Current reference price: WTI was around US$77.54/bbl intraday on June 19, 2026, after falling sharply from above US$80 earlier in the week.

Base case, next 1–2 weeks:US$74–82/bbl, assuming Hormuz traffic continues but remains politically fragile.

Bull case:US$85–95/bbl if Iran’s closure threat becomes operationally real, insurance rates spike, or tanker traffic materially slows.

Bear case:US$68–74/bbl if U.S.–Iran talks stabilize, stranded Gulf barrels move quickly, and the market prices in surplus risk.

The key variable is not demand; it is shipping reliability through the Strait of Hormuz, which handles roughly 20% of global oil and LNG supply. Reuters reported that U.S. Central Command disputed Iran’s closure claim and said 55 merchant ships carrying more than 17 million barrels of oil transited the Strait on Saturday.

Base Forecast

Timeframe

WTI Forecast Range

Bias

Reason

Next week

US$74–82/bbl

Volatile / range-bound

Hormuz traffic continues, but political risk premium remains

1 month

US$72–85/bbl

Wide range

Depends on whether stranded Gulf supply clears smoothly

3 months

US$68–82/bbl

Mild downside bias

More supply returning could pressure prices unless disruption resumes

Base case is not a straight collapse because inventories are tight. Reuters reported that U.S. crude stocks dropped to their lowest level since 1985, while the EIA warned that OECD oil inventories were headed toward their lowest levels since at least 2003.

Key Drivers

1. Geopolitical risk: still high, but not fully priced as closure

Iran said it closed the Strait of Hormuz, but the U.S. disputed that claim and reported continued commercial transit. That means the market is likely pricing a risk premium, not a full blockade. A real closure would move WTI materially higher.

2. Oil flows are restarting, but not normal

Reuters reported that at least four tankers entered Hormuz on June 19, and analysts expected the deal to release more than 85 million barrels of stranded oil into global markets. That is bearish for oil if the barrels move smoothly.

3. Inventories remain the bullish offset

Even with peace-deal hopes, inventories are tight. The EIA said global stock draws were severe because of lost Middle Eastern output, and Reuters reported the EIA expected oil prices to remain elevated until flows normalize and inventories rebuild.

4. Forward supply risk is bearish

Reuters reported the IEA sees global supply significantly overtaking demand next year, and Citi’s base case expects oil markets to move into surplus with prices trending lower over 6–12 months.

CNQ, SU, IMO, CVE benefit; airlines and consumer discretionary pressured

WTI US$74–82

Neutral to mildly positive

Energy stable; pipelines less sensitive than producers

WTI US$68–74

Negative for producers

Energy sector underperforms; inflation relief helps rate-sensitive sectors

What Would Disprove the Base Case

The base case of US$74–82 WTI would be wrong if either of these happens:

Trigger

Forecast Change

Verified tanker stoppage through Hormuz

Move forecast toward US$85–95+

U.S.–Iran talks produce enforceable transit rules and exports resume quickly

Move forecast toward US$68–74

U.S. crude inventories keep falling despite resumed Gulf flows

Holds WTI above US$80

Brent/WTI both break below recent support on heavy volume

Confirms bear case

Bottom Line

WTI’s near-term fair range is US$74–82/bbl. The market is balancing two opposing forces: tight inventories and Hormuz risk are bullish, while resumed tanker traffic, possible Iranian supply, and surplus concerns are bearish. A verified Strait disruption is the clearest upside shock; a smooth reopening is the clearest downside trigger.

Canada CPI for May is the key domestic macro event, scheduled for Monday, June 22; this can affect banks, REITs, utilities, telecoms, and rate-sensitive dividend stocks.

U.S. PCE inflation, personal income/spending, Q1 GDP third estimate, durable goods, and jobless claims all land Thursday, June 25, making that the highest-risk macro day for North American equities.

Strait of Hormuz / Iran risk remains the major geopolitical variable for oil, gold, CAD/USD, and TSX energy stocks. Reuters reported conflicting claims: Iran said the Strait was closed, while U.S. Central Command said traffic continued.

Alimentation Couche-Tard reports Q4/FY2026 results on June 22 after market close, relevant to ATD.TO and the TTCS staples index.

TSX trading is open during the week; Canada Day closure is the following week on Wednesday, July 1, 2026.

Key Events & TSX Impact

Date

Event

Why It Matters for TSX

Most Affected Areas

Mon Jun 22

Canada CPI — May 2026

Direct read on inflation and Bank of Canada rate expectations. Hot CPI pressures rate-sensitive sectors; soft CPI supports dividend/defensive names.

