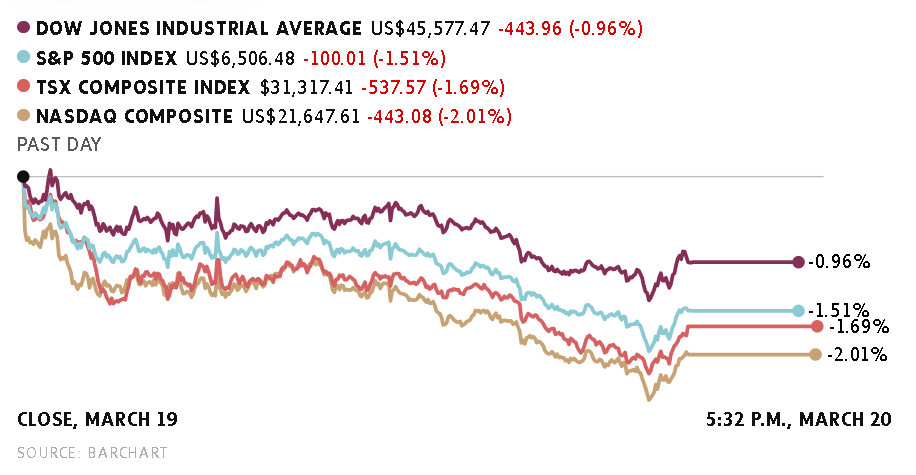

Extending the nosedive seen over the two previous sessions, Canadian stocks plunged on Friday as inflationary concerns due to the intensifying gulf war pressured investors away from risky assets.

After opening below yesterday’s close, today the benchmark S&P/TSX Composite Index traded firmly negative before settling at 31,317.23, up by 537.75 points (or 1.69%).

Of the 11 sectors, only Consumer Staples posted gains today.

The U.S.-Israel versus Iran war entered day number twenty-one.

Today, Kuwait’s largest oil refinery, Mina al-Ahmadi, which processes around 730,000 barrels of oil per day, was struck by Iran, leading to the shutdown of several of its units.

Following Israel’s massive attacks on Iran’s South Pars gas field, Iran conducted strikes on Qatar’s largest LNG plant, Ras Laffan. The facility suffered extensive damage, with the resumption of operations estimated to begin only after a year.

Iran warned that it will show “zero restraint” if its facilities are attacked again.

With an end to the conflict, becoming unpredictable, the spike in crude oil prices and the resultant inflation concerns, along with vanishing expectations of any rate cut in the near-term, have forced investors to avoid making “big” investments.

The Strait of Hormuz, a narrow waterway off Iran’s coastal region remains blocked for vessels carrying oil and energy from Arab nations.

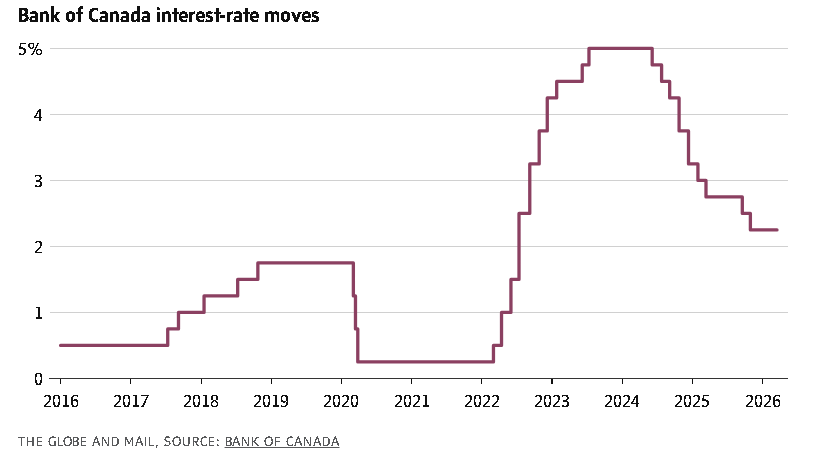

The U.S. Federal Reserve held interest rates at the current 3.50% to 3.75% range on Wednesday.

Market participants have canceled their bets on lowering of interest rates by the Fed, with many of them anticipating a rate hike this year.

The CME Group’s FedWatch Tool was last seen indicating that traders were betting on a 12.40% chance of a “quarter-point rate hike” at the April meeting.

Other central banks globally have followed suit, expressing concerns about the impact of skyrocketing crude oil prices on national economies and the inflationary effects.

On Wednesday, the Bank of Canada elected to hold interest rates at the current 2.25% level.

Data released by Statistics Canada today revealed that Canadian producer prices rose by 0.4% month-over-month in February, below market forecasts of a 1.1% increase. Producer Prices surged 5.4% in January compared to the same month in the previous year.

A preliminary estimate revealed that retail sales in Canada increased by 0.90% from February.

With rate-cut expectations receding from the radar, the attention of traders is now focused on any breakthrough in the Canada-United States-Mexico agreement.

The only sector that gained in today’s trading was Consumer Staples (0.17%).

Among the individual stocks, Maple Leaf Foods (2.37%), Saputo Inc (1.36%), Metro Inc (0.80%), and Weston George (0.45%) were the prominent gainers.

Major sectors that lost in today’s trading were Utilities (2.02%), IT (2.62%), Healthcare (2.94%), and Materials (3.13%).

Among the individual stocks, Lithium Americas Corp (7.59%), Vizsla Silver Corp (6.85%), B2Gold Corp (6.75%), Perpetua Resources Corp (5.77%), and Curaleaf Holdings Inc (4.75%) were the notable losers.

Orla Mining Ltd (4.50%) and Secure Waste Infrastructure Corp (3.65%) were among the prime market-moving stocks today.