Executive Summary: Past 10 Days

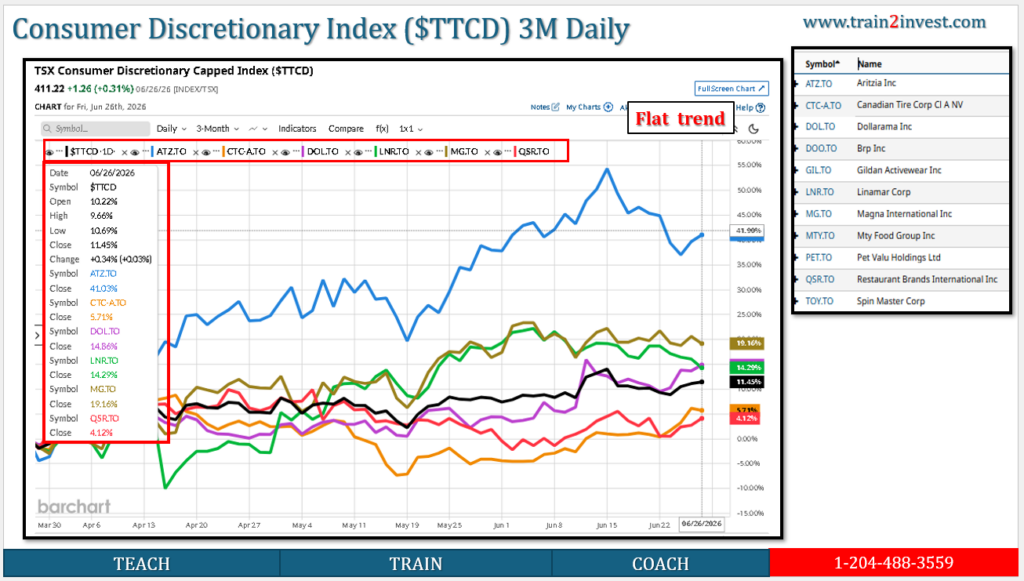

- TTCD has been rising, not falling: latest quoted level was 411.22, up +0.31% on the day, with a 52-week high of 423.67.

- Exact 10-trading-day return was not available from the accessible data, but Barchart shows +1.12% over 5 days and +3.04% over 20 days, so the 10-day move likely sits between those unless there was a sharp single-day reversal.

- The move appears driven by large constituents, especially Dollarama, Restaurant Brands, Magna, Aritzia, and Canadian Tire, which TMX lists among TTCD’s major holdings.

- Aritzia has been a major positive fundamental driver: Q4 fiscal 2026 revenue rose 32.6% YoY, comparable sales rose 27.7%, and U.S. revenue rose 37.8%.

- The index is still below its recent high: 411.22 vs 423.67, about 2.9% below the 52-week high.

Key Drivers

1. Consumer discretionary sentiment improved

TTCD benefits when investors become more comfortable with Canadian consumer spending, retail earnings, and rate-sensitive cyclicals. The recent move looks like a risk-on / consumer resilience trade, rather than a defensive sector rotation.

2. Aritzia strength helped sentiment

Aritzia’s latest reported quarter was very strong: net revenue +32.6% YoY, comparable sales +27.7%, digital revenue +29.2%, and U.S. revenue +37.8%. That supports the view that higher-quality discretionary retailers can still grow despite tariff and consumer pressure.

3. Canadian Tire showed “resilient but selective” consumer behaviour

Canadian Tire’s Q1 showed revenue +3.3%, retail revenue +2.9%, and EPS of C$2.02 versus C$0.67 a year earlier, but comparable sales were still down 1.0%. That is mixed: supportive for earnings quality, but not a broad spending boom.

4. Technical position is constructive but not overextended

| Measure | Reading | Interpretation |

|---|---|---|

| Last price | 411.22 | Near upper range |

| 5-day change | +1.12% | Short-term upward momentum |

| 20-day change | +3.04% | Broader 1-month recovery |

| 9-day RSI | 59.73 | Positive, not extreme |

| 14-day RSI | 58.43 | Momentum supportive, not overbought |

| 9-day ATR | 1.55% | Normal short-term volatility |

Source: Barchart technical table.

Interpretation

TTCD’s recent strength looks like a controlled advance, not a blow-off rally. The index is above its short-term moving average and showing positive 5-day and 20-day performance, but RSI near 58–60 suggests momentum is healthy rather than stretched.

The main reason: investors are rewarding selective consumer strength. Aritzia is showing exceptional growth, Canadian Tire is showing resilience but mixed same-store sales, and larger holdings like Dollarama and Restaurant Brands add quality/defensive-growth characteristics inside a discretionary index.

Risks

- Tariffs / input costs: Aritzia itself flagged tariff impact and de minimis changes, even while margins improved.

- Consumer slowdown: Canadian Tire’s comparable sales decline shows consumers remain selective.

- Auto exposure: Magna adds cyclical and tariff-sensitive auto exposure to TTCD.

- Index near resistance: TTCD is still below the 423.67 high; failure near that level would suggest the rally is losing breadth.

Scenarios

| Scenario | What happens next | TTCD implication |

|---|---|---|

| Bull | Retail earnings stay strong, rates ease, consumer spending holds | Retest of 423–424 area |

| Base | Mixed earnings, selective spending, no major macro shock | Range trade around 405–415 |

| Bear | Consumer data weakens, tariffs pressure margins, auto stocks lag | Pullback toward 399–405 support zone |

Actionable Takeaways

TTCD’s past 10-day movement is best explained as positive sector rotation into higher-quality consumer names, supported by strong Aritzia results and resilient Canadian Tire data. The short-term trend is constructive, but the index is close enough to its recent high that confirmation requires a move above the 423–424 zone.