tariffs combine two of his foundational political issues: building protectionist trade barriers around the U.S. economy and hardening the country’s borders against migrants.

Much, however, remains unclear: whether Mr. Trump will actually be able to impose the levies, how specifically Canada and Mexico will satisfy his demands and how all of it will be bound up with his promised renegotiation of the U.S.-Mexico-Canada Agreement that governs continental trade.

Alimentation Couche-Tard ATD-T says its earnings attributable to shareholders were US$708.8-million in its second quarter.

That’s down 13.5 per cent from US$819.2-million a year earlier.

The Laval, Que.-based company says total revenues were US$17.4-billion, up six per cent from US$16.4-billion.

Earnings per diluted share were 75 cents US, down from 85 cents US during the same quarter last year.

The company says its adjusted net earnings were reduced primarily due to a lower road transportation fuel gross margin in the U.S. as well as softer consumer traffic and demand and other factors.

President and CEO Alex Miller says parts of the company’s fuel and convenience business continued to feel the effects of careful consumer spending, and the company is confident in its long-term strategic growth plan.