Statistics Canada’s 2026 release schedule lists Consumer Price Index for May 2026 on June 22, Investment in building construction for April 2026 on June 22, and Travel between Canada and other countries for April 2026 on June 23.

Statistics Canada also released April retail sales on June 19, showing retail sales increased 0.5% to C$73.0B in April, with an advance estimate suggesting May sales increased 1.0%. That is a useful background input for Canadian consumer names next week, but it is already released data, not a new event next week.

U.S. releases

BEA’s release schedule shows Personal Income and Outlays for May 2026 on June 25 at 8:30 a.m., which includes PCE inflation. The BEA PCE page shows the prior April 2026 PCE inflation reading at +3.8% YoY, with the next release on June 25.

The U.S. Census durable goods schedule lists the May 2026 advance durable goods report for June 25, 2026 at 8:30 a.m.

Negative energy short-term; positive consumer/rate-sensitive sectors

ATD earnings beat

Supports TTCS and defensive staples

Positive ATD, TTCS

ATD earnings miss / weak guidance

Staples drag increases

Negative ATD, TTCS

Valuation Logic

The TSX is vulnerable to rate and commodity shocks because its sector mix is concentrated in financials, energy, materials, industrials, and dividend-sensitive defensives. The most important valuation variable next week is not a single earnings multiple; it is the direction of bond yields, oil, gold, and CAD/USD.

Input

Valuation Effect

Higher Canadian CPI

Higher discount rates; lower multiples for defensives and REITs

Higher U.S. PCE

Stronger USD, higher yields; pressure on gold and tech multiples

Higher oil from Hormuz risk

Energy cash-flow expectations rise; inflation risk also rises

Lower oil from reopening/supply normalization

Energy earnings expectations weaken; consumer inflation pressure eases

Strong ATD results

Supports premium valuation in staples

Weak ATD guidance

Pressure on TTCS multiple

Scenarios for TSX Next Week

Scenario

TSX Bias

Conditions

Bull

TSX grinds higher

Canada CPI and U.S. PCE come in softer; Hormuz remains open; oil stabilizes without inflation shock; ATD results support staples

Base

Choppy / range-bound

CPI/PCE roughly in line; oil headlines remain noisy; TSX rotates between energy, gold, banks, and defensives

Bear

TSX pulls back

Hot inflation data; stronger USD; yields rise; Hormuz risk escalates; oil spike revives inflation fears and pressures non-energy sectors

What Would Disprove the Base Case

The base case is range-bound, headline-driven trading. It would be disproved by any of the following:

Trigger

Interpretation

Canada CPI meaningfully above expectations

BoC easing hopes weaken

U.S. PCE above expectations

Fed-cut expectations weaken; global equities pressure

Verified Hormuz disruption

Oil shock becomes dominant TSX driver

Brent crude spikes sharply and holds

Energy leads, but broader TSX may weaken on inflation risk

Gold fails while yields rise

Gold miners lose defensive support

ATD breaks lower after earnings

TTCS weakness deepens

Actionable Takeaways

Most important day:Thursday, June 25 because of U.S. PCE, GDP, durable goods, income/spending, and jobless claims.

Most important Canadian release:Canada CPI on Monday, June 22.

Most important TSX stock event:ATD.TO earnings after close on June 22.

Most important geopolitical variable:Strait of Hormuz / Iran shipping risk.

Sectors to monitor closely: energy, gold miners, banks, REITs, utilities, consumer staples, and tech.

(8:30 a.m. ET) Canada’s job vacancy rate for April.

(8:30 a.m. ET) U.S. initial jobless claims for week of June 20. Estimate is 230,000, up 4,000 from the previous week.

(8:30 a.m. ET) U.S. personal spending and income for May. The Street is expecting month-over-month increases of 0.6 per cent and 0.4 per cent, respectively.

(8:30 a.m. ET) U.S. core PCE price index for May. The consensus forecast is a rise of 0.3 per cent from April and up 3.4 per cent year-over-year.

(8:30 a.m. ET) U.S. real GDP and price index for Q1. The Street is projecting annualized rate increases of 1.6 per cent and 3.5 per cent, respectively.

(8:30 a.m. ET) U.S. real GDP by industry for Q1.

(8:30 a.m. ET) U.S. pretax corporate profits for Q1.

(8:30 a.m. ET) U.S. durable and core goods orders for May.

Earnings include: BlackBerry Ltd.

Friday June 26

China’s industrial profits

Japan’s CPI

(8:30 a.m. ET) Canadian wholesale trade for May.

(8:30 a.m. ET) U.S. goods trade deficit for May.

(8:30 a.m. ET) U.S. wholesale and retail inventories for May.

(10 a.m. ET) U.S. University of Michigan Consumer Sentiment Survey for June.

Earnings include: Apogee Enterprises Inc.; Corus Entertainment Inc.

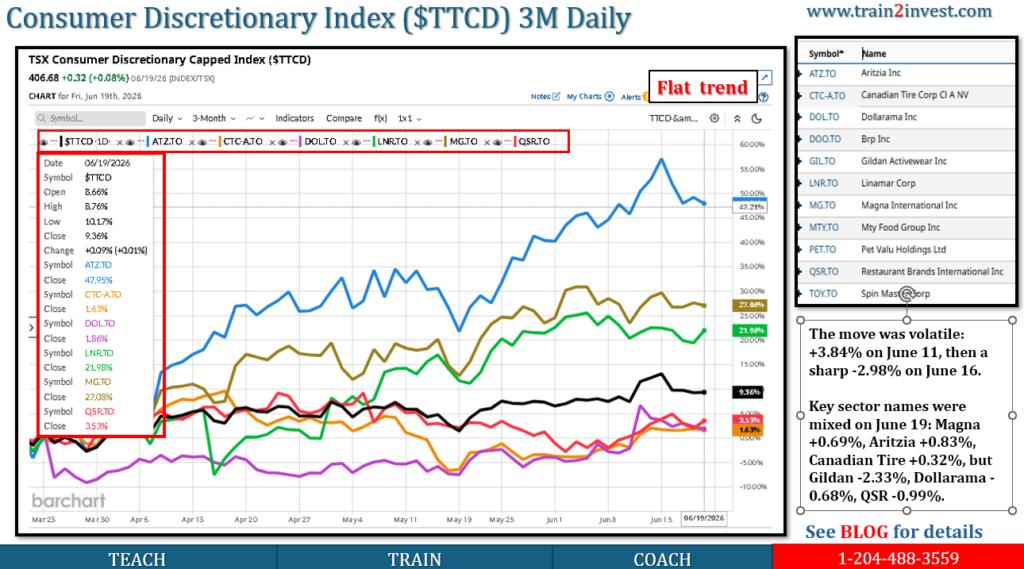

TTCD closed at 406.68 on June 19, 2026, up +1.24% over the last 10 trading sessions using June 5 close as the base.

Using June 8–June 19 closes only, TTCD rose +1.75%.

TTCD slightly outperformed the S&P/TSX Composite, which rose +1.29% from June 5 to June 19.

The move was volatile: +3.84% on June 11, then a sharp -2.98% on June 16.

Key sector names were mixed on June 19: Magna +0.69%, Aritzia +0.83%, Canadian Tire +0.32%, but Gildan -2.33%, Dollarama -0.68%, QSR -0.99%.

TTCD — Last 10 Trading Sessions

Date

Close

Daily Change

Jun 19

406.68

+0.08%

Jun 18

406.36

-0.44%

Jun 17

408.16

-0.03%

Jun 16

408.27

-2.98%

Jun 15

420.79

+0.75%

Jun 12

417.67

+0.69%

Jun 11

414.81

+3.84%

Jun 10

399.47

-0.92%

Jun 9

403.18

+0.88%

Jun 8

399.67

-0.50%

Jun 5

401.68

+0.24%

Source data: Investing.com historical table for GSPTTCD.

Performance Math

Measure

Result

Jun 5 close

401.68

Jun 19 close

406.68

Point change

+5.00

10-session change

+1.24%

Jun 8–Jun 19 close-to-close

+1.75%

Pullback from Jun 15 close of 420.79

-3.35%

Pullback from Jun 15 intraday high of 423.67

-4.01%

Key Drivers

Macro: TTCD benefited early in the period from broad risk appetite, but the sector lost momentum after the TSX pulled back from record highs. On June 17, Reuters reported the TSX retreated after hawkish Federal Reserve signals, with investors reassessing the higher-for-longer interest-rate backdrop.

Sector: Consumer discretionary is sensitive to rates, credit conditions, household spending, and confidence. The June 16 drop suggests profit-taking after the June 11–15 rally rather than a smooth uptrend.

Company mix: The sector was not uniformly strong. On the latest quoted day, Magna and Aritzia were positive, while Gildan, Dollarama, QSR, BRP, and Pet Valu were weaker. That points to stock-specific dispersion rather than a clean sector-wide breakout.

Scenarios

Scenario

Interpretation

Bull

TTCD holds above ~406 and retests the 420–424 area if rate pressure eases and cyclicals recover.

Base

Range-bound between ~400 and ~420 as investors rotate between defensives, cyclicals, and financials.

Bear

Break below ~400 if bond yields rise, consumer spending weakens, or key components such as Gildan, QSR, DOL, or MG sell off together.

Actionable Takeaways

TTCD’s past 10-day performance was positive but choppy, not a clean momentum move. The strongest signal was the June 11 jump; the warning signal was the June 16 reversal. For monitoring, watch 400 support, 420–424 resistance, Canadian bond yields, and the large sector constituents: MG, DOL, QSR, GIL, ATZ, CTC.A, LNR, DOO, PET.

TSX fell for three straight sessions after a record close on June 16, 2026, dropping from 35,389.58 to 34,857.34 by June 19: -532.24 points / -1.5%.

Main driver: profit-taking after record highs, amplified by a hawkish U.S. Federal Reserve signal that reduced rate-cut expectations.

TSX-specific pressure came from commodity-linked sectors: lower oil and gold hit energy and materials/mining shares.

June 19 weakness was concentrated in basic materials, with gold miners such as Alamos Gold and Agnico Eagle weighing on the index.

The decline looks like a valuation/rate/commodity reset, not evidence of a broad Canadian recession shock by itself.

TSX Move: June 17–19, 2026

Date

TSX Close

Daily Change

Main Reported Driver

June 16

35,389.58

+113.94 / +0.3%

Record high, helped by financials and metal miners

June 17

35,125.11

-264.47 / -0.8%

Fed hawkishness; resource and industrial weakness

June 18

34,969.26

-155.85 / -0.4%

Lower oil and gold; higher-rate concerns

June 19

34,857.34

-111.92 / -0.3%

Basic materials/gold miners weighed on TSX

Total from June 16 close to June 19 close: -532.24 points = -1.50%

Key Drivers

1. Fed rate shock hit equity valuations

The immediate trigger was the U.S. Federal Reserve’s more hawkish tone. Markets interpreted the Fed message as reducing the odds of rate cuts and increasing the possibility of higher rates later in 2026. That matters for the TSX because higher U.S. rates usually pressure valuation multiples, especially after a strong rally.

This was not just a Canada issue. U.S. equities also sold off on June 17 after traders increased bets on a potential Fed hike.

2. TSX was vulnerable because it had just hit a record high

The TSX had reached a record close on June 16 at 35,389.58. After a record run, even a modest macro surprise can trigger profit-taking. The June 17 decline was described as a pullback from that record high.

3. Commodity weakness hit Canada harder than the U.S.

The TSX has heavy exposure to energy, materials, financials, and industrials. On June 18, the decline was linked directly to lower oil and gold prices, plus the Fed’s hawkish stance. That combination is negative for a commodity-linked index because it hits earnings expectations for miners and energy producers while also pressuring valuation multiples.

4. Gold miners dragged the index on June 19

On June 19, the pressure was mainly in basic materials, with gold miners weighing on the index. Reports cited Alamos Gold down about 18% and Agnico Eagle down about 2% as notable drags.

5. Weaker Canadian macro signals added pressure

The Canadian dollar fell to a 14-month low on June 19, pressured by weaker core retail sales, falling oil prices, and a stronger U.S. dollar after the Fed’s hawkish stance. That reinforced the message of softer domestic demand and tighter financial conditions.

What It Means

This was mainly a three-factor pullback:

Factor

Impact on TSX

Hawkish Fed

Higher discount rates; lower equity multiples

Lower oil/gold

Direct pressure on TSX energy and materials

Record-high starting point

Profit-taking after strong run

The TSX decline was not large in percentage terms: about -1.5% over three sessions. The pattern suggests a controlled pullback rather than a market breakdown.

Scenarios

Scenario

What Happens Next

TSX Implication

Bull

Oil/gold stabilize; Fed hike fears fade

TSX retests 35,000–35,400

Base

Rates stay uncertain; commodities mixed

TSX trades sideways around 34,700–35,200

Bear

Fed hike odds rise; gold/oil fall further

TSX tests lower support near 34,400–34,600

What Would Disprove the “Normal Pullback” View

The decline would become more concerning if:

TSX breaks below the early-June low area near 34,100–34,400.

Financials join materials and energy in sustained weakness.

Oil and gold continue falling together.

U.S. yields keep rising and Fed hike odds increase further.

Canadian consumer/economic data deteriorates beyond retail sales weakness.

Actionable Takeaways

Treat June 17–19 as a rate-and-commodity-driven pullback, not a standalone recession signal.

Watch gold miners, energy stocks, and financials for confirmation.

The key macro variable is now U.S. rate expectations; the key TSX-specific variable is commodity price direction.

A recovery likely requires either lower bond yields, stabilizing oil/gold, or renewed strength in financials.

The Canadian dollar has been underperforming the US dollar since the onset of the Iran war.

The loonie softness is largely due to US dollar strength rather than domestic fundamentals, according to analysts.

Expectations of US Federal Reserve interest rate increases are amplifying the greenback’s strength.

With the Canadian dollar slumping against the US dollar, 2026 isn’t turning out the way many analysts expected. Coming into this year, forecasters had a strong outlook for the Canadian dollar, amid expectations of a healthy economy and Federal Reserve interest rate cuts in the United States. But the Iran war upended this. The Canadian economy is struggling, and investors now think the Fed could raise rates before 2026 is over. Not only that, but analysts say the US dollar has benefited from investors using it as a haven to mitigate war-related volatility.

The Canadian dollar was trading at C$1.39 against the US dollar on June 4, having fallen from C$1.35 just a week after the Iran war broke out on Feb. 28. A once-bullish outlook has turned dour. Analysts expect the loonie to continue to lag in the near term as economic resilience and expectations of higher-for-longer interest rates in the US continue to provide tailwinds for its currency.

The big picture is that the Canadian dollar’s fortunes are being driven more by US than Canadian dynamics, according to analysts. “We estimate around 85% of the move in [the Canadian dollar] has been driven by broader US dollar strength—due both to the rise in geopolitical risk and better-than-expected data [in the US],” says Sarah Ying, head of FX strategy at CIBC.

Currency analysts attribute only a limited share of the loonie’s recent weakness to domestic factors, such as a faltering labor market, slower GDP growth, and fading expectations for interest rate hikes at the Bank of Canada. Canada’s economy unexpectedly shrank in the first quarter, following a larger contraction in the fourth quarter of 2025, marking two consecutive quarters of negative economic growth. This is the technical definition of a recession.

The Loonie Lags as Iran War Jitters Fuel US Dollar’s Surge

The Canadian dollar started the year at C$1.37 against the US dollar, and it drifted higher to C$1.35 in February, boosted by growing expectations for a Bank of Canada rate hike and strong momentum in commodities, particularly gold. However, the script flipped when the Iran war erupted. War-driven oil price volatility prompted investors to seek refuge in the US dollar.

Nick Rees, head of macro research at Monex Canada, says that while the currencies of all the Group of 10 countries have slid against the US dollar, “the loonie is the worst-performing.”

Weaker Domestic Economic Data

Analysts say that some of the loonie’s weakness comes from concerns that domestic economic growth is being held back by a softening labor market and an uptick in inflation. “Relatively soft economic data early in May contributed to underperformance,”says Tom Nakamura, currency strategist and co-head of fixed income at AGF Investments.

In contrast, the US economy has shown signs of resilience, according to CIBC’s Ying. “Recent data suggests the American job market has stabilized, and inflation is running a bit higher than expected, partly because of rising energy costs,” she says.

Divergent Central Bank Rate Paths

With the Canadian economy softening and the US economy remaining healthy (though with high inflation), the outlook for monetary policy in both countries is heading in opposite directions.

The oil shock from the Iran war “has created some material concern that persistent inflation could not only prevent the Fed from cutting rates, but also compel it to hike rates to moderate inflation expectations,” says AGF’s Nakamura, who adds that this has helped drive up the US dollar.

Meanwhile, inflation in Canada has been showing signs of cooling, evidenced by core CPI (which excludes food and energy) hovering around 2%. “While higher energy prices could push core inflation up slightly, we don’t see an urgent need for the Bank of Canada to raise interest rates this year,” says CIBC’s Ying.

The resulting higher rates in the US and steady rates in Canada “tend to strengthen the US dollar against other currencies, including the Canadian dollar,” Ying says.

What Needs to Change to Lift the Loonie?

For the Canadian dollar to reverse its course and close the gap with the US dollar, analysts say that certain catalysts must materialize. The Canadian dollar could appreciate if “the Strait of Hormuz opens, with the expectations that it will remain open and [the West Texas Intermediate crude oil price] normalizes to USD 80-USD 85,” says CIBC’s Ying. Other potential key drivers include deteriorating US employment data, which would require the Fed to ”remain patient for longer,” or certainty about the Canada-United States-Mexico Agreement.

Monex’s Rees says the Canadian dollar could see a reprieve in the third quarter, when he expects domestic economic indicators to improve, following a resolution to the war in the Middle East and greater clarity around the trade deal with the US. “At that point, we see a solid case for loonie gains, with the economy starting from a weaker base, meaning greater scope for improving data to fuel the Canadian dollar upside,” he says.

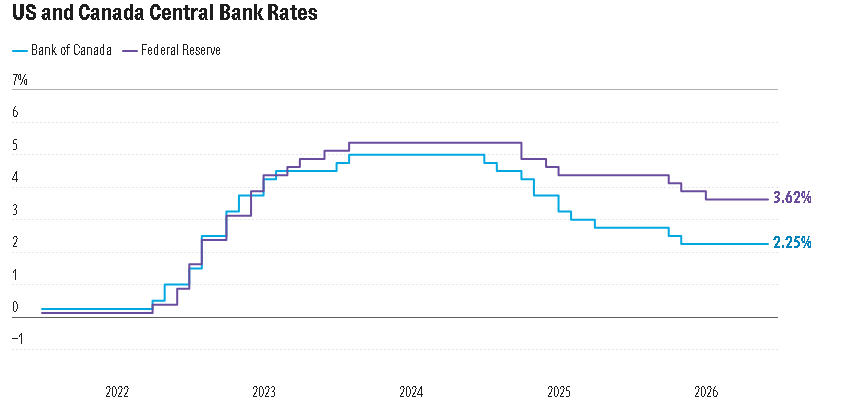

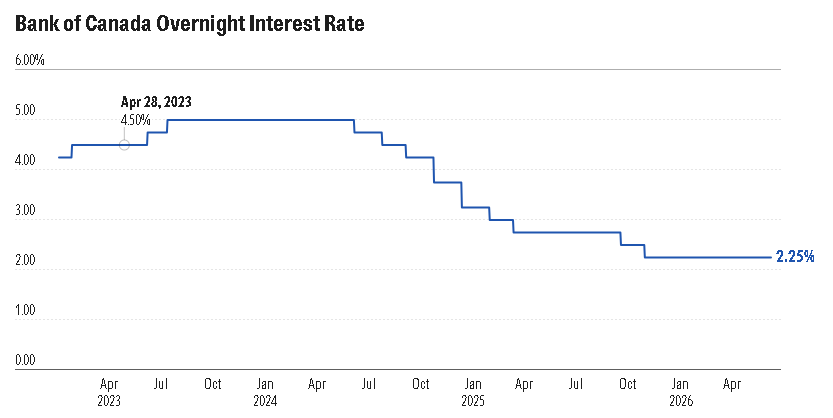

The Bank of Canada left its overnight interest rate unchanged, marking a fifth consecutive hold.

Policymakers highlighted the complexity of responding to opposing forces of slower growth and higher inflation from the Iran war.

Some analysts see a slight shift in the Bank’s tone away from rate hikes, but most believe policy will be on hold throughout 2026.

For the fifth time in a row, the Bank of Canada held its overnight interest steady at 2.25% on Wednesday, as it juggles the economic impact of Iran war-driven energy prices and trade uncertainty. Analysts say the central bank is in no hurry to change rates, and this hold could be extended throughout the year.

In its policy statement, the Bank underscored the challenge of balancing weaker-than-expected first-quarter economic activity with a reacceleration in inflation to 2.8% in April from 2.4% the month before, stemming from the war in the Middle East. “Economic weakness combined with rising inflation is a dilemma for monetary policy,” said Bank Governor Tiff Macklem at the press conference following the announcement. “Raising rates to dampen inflation could further slow the economy. Easing rates to support growth increases the risk that higher inflation becomes persistent.”

For that reason, the Governing Council decided to look past the Iran war’s near-term inflationary effects. But policymakers reiterated their readiness to enact multiple rate hikes conveyed in the April Monetary Policy Report: “if energy prices stay high, we will not let their effects become broad-based persistent inflation.” At the same time, the Bank acknowledged that it may need to cut rates to support the economy, should “the United States impose significant new trade restrictions on Canada.”

The Bank cut the overnight rate by 1 percentage point over the course of 2025 before moving to the sidelines in December.

Following the announcement, most analysts—including those at Vanguard, BMO, TD Economics, and CIBC—say that despite energy-driven inflation, economic weakness and trade uncertainty will prevent the Bank from hiking rates this year. In contrast, analysts at Mackenzie and IG Wealth forecast that a rate cut could come as early as later this year

Markets were little changed by the news. The Canadian dollar rose 0.31% against the US dollar to C$1.39, or 0.71 US cents. The S&P/TSX Composite Index edged 0.17% lower to 34,369.55, while the Morningstar Canada Index slid 0.26% to 6,089.99. The yield on Government of Canada 2-year bonds ticked 0.02 percentage points lower to 2.82%.

Here’s a closer look at commentary on the Bank of Canada’s decision and the outlook for interest rates.

Bank of Canada on Hold Through 2026

“Very little new information from the Bank of Canada, as the June policy statement and opening statement were similar to April’s. The extra line about the economy being ”weak” is a touch more dovish, but there’s still concern about the potential for rising inflation from higher energy prices. We continue to expect the Bank of Canada to stay on hold through the rest of 2026.”

—Benjamin Reitzes, managing director, Canadian rates and macro strategist at BMO Economics

No Rate Move Expected Until Next Year

“The slightly dovish shift [a tilt towards easing policy] in language from the Bank of Canada today provides support to our forecast that it will leave interest rates unchanged this year … Governor Tiff Macklem has tweaked some of the key phrases in his opening statement to the press conference. Back in April, Macklem said that ‘if the economy evolves broadly in line with the base case, changes in the policy rate can be expected to be small.’ Today, he notes that ‘economic weakness combined with rising inflation is a dilemma for monetary policy’ and that ‘holding the policy rate unchanged balances those risks.’

“That tweak makes us a bit less concerned about the possibility that the Bank might have wanted to raise interest rates modestly simply to position itself back in the middle of its 2.25% to 3.25% neutral range estimate, leaving us comfortable with our view that the Bank is unlikely to move in that direction until at least early 2027.”

—Stephen Brown, chief North America economist at Capital Economics

Bank of Canada Appears Set to Stay on Hold

“Overall, we view today’s communication as highlighting a very patient central bank that has plenty of time to wait and see how risks to the economy play out. We continue to see no change in interest rates this year, and that rates at their current level should support a recovery in the economy later this year and into 2027, assuming some of the uncertainties regarding oil prices and trade lessen during that time period.”

—Andrew Grantham, senior economist at CIBC Capital Markets

The BoC Is in No Hurry to Move Rates

“For the moment, the Governing Council seems very comfortable leaving rates unchanged. It’s a bit surprising that Macklem largely repeated the language used in April, given the persistent weakness in Canadian economic indicators and the tame nature of underlying inflation. That said, markets aren’t taking the bait this time. Despite his commentary on the possibility of consecutive rate hikes, Government of Canada bond yields are slightly lower on the day.”

—Royce Mendes, managing director and head of macro strategy at Desjardins Capital Markets

Rate Hike Expectations Could Give Way to a Cut

“Unfortunately for those looking for a strong signal in either direction, the Bank didn’t say much. Coming off two disappointing quarters of negative GDP growth on an annualized basis and three negative quarters out of the last four, the Bank couldn’t simply overlook the deceleration in economic activity. And while last month’s jobs data was an encouraging sign, excluding the COVID period, the 12-month average job gains are still near the lowest in 10 years. These are economic conditions that the Bank can’t ignore. And by its statement, it didn’t and at the same time, gave nothing away.

“Nonetheless, while the Bank’s mandate is price stability, with a target of 2% inflation +/- 1%, given the economic conditions, there is room for the Bank of Canada to cut the overnight rate and provide some stimulus. This runs counter to other central bank postures, in particular what is becoming the prevailing view that the US Federal Reserve may be forced into a hike before the end of the year. However, the Canadian economy is not the US economy, and the Bank recognizes that. Views for the Bank of Canada to raise its overnight rate once before the end of the year should quickly turn into expectations for a cut.”

“The statement was largely a copy of April’s, noting both risks of a hike and cut under various scenarios. The Bank of Canada continues to emphasize it will not let inflation move materially higher, but also continues to stress it views the hostilities in the Middle East as temporary and will look through. On the other hand, the Bank continues to be concerned over the outcome of USMCA [United Sates-Mexico-Canada Agreement], and disruptions in the agreement to long-established supply chains could necessitate some easing in policy rates.

“The Bank of Canada appears to be on hold for the foreseeable future. Mackenzie continues to see significant risks to USMCA implementation as well as other domestic macro headwinds, and expects the Bank to cut rates before year end.”

—Dustin Reid, chief strategist, fixed income at Mackenzie Investments

Rate Hold to Last Through the Year

“The outlook remains highly uncertain. Oil prices have come off their peaks but are still high as uncertainty about the course of the conflict in the Middle East persists. On the other hand, negotiations around the CUSMA review have yet to get started, casting a pall over trade prospects. Recent data suggest a second-quarter bounce-back in growth, but one that is insufficient to absorb all of the excess capacity in the economy. Given the competing forces on inflation, we expect the Bank of Canada to stay on hold through the balance of the year.”

—Andrew Hencic, director and senior economist at TD Economics

A Rate Hike Is Unlikely This Year

“Elevated uncertainty and the energy price shock associated with the US–Iran conflict are likely to weigh on global demand, shaping the backdrop against which the Bank of Canada is setting its policy rate. Canada stands out among advanced economies in that higher oil prices may provide a modest near‑term boost to GDP, on the order of 10 to 20 basis points, reflecting its position as a net energy exporter.

“However, this growth impulse arrives alongside an inflationary shock. Higher energy prices are pushing up headline inflation and raising the risk that the disinflation process stalls in the near term. For the Bank of Canada, this creates a more complicated policy environment. While growth may receive a temporary lift, inflation dynamics limit the central bank’s flexibility. In our view, this trade-off makes it more difficult for policymakers to pivot toward rate cuts, reinforcing our expectation that the Bank of Canada’s policy rate will remain unchanged at 2.25% through year‑end 2026.”

—Ashish Dewan, investment strategist at Vanguard Canada

Vice President JD Vance told Fox News on Saturday that “we’re not seeing any evidence that the Iranians are still closing down the Strait of Hormuz.”

“It is going to take some time to clear those mines, though,” Vance told “Fox & Friends Weekend.”

“We got 16 million barrels out of the Strait of Hormuz in just the last 24 hours. That is basically to where it was before the war even started. And so that suggests that the Straits really are open,” Vance also said.

Iran MOU: Yes, it appears valid/in effect, but it is fragile and provisional, not a final peace treaty. Reuters reports U.S. and Iranian officials said it was digitally signed and Iran said it was already in effect as of Wednesday, June 17, 2026.

Legal status: It is best treated as a 60-day ceasefire / negotiation framework, not a comprehensive settlement. A U.S. official said parties could still walk away and sequencing is key.

Strait of Hormuz:Not clearly “closed” in a fully enforced physical sense, but it is high-risk and severely disrupted. Iran/IRGC has declared closure again, while U.S. officials dispute that an actual shutdown is occurring.

Shipping evidence is mixed: UKMTO/JMIC said on June 18 the maritime threat level had been reduced to moderate after reopening intentions, but separate tracking showed very limited or no active commercial outbound transits early June 20.

Market reading: Treat the MOU as still alive but under stress; treat Hormuz as functionally constrained, not safely normalized.

Direct Answer

1. Is the Iran MOU valid?

Yes — currently valid, but weak.

The reported MOU was signed by U.S. President Donald Trump and Iranian President Masoud Pezeshkian, according to Reuters, and Iran said it was already in effect as of June 17. The agreement reportedly extends the ceasefire for 60 days and is meant to allow talks toward a final truce.

However, it is not a durable final agreement. Reuters also reported that a U.S. official said either side could still walk away, and implementation depends heavily on sequencing.

Conclusion: Valid on paper; fragile in practice.

2. Is the Strait of Hormuz closed?

Not conclusively closed in the sense of a complete, verified, enforced shutdown. But it is not normal either.

Iran’s military/IRGC has declared the Strait closed again, citing alleged ceasefire violations. Reuters reported Iran’s announcement via Mehr on June 20.

But Axios reported that a senior U.S. defense official said there were no signs of Iranian military activity indicating an actual closure.

There is also evidence of some vessel movement: three Indian-flagged oil tankers reportedly crossed the Strait and headed to India.

Conclusion: The correct wording is: Hormuz is threatened, restricted, and risky — not clearly confirmed as fully closed.

Practical Market Interpretation

Question

Best Current Assessment

Confidence

Is the MOU valid?

Yes, but provisional and fragile

Medium-high

Is the MOU a final peace deal?

No

High

Is Hormuz fully closed?

Not confirmed

Medium

Is Hormuz back to normal?

No

High

Is oil risk premium still justified?

Yes

High

TSX / Market Impact

Short term: Bullish for oil volatility, energy risk premium, gold risk hedge, and defence/security sentiment. Negative for airlines, transport, chemicals, and consumer discretionary if crude spikes.

Long term: If the MOU survives and Hormuz traffic normalizes, the oil risk premium should fade. If the MOU breaks, Brent could reprice sharply higher.

What Would Disprove This View

The “Hormuz not fully closed” view would be wrong if confirmed AIS, UKMTO, Lloyd’s List, or naval sources show sustained zero commercial transit plus active Iranian enforcement.

The “MOU still valid” view would be wrong if either Washington or Tehran formally withdraws, suspends implementation, or resumes direct military action.

Bottom line: The MOU is valid but fragile. The Strait of Hormuz is not reliably open in a normal commercial sense, but a full enforced closure is not yet independently confirmed